By Rinki Pandey August 3, 2025

Every day, billions of dollars move between U.S. bank accounts through the Automated Clearing House (ACH) network. ACH payments power everything from employee paychecks to vendor invoices to consumer bill payments. In 2024 alone, the ACH network processed 33.6 billion payments (over $86 trillion in value), making it a backbone of the U.S. financial system.

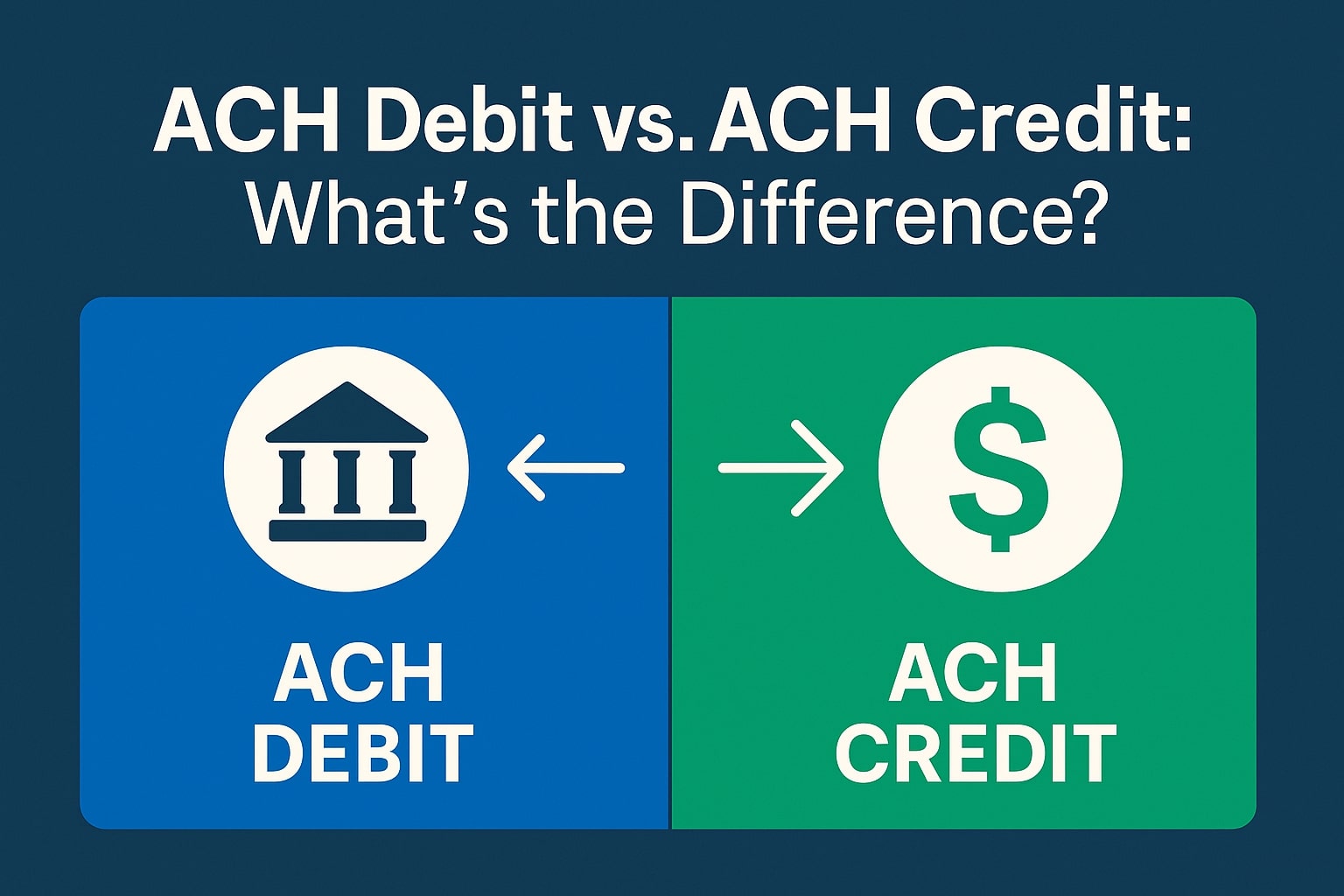

Yet many business owners remain unclear on the nuances of ACH transactions – particularly the difference between ACH debits and ACH credits. These terms may sound technical, but the concept is straightforward: an ACH credit pushes funds into an account, while an ACH debit pulls funds out of an account.

In this article, we’ll demystify ACH transfers and explain in detail how ACH debits and credits work. We’ll also compare ACH transfers to other payment methods like wire transfers and credit card payments, discuss U.S. regulations and recent data, outline practical use cases along with benefits and risks, and answer common questions for business owners. By the end, you’ll have a clear understanding of when to use ACH debit versus ACH credit and how to leverage them for your business’s needs.

Understanding ACH: The Automated Clearing House Network

ACH stands for Automated Clearing House, which is the primary electronic payment network in the United States. It’s a nationwide system through which banks and credit unions send each other batches of electronic transfers. Instead of processing payments one by one in real time, ACH transactions are accumulated and processed in groups (batches) at scheduled intervals.

This batching makes ACH highly efficient for handling large volumes of payments. In fact, the ACH network handles more than 30 billion transactions each year, covering everything from payroll direct deposits and bill payments to business-to-business (B2B) transfers.

The ACH network is governed by the National Automated Clearing House Association (Nacha) and regulated by the Federal Reserve. There are two central ACH operators (the Federal Reserve Banks’ ACH service and the private Electronic Payments Network), which work together to route transactions to the correct receiving banks.

The network reaches all U.S. banks and credit unions, ensuring virtually any U.S. bank account can send or receive an ACH payment. Because of this reach, ACH is ubiquitous in the U.S. financial landscape – for example, roughly 92% of American workers are paid via ACH direct deposit (an ACH credit), and almost all Social Security and tax refund payments use ACH.

In summary, ACH is an electronic funds transfer system that moves money between bank accounts in the U.S. It’s fast (though not instantaneous), cost-effective, secure, and ideal for recurring or scheduled payments. There are two main types of ACH transactions – ACH credits and ACH debits – which we will explore next.

What Is an ACH Credit?

An ACH credit is an electronic payment that allows a person or organization to send money to another bank account. In an ACH credit transaction, the sender (also called the “originator”) initiates the transfer of funds from their account to the recipient’s account. In simple terms, an ACH credit is like a digital “push” of money.

How ACH Credits Work: The payer instructs their bank (or payment processor) to transfer a certain amount to the payee’s bank account. The payer’s bank (the Originating Depository Financial Institution, or ODFI) bundles this request into an ACH batch along with others, and sends it through the ACH network.

The ACH operator then routes the transaction to the recipient’s bank (the Receiving Depository FI), which credits the funds to the recipient’s account. Settlement between banks typically happens within 1–2 business days, though it can be as fast as the same day if sent via same-day ACH. From the sender’s perspective, an ACH credit is analogous to writing a check, except it’s all digital and processed through the banking system.

Common Examples: ACH credits are extremely common in business and daily life. Here are typical use cases:

- Payroll Direct Deposit: Employers pay employees via ACH credit – on payday, funds are pushed directly into workers’ bank accounts (this is why employees often see “Direct Deposit ACH” on their statements). For instance, on Friday payday, the money is usually available in the employee’s account by morning of that day.

- Vendor or Supplier Payments: Businesses pay suppliers, contractors, or service providers electronically using ACH credits instead of mailing paper checks. This streamlines accounts payable and is safer and faster than check payments.

- Government Payments: Government agencies use ACH credits to disburse funds, such as tax refunds or Social Security benefits, directly to citizens’ bank accounts.

- Consumer Bill Pay and P2P Transfers: When you use your bank’s online bill pay to send money (for example, paying your utility bill or sending money to a friend through an app like Zelle or CashApp), the bank likely issues an ACH credit that pushes funds from your account to the biller or your friend.

The key feature of ACH credits is control for the payer – the payer decides when and how much to send, thereby “pushing” the payment out. From the recipient’s viewpoint, an ACH credit is a deposit coming in (they don’t have to take any action except perhaps providing their account info to the sender). ACH credits give businesses and individuals a reliable, low-cost way to transfer money while controlling the timing of outflows.

What Is an ACH Debit?

An ACH debit is the opposite of an ACH credit – it is an electronic payment that pulls funds from a payer’s bank account and transfers them to another account. In an ACH debit transaction, the recipient (the party receiving the money) initiates the transfer by requesting to withdraw money from the payer’s account (with proper authorization). In other words, an ACH debit is a “pull” of funds from the payer.

How ACH Debits Work?

To use an ACH debit, the party receiving payment (often a business or service provider) must first obtain authorization from the payer to pull the funds. This authorization could be a signed form, an online agreement, or some consent that meets Nacha’s requirements (for consumer accounts, authorizations must be in writing or similarly authenticated).

Once authorized, the recipient’s bank initiates the debit entry through the ACH network. The payer’s bank account is debited (funds taken out) and the recipient’s account is correspondingly credited after the ACH transaction clears. Just like credits, ACH debits are processed in batches. The debit may hit the payer’s account on the due date and typically settles within 1–2 business days (or the same day if using same-day ACH).

Common Examples: ACH debits are widely used for recurring payments and collections. Typical scenarios include:

- Automatic Bill Payments: Companies that bill customers on a recurring basis often use ACH debits (sometimes called “direct debits”). For example, a utility company or subscription service can pull the amount due directly from a customer’s bank account on the due date (after the customer has signed up for autopay). This spares the customer from having to remember to pay, and ensures the business gets paid on time.

- Business-to-Business Collections: In B2B settings, an agreement might allow one business to pull funds from a partner or client’s account. For instance, a wholesale supplier could debit a retailer’s account for an invoice on the agreed date. Many one-time B2B payments are also done via ACH debit, especially when the payer prefers the recipient to initiate the transaction for convenience.

- Tax Payments to Government: The IRS and state tax authorities often use ACH debits for electronic tax payments. When businesses or individuals schedule tax payments (like quarterly estimated taxes or payroll tax remittances), they authorize the government to withdraw the amount due directly from their account on a specified date.

- Mortgage and Loan Payments: Many lenders let borrowers set up ACH debit (direct withdrawal) so that monthly mortgage or loan payments are automatically pulled from the borrower’s bank account. This ensures on-time payment without the borrower manually sending money each month.

From the payer’s perspective, an ACH debit means trusting the payee to initiate the payment. It requires giving your bank details and permission to another party. As long as it’s a trusted party (and authorization is properly obtained), ACH debits provide convenience – you “set it and forget it” for recurring obligations.

For the recipient (e.g., a business collecting money), ACH debits offer assurance of payment because they can pull funds when due (though they must handle situations like insufficient funds or revoked authorizations appropriately).

Key Differences Between ACH Credit and ACH Debit

ACH credits and ACH debits are two sides of the same coin – both move money between bank accounts via the ACH network – but they differ in who initiates the transaction and how the funds flow. Here are the key differences:

- Initiation (Who Starts the Transaction): In an ACH credit, the payer (sender of funds) initiates the payment. In an ACH debit, the payee (receiver of funds) initiates the transfer by requesting the funds. Another way to put it: ACH credit = the payer pushes money out; ACH debit = the payee pulls money in.

- Direction of Funds: ACH credit transactions transfer money from the originator’s account to the recipient’s account, whereas ACH debit transactions transfer money from the payer’s account to the initiator’s account (i.e. the recipient is pulling from the payer. Practically, this means an ACH credit results in a deposit to the recipient, while an ACH debit results in a withdrawal from the payer.

- Typical Use Cases: ACH credits are commonly used for payments out: e.g. payroll deposits, vendor payments, refunds, or person-to-person payments where the sender triggers the transfer. ACH debits are commonly used for collections: e.g. recurring bill payments, subscription charges, or any scenario where the payee is authorized to collect money from customers or partners. Businesses often use ACH credits to pay what they owe, and ACH debits to collect what they are owed.

- Authorization Requirements: Both ACH credits and debits require the originator to have the necessary bank details (routing and account number) and authorization. However, the authorization is especially critical for ACH debits, because you are pulling money from someone else’s account. Nacha rules mandate that ACH debits from consumer accounts must be authorized in writing or similarly verifiable form, and businesses must retain proof of that authorization. For ACH credits, the act of the sender initiating the payment generally implies authorization (for example, an employer has an agreement with an employee to pay salary via direct deposit).

- Impact on the Consumer/Business: If you are on the sending end, an ACH credit means you send out money (your account gets debited, the other side is credited). If you’re on the receiving end of an ACH credit, you see a deposit. With an ACH debit, if you’re the one paying, your account gets debited by someone else (money taken out) – it feels like an automatic withdrawal. If you’re the receiver of an ACH debit, you get the money and the payer’s account is charged. In short, ACH credit = you pay someone; ACH debit = someone pays you (by taking from the payer’s account).

- Processing Timing: Historically, ACH credits and debits had slightly different timing rules. In modern ACH operations, both credits and debits can settle quickly (often next day or even same-day). One nuance is that ACH credits can be future-dated (an employer might initiate payroll credits a day or two in advance for settlement on payday), whereas ACH debits are typically intended to be processed either same-day or next available day by the due date.

According to Nacha, many ACH credit transactions settle either the same day or next banking day, but credits can be scheduled up to two business days out if desired; ACH debits, on the other hand, are usually settled either same-day or next day by rule. For most business purposes, however, both ACH debits and credits move on similar timelines (described in more detail in the Processing Times section below).

It’s worth noting that regardless of type, ACH payments are not instant. They are batch-processed and typically clear in 1–3 business days, though Same Day ACH options exist. We’ll discuss speed and how ACH compares to other methods next.

But first, keep this simple distinction in mind: ACH credit = “push” payment (payer-initiated), ACH debit = “pull” payment (payee-initiated). Both are secure, efficient ways to transfer money electronically; the choice depends on who is initiating the transaction and the business context.

ACH vs. Wire Transfers

How do ACH payments stack up against wire transfers, another common method for moving money? While both ACH and wire transfers are forms of electronic funds transfer (EFT), they differ significantly in speed, cost, and use cases.

Speed: Wire transfers are typically much faster than ACH. A domestic wire transfer is often completed within minutes or a few hours the same day (as long as it’s sent before the bank’s cutoff. ACH transfers usually take 1–3 business days to fully settle, since they go through batch processing and clearing cycles.

For instance, paying a vendor by ACH might result in the funds showing up in their account the next day or the day after, whereas a wire could get it there within the same day. If timing is critical – say, a closing payment on a house or an urgent large purchase – wire transfers have the advantage. ACH is catching up in speed with Same Day ACH (which can settle payments within hours on the same business day), but wires are still considered the go-to for immediate, time-sensitive transfers.

Cost: ACH transfers are far cheaper than wire transfers. ACH payments are usually low-cost or even free for the sender, especially through banks or business payment services. Banks often charge nothing or just a few cents to a few dollars per ACH transaction. In contrast, wire transfers are expensive, typically costing a flat fee that can range from $20 to $35 (domestic outgoing) per transfer, sometimes more for international wires. Receiving banks may also charge a fee for incoming wires (often $10–$20). Because of these costs, wiring money is not cost-effective for frequent or low-value transactions; ACH wins on cost efficiency.

Reversibility and Risk: ACH transfers, being slower and batch-processed, have a window in which they can be reversed or recalled under certain conditions. If an error is discovered (like a duplicate payment or wrong amount), ACH rules allow initiating a reversal within a short time frame (generally within 5 business days for errors in credits).

Consumers also have protections for unauthorized ACH debits – a consumer can dispute an unauthorized debit and have it refunded if reported within 60 days, per Regulation E. Wire transfers, on the other hand, are largely irreversible once executed.

Because wires move so quickly, it’s very difficult to get money back after it’s sent; a mistaken or fraudulent wire often cannot be undone unless caught immediately. In fact, scammers often target wire transfers for this reason, whereas ACH transactions (with their slight delay) are less common targets of fraud and can be intercepted if flagged promptly.

Use Cases: ACH and wire transfers serve different purposes in business:

- ACH is ideal for routine, non-urgent payments, especially recurring ones. Paying vendors on regular terms, running payroll, collecting subscription payments, and transferring funds between your own accounts are all well-suited for ACH. It shines when you need a cost-effective solution and timing is predictable (a few days is fine). ACH is typically domestic (U.S.-only) – while there is a form of international ACH, cross-border payments are usually done via wires or other networks.

- Wire transfers are reserved for situations where speed or finality is paramount. Examples include sending a large payment that must arrive the same day (e.g., real estate closings, urgent supplier payments), or sending money internationally to a foreign bank. Businesses might use wires for one-off large transactions or when the payee cannot accept ACH. Wires are also used when immediate clearing is needed despite the higher cost.

Summary of ACH vs Wire: ACH transfers are slower but vastly cheaper (often free or pennies) compared to wires, which are fast but expensive. ACH offers more flexibility to reverse or correct errors in the short term, whereas wires are essentially final once sent.

In terms of security, both are secure networks, but wire fraud and scams (like fake supplier instructions) are a known risk due to irreversibility, whereas ACH fraud rates are very low in comparison (only about $0.08 of fraud per $10,000 in ACH payments, according to a Federal Reserve study).

For a business owner, this means: use ACH for most day-to-day payments where cost savings matter and a short wait is acceptable; use wire transfers sparingly for high-priority, immediate needs or international payments.

ACH vs. Credit Card Payments

Many businesses also wonder whether they should encourage bank payments via ACH or use credit card processing for customer payments. Credit card transactions (through Visa, MasterCard, etc.) are very different from ACH, even though both are electronic. Here’s how they compare:

- Cost and Fees: This is one of the biggest differentiators. Credit card payments carry higher fees for merchants – typically around 2% to 3.5% of the transaction amount, plus possibly a per-transaction fee. These fees include interchange fees (to the card-issuing bank), assessment fees (to the card network), and processor markups. On a $1,000 payment, a 3% fee means $30 cost to the business. ACH payments, by contrast, are extremely low-cost.

ACH fees are often a flat amount (e.g. $0.20 to $1.50 per transaction) or a very small percentage (often under 1%). In many cases, banks don’t charge anything for basic ACH transfers, or a payment processor might charge a nominal fee like $0.25 per ACH transaction – which is pennies compared to credit card costs. For businesses handling large payments or recurring billing, ACH’s cost advantage can save a lot of money. Bottom line: ACH is far more cost-effective than credit cards for accepting payments, especially high-dollar or frequent transactions. - Speed and Availability of Funds: Credit card transactions have instant authorization, meaning when a customer pays by card, you immediately get approval or denial from the network (the card is charged in real time). This is great for retail or e-commerce, as you can confirm payment on the spot. However, the actual funds from a credit card sale typically take a day or two to settle into the business’s bank account (the merchant receives a batch payout from the processor, usually the next business day or so).

ACH transactions settle in 1-3 days, as noted earlier, and do not provide instant confirmation at the time of transaction. For example, if a customer pays via ACH (say, entering their bank info on an invoice form), the business won’t know immediately if the payment will clear – it may take a day to find out if it was successful or if it failed (e.g., due to insufficient funds). In scenarios like online shopping carts or on-demand services, this lack of instant authorization makes ACH impractical. But for invoiced B2B transactions or recurring payments, waiting a day or two is usually fine. - Authorization and Guarantee of Funds: Because credit cards are processed in real time, they come with a guarantee of funds at purchase (if the transaction is approved, the merchant can expect to get paid, barring chargebacks). The card network and issuing bank handle the risk of the customer’s credit. With ACH, there is no instant guarantee – a payment could bounce if the account has insufficient funds or if the account info was wrong.

In fact, ACH debits can be returned for non-sufficient funds (NSF) typically a day or two after initiation. This is why ACH isn’t used at point-of-sale for say, buying a coffee – there’s a risk the payment won’t go through. For billing known customers or businesses, however, this risk can be managed or is acceptable. - Chargebacks and Disputes: Credit cards allow customers broad rights to dispute charges (chargebacks), which can be costly and time-consuming for businesses. A customer can often initiate a chargeback up to 60-120 days after a transaction for various reasons (fraudulent use, dissatisfaction, etc.), and the merchant may lose the funds plus pay a chargeback fee. ACH transactions have a lower incidence of disputes. While consumers can dispute an unauthorized ACH debit (within 60 days) or an error, the overall chargeback (return) rates on ACH are typically lower than on cards.

ACH debits that are properly authorized face less frequent chargebacks, and business-to-business ACH transactions have even fewer dispute mechanisms (since Reg E protections apply only to consumer accounts). For a business, this means ACH payments carry less risk of surprise reversals compared to credit card payments – as long as you have proper authorization and are dealing with legitimate transactions. - Customer Convenience and Usage: Credit cards are widely used and convenient for customers, especially for one-time purchases or retail scenarios. Most customers know how to pay with a credit or debit card by entering the card number, and many prefer it for the rewards points or simply habit. ACH payments require the customer’s bank routing and account number, which not all customers have memorized or are willing to input, and an ACH debit requires them to authorize the transaction. There can be a bit more friction getting a customer to pay via ACH, unless it’s a situation where they expect to (like setting up direct debit for a utility or a B2B invoice).

However, for large payments, some customers may prefer ACH (to avoid maxing credit limits or incurring card fees). Also, ACH is great for recurring payments – once the customer signs an ACH authorization once, future payments can be pulled automatically, which can be even more convenient than entering a card each time (and there’s no card expiration to worry about). Each method has its place: credit cards excel in immediate, point-of-sale transactions and consumer-driven purchases, while ACH shines for recurring billing, high-value transactions, or situations where cost savings are important. - Transaction Limits: Credit card payments are constrained by the cardholder’s credit limit or daily transaction limits. This can make very large B2B payments difficult or impossible to put on a card. ACH transfers generally accommodate much larger amounts. For example, Nacha currently allows up to $1 million per payment for Same Day ACH transfers, and standard ACH transfers can be even higher (practically limited by agreements with your bank or ACH provider). Businesses often use ACH for large invoice payments or payroll runs that would be impractical with cards.

In summary, ACH vs Credit Card comes down to cost vs speed/convenience. ACH is cheaper, often just a flat few cents per transaction, and it’s very secure for large and repeated payments. Credit cards are faster at point of sale and easier for spontaneous purchases, but with significantly higher fees (a few percent per transaction) and higher risk of chargebacks.

For a business owner, it might make sense to offer both: let customers pay by card for convenience, but encourage ACH for large invoices or recurring subscriptