By Rinki Pandey September 12, 2025

ACH debit is a core component of electronic payments in the United States. Business owners often encounter ACH debits when collecting customer payments or paying bills.

But what does ACH debit mean and why does it matter for your business? In this guide, we’ll explain the meaning of ACH debit, how it works in the U.S. ACH network, and its benefits and considerations for businesses.

We’ll also provide up-to-date facts, practical examples, and expert insights to ensure you have a clear, current understanding of ACH debit.

The Automated Clearing House (ACH) Network is the backbone of U.S. bank-to-bank payments. It’s a system that moves money electronically between bank accounts, processing billions of transactions annually.

In 2023 alone, the ACH Network handled 31.5 billion payments totaling $80.1 trillion in value. A significant portion of these were ACH debit transactions – electronic “pull” payments where funds are withdrawn from one account and transferred to another.

This comprehensive guide focuses on the U.S. ACH system and is tailored for business owners.

We’ll cover ACH debit meaning, how ACH debits work, the differences between ACH debits and ACH credits, and why ACH debits can be advantageous for companies.

You’ll learn about the setup process, costs, timing, security considerations, and recent updates in ACH rules that impact debit transactions. Real-world examples and a handy FAQ section will help answer common questions.

What Does ACH Debit Mean?

ACH debit refers to an electronic bank payment that pulls funds from a payer’s account and transfers them to a payee’s account via the ACH network. In other words, an ACH debit is a withdrawal initiated by the recipient (with the payer’s permission) through the Automated Clearing House system.

It is the opposite of an ACH credit, where the sender pushes funds to the receiver. ACH debits are sometimes called direct payments or direct debits.

For example, if you set up automatic bill pay for your electricity bill, the utility company will initiate an ACH debit to pull the amount due from your checking account each month.

The ACH Network is a U.S. electronic payment network regulated by Nacha (National Automated Clearing House Association) and the Federal Reserve system.

It processes both credit and debit transactions.

Common examples of ACH debit transactions include automatic payment of mortgages, utility bills, insurance premiums, and subscription services. In all these cases, the customer has given authorization for the business to withdraw funds when payments are due.

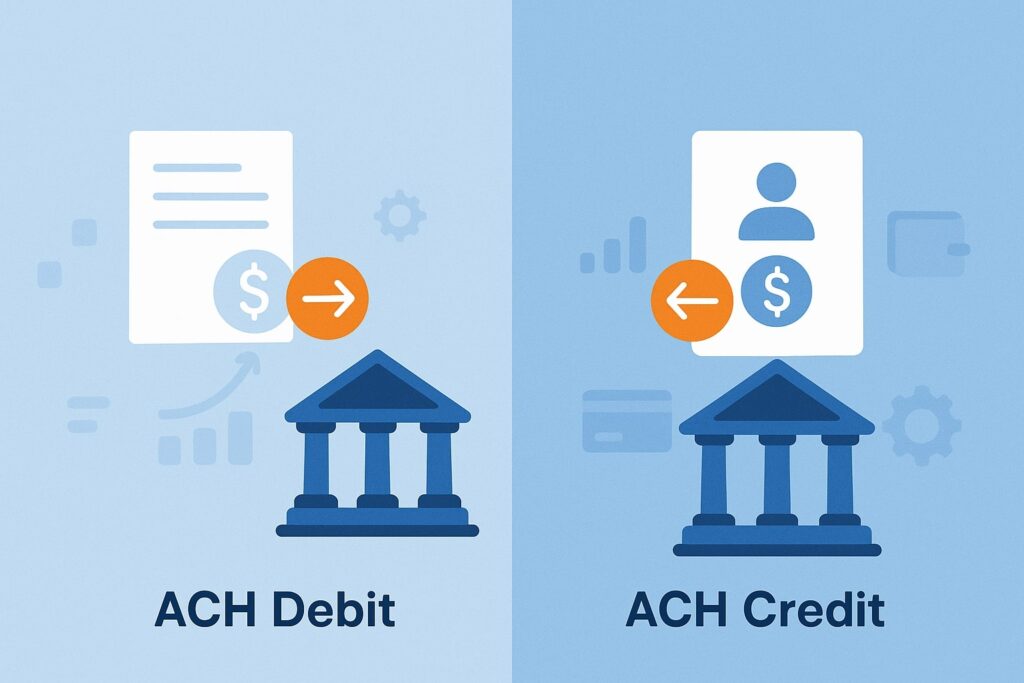

ACH Debit vs. ACH Credit

It’s useful to compare ACH debits and credits, since they are two sides of ACH payments.

An ACH credit is initiated by the payer and pushes money to the recipient (for instance, a business paying a vendor or an employer depositing salaries).

An ACH debit, by contrast, is initiated by the recipient (payee) and pulls money from the payer’s account (for example, a company pulling a customer’s monthly fee). Both types go through the same ACH network, but the flow of funds is reversed.

Below is a quick comparison of key differences between ACH debit and ACH credit:

| Aspect | ACH Debit (Pull Payment) | ACH Credit (Push Payment) |

|---|---|---|

| Initiated by | Payee (recipient of funds), with payer’s authorization | Payer (sender of funds) initiates |

| Typical uses | Recurring bills, subscriptions, invoice payments (collecting from customers) | Payroll direct deposit, vendor payments, refunds (sending to others) |

| Fund movement | Funds withdrawn from payer’s account and credited to payee’s account | Funds sent from payer’s account and deposited in recipient’s account |

| Timing | Usually next-day settlement (ACH debits can’t be scheduled more than 1 day ahead by rule); same-day possible | Often next-day; can be same-day or up to 2 days (most credits also settle within 1-2 days) |

Nacha’s rules ensure ACH debits move quickly – a debit transaction cannot have a settlement date more than one banking day in the future.

In practice, that means most ACH debits settle by the next business day (and many can settle the same day). ACH credits can be scheduled slightly further out (commonly one or two days), but they too typically settle within one or two days.

How ACH Debit Payments Work

ACH debits involve a few key players and steps from start to finish. Here’s an overview of how an ACH debit transaction works:

- Authorization by the Payer: The process begins with the customer (payer) authorizing the business to debit their account. This is usually done via a signed form or electronic agreement.

Businesses must obtain this prior authorization and keep a record of it, as required by Nacha rules. For example, a customer might fill out an online form giving a gym permission to withdraw a membership fee each month. - Initiation by the Business (Originator): When payment time arrives, the business – known as the Originator in ACH terms – creates a payment instruction to pull the specified amount from the customer’s bank account.

This instruction is sent to the business’s bank, which is the Originating Depository Financial Institution (ODFI). - Clearing through the ACH Network: The ODFI bundles the transaction into an ACH file and forwards it to an ACH Operator (either the Federal Reserve or The Clearing House’s network).

The ACH operator acts as the central clearinghouse – it sorts and routes the transaction to the customer’s bank based on the account information. - Customer’s Bank Receives (RDFI): The customer’s bank, termed the Receiving Depository Financial Institution (RDFI), receives the ACH debit entry and debits the customer’s account for the payment amount. Essentially, the funds are withdrawn from the customer’s account at this stage.

- Settlement and Credit to Business: The ACH network ensures that the funds are transferred to the business’s bank. The ODFI receives the funds and credits the business’s account, completing the transaction.

Settlement between banks typically happens within one business day. The business then sees the payment deposited in its account.

Throughout this process, everything is handled electronically and in batches. ACH transactions are processed in batch cycles throughout the day rather than instantly, but they move swiftly.

In fact, as of recent years, about 80% of ACH payments settle within one business day or less thanks to improvements like Same Day ACH. For businesses, this means ACH debits offer both automation and reasonably prompt fund transfers.

Benefits of ACH Debit for Businesses

ACH debit payments offer several advantages that make them attractive to businesses. Key benefits include:

- Lower Costs – ACH transactions tend to be very inexpensive compared to other payment methods. Businesses can save on fees by using ACH instead of credit cards (which carry percentage-based fees) or wire transfers.

In many cases, ACH payments are free or only a few cents each, saving money on each transaction. - Reliable Cash Flow – With ACH debits, payments can be automated on a schedule, which helps ensure on-time payments. This improves cash flow predictability.

For example, a company can have all customers’ accounts debited on the first of the month, virtually guaranteeing the revenue arrives as expected. It also reduces the chance of late payments or missed bills. - Time Savings & Efficiency – ACH debits remove much of the manual work from payment collection. No paper checks to handle, and no need to follow up with customers each billing cycle.

Once a customer is set up on ACH autopay, billing becomes hands-off. This streamlines operations and reduces administrative overhead (fewer invoices to chase and deposits to make). The electronic records also simplify accounting and reconciliation. - Improved Customer Experience – Many customers appreciate the convenience of automatic payments. They only have to provide their bank details and consent once, and then they don’t have to worry about forgetting a payment.

Offering ACH debit as an option can increase customer satisfaction and loyalty, since it makes paying easier. It’s a win-win: customers avoid late fees and companies get paid on time. - Reduced Payment Failures – Bank account numbers rarely change, whereas credit cards can expire or get replaced often. This means recurring ACH payments have a lower failure rate over time compared to recurring card charges.

ACH debits also bypass issues like postal delays or lost checks. Overall, the payment success rate is high, and businesses spend less effort resolving payment issues.

It’s worth noting that ACH payments are extremely popular in the U.S. today – in 2023 there were over 15.2 billion consumer ACH debit payments for paying bills and other purposes. In short, ACH debits provide a cost-effective, efficient way for businesses to collect the money they’re owed.

Potential Drawbacks and Limitations

While ACH debits have many benefits, businesses should be aware of a few limitations or challenges:

- Takes Time to Clear – ACH payments aren’t instant. They typically settle the next business day, not in real-time. This means if you pull a payment on Friday, you won’t have the funds until Monday in most cases.

Same Day ACH can speed this up, but cut-off times apply. Businesses must plan around the 1–2 day clearing time. - Risk of Insufficient Funds or Returns – If a customer doesn’t have enough balance, the ACH debit can bounce (similar to a bounced check). You might not find out until a day or two after initiating the debit that it was returned for insufficient funds or other errors.

Additionally, customers can dispute unauthorized or incorrect ACH debits, which can result in a reversal of the payment. Consumers have up to 60 days to report an unauthorized debit and have it reversed. So, there is a window during which a payment could be clawed back. - Requires Authorization and Bank Info – You cannot just start pulling funds; you need the customer’s permission and their bank routing/account number. Obtaining and securely storing this information is an extra step compared to, say, sending an invoice for the customer to pay.

Some customers may be hesitant to share bank details or might prefer to pay manually. There’s also an administrative responsibility to keep authorization records and to stop debits if a customer revokes permission. - Potential Overdrafts or Errors – Customers need to be aware of when ACH debits will hit their account to avoid overdrafts. If the timing isn’t communicated, a debit could catch someone off guard and overdraw their account.

Additionally, while errors are infrequent, they can happen (for example, a duplicate debit). However, in case of a mistake, the customer can dispute it and the error can be corrected through the ACH return process. Businesses should be prepared to handle any such customer complaints or refund requests promptly.

Despite these considerations, many of these risks can be managed with good practices. Clear communication with customers (like notifying them of upcoming debits), verifying bank info, and using account management tools can mitigate most issues. For most companies, the efficiency gains of ACH debit far outweigh the drawbacks.

How to Set Up ACH Debit Payments

Setting up ACH debit payments for your business involves a few steps, but many banks and payment processors make it straightforward:

- Establish an ACH Service: First, ensure you have the capability to send ACH transactions. This could be through your business bank (sign up for their ACH origination service) or via a third-party payment processor that supports ACH. Many billing and accounting software platforms also offer ACH payment integration.

- Obtain Customer Authorization: Before debiting any account, get the customer’s explicit permission. Have them sign an ACH authorization form (paper or electronic) that clearly states the amount (or how it’s determined), timing, and account to be debited.

For consumer accounts, the authorization must be written or electronically recorded and readily understandable. Keep these authorizations on file – they are your defense in case of any dispute. - Collect Bank Account Details: You’ll need the customer’s bank routing number and account number from a check or directly from them.

Accuracy is crucial – one wrong digit will result in a failed payment. Some businesses perform a test transaction (like a $0.01 micro-deposit) to verify the account. Make sure to handle this sensitive information securely (follow data protection best practices). - Initiate the ACH Debit: Using your bank’s online portal or your payment software, enter or upload the payment details.

Specify whether it’s a one-time debit or recurring. Double-check the amount and schedule. Submit the transaction before the bank’s cut-off time for the desired settlement date. If it’s recurring, the system will automate future draws as scheduled. - Monitor and Manage: Confirm that the payment was successful by checking the next day’s transaction report or your bank account. If an ACH debit is returned (e.g. NSF or account closed), you’ll get a return code notification.

You may then need to contact the customer and try again or arrange another payment method. Also, if a customer revokes authorization or their bank account changes, update your records immediately to avoid errors.

By following these steps, a business can start accepting ACH debit payments in a compliant and smooth manner. It’s advisable to start with a small number of transactions and become familiar with the process and reports.

Over time, ACH processing will likely run in the background, saving you time and ensuring you get paid in a timely fashion.

Security and Fraud Considerations

Security is a common concern when dealing with bank payments, but the ACH system has proven to be very safe and reliable for businesses and consumers alike. Here are some points to consider regarding ACH debit security:

- Safety Compared to Checks: ACH debits are generally safer than traditional paper checks. With electronic payments, there’s no physical document that can be stolen or altered, and sensitive bank information isn’t exposed on pieces of paper.

Checks are actually the payment method most prone to fraud – in 2024, 63% of organizations reported incidents of check fraud, versus only 38% reporting ACH debit fraud. Moving to ACH can significantly reduce the risk of payment fraud. - Customer Protections: Consumers are protected by regulations in the event of unauthorized ACH withdrawals. If a fraudulent or incorrect debit hits a consumer’s account, they can dispute it with their bank.

The bank will reverse the transaction after an investigation, as long as the customer reports the issue in a timely manner (typically within 60 days of the statement). This consumer protection framework means customers can trust ACH debits, and it encourages businesses to adhere strictly to authorization rules. - Business Safeguards: For business accounts, the dispute timeframe is much shorter (usually only 1–2 days for unauthorized debits), so businesses often use additional safeguards.

Banks offer services like ACH debit blocks or filters – these allow a company to prevent any unknown ACH debits from hitting their account. If you’re worried about someone pulling funds from your business account, talk to your bank about setting up blocks or approval filters for ACH. - Fraud Prevention Best Practices: When you’re the one originating ACH debits, you should implement best practices to prevent fraud and errors.

This includes verifying customer bank details (to avoid typing mistakes or invalid accounts), using secure systems to store data (Nacha rules mandate encrypting stored account info for larger entities), and monitoring your ACH transactions.

Unusually high return rates or patterns can indicate a problem. Also, always honor customer requests to cancel an authorization promptly – continuing to debit after revocation is not only against the rules but could be seen as fraudulent. - Nacha Rules and Updates: The ACH Network is continuously improving security. Nacha regularly updates its rules to combat fraud trends.

For example, in recent years they implemented requirements for account verification for online ACH debits to reduce fraud on WEB transactions, and they are planning new monitoring requirements for banks to detect suspicious activity.

Staying informed about such rule changes (via your bank or Nacha’s resources) will help your business remain compliant and secure.

In summary, ACH debit transactions are highly secure, especially when both parties (you and your customer) take basic precautions. By following the rules, using available bank security tools, and keeping open communication, businesses can enjoy the efficiency of ACH debits without compromising on safety or trust.

Frequently Asked Questions (FAQ)

Q1: How long do ACH debit payments take to clear?

A1: Most ACH debits clear very quickly – typically by the next business day. In many cases, if a payment is initiated on a Monday, the funds will settle and be in the recipient’s account by Tuesday (assuming no bank holidays).

Thanks to enhancements like Same Day ACH, some debits can even clear the same day they are initiated. In fact, as of recent data, roughly 80% of ACH payments settle within one day or less. However, there are a few caveats:

Q2: Can an ACH debit payment be reversed or disputed?

A2: Yes, ACH debits can be reversed under certain conditions. If a mistake or unauthorized transaction occurs, the ACH network has processes to correct it:

- By the bank (RDFI): If you, as an account holder, dispute a debit as unauthorized, your bank can return the transaction and refund you, provided you make the claim in time. Consumers usually have up to 60 days to report an unauthorized ACH debit.

Business accounts have a much shorter window (typically 1–2 days). The bank will have you sign an affidavit of unauthorized debit, and the transaction will be reversed with an ACH return code. - By the originator (ODFI): Reversals can also happen if the company realizes an error (for example, duplicate billing or wrong amount). ACH rules allow originators to initiate a reversal entry within 5 business days in cases of errors (with appropriate notification to the receiver).

Keep in mind, if a legitimate ACH debit is returned (say a customer had insufficient funds or disputes a legit charge), the business may reach out to collect payment by other means.

But the network does prioritize consumer protection – unauthorized or fraudulent debits can be clawed back. For businesses, this underlines the importance of having proof of authorization for every debit.

Q3: How is an ACH debit different from a debit card payment?

A3: This is a great question because the terminology can be confusing. Both ACH debits and debit card transactions pull money from a checking account, but they go through different payment channels:

- An ACH debit uses the bank’s routing and account number and goes through the Automated Clearing House network as described in this guide. It usually is set up in advance (like bill pay) and doesn’t involve any card.

- A debit card payment (e.g., you swipe your debit card at a store or enter the card number online) goes through the card networks (Visa, MasterCard, etc.).

Even though it ultimately draws from your bank account, it is processed like a card transaction, with real-time authorization and often fees similar to credit card processing for the merchant.

In short, ACH is a direct bank-to-bank transfer mechanism, whereas a debit card is an instrument tied to your bank account but processed via the card system. When we talk about ACH debits in this article, we mean the bank transfer type (no physical card involved).

Q4: Are there fees for ACH debit transactions?

A4: One big advantage of ACH is its low cost. ACH payments are often free or very cheap for transfers and bill payments. Banks typically charge either no fee or just a small flat fee (like a few cents) per ACH transaction for business accounts.

Unlike credit card payments which might cost a few percent in processing fees, ACH costs only pennies or may even be included for free in your banking package.

It’s always good to check your bank’s policy – some might have a nominal charge or monthly fee for ACH services – but overall ACH is one of the most affordable ways to move money.

Conclusion

ACH debits play a vital role in the U.S. payments landscape, offering businesses a powerful way to collect money electronically with speed and efficiency. We’ve explored what ACH debit means – essentially an authorized pulling of funds from a customer’s bank account – and seen how it works within the banking system.

For business owners, understanding ACH debit is more than just a technical matter; it’s about unlocking a payment method that can reduce costs, improve cash flow, and streamline operations.

With an ACH debit, a business can ensure recurring revenues arrive on time, avoid the pitfalls of paper checks, and provide a convenient payment option that many customers appreciate. The U.S. ACH Network is well-established and continues to grow, handling tens of billions of transactions each year.

It has kept pace with modern needs by introducing faster settlements and tighter security measures. By focusing on people-first practices – such as obtaining clear authorizations and safeguarding customer data – companies can use ACH debits in a trustworthy manner that enhances their reputation and compliance.

In summary, ACH debits (also known as direct payments) provide a meaningfully efficient way to transfer funds from your customers to your business. They answer the question of “what does ACH debit mean” with tangible benefits: cost savings, reliability, and ease of use.

As with any financial tool, one should remain informed and diligent – keep up with Nacha rule updates, ensure security steps are in place, and maintain open communication with customers.

Armed with the knowledge from this in-depth guide, business owners can confidently incorporate ACH debit into their payment strategy, leveraging it to support their growth while delivering a smooth payment experience for their clientele.

Leave a Reply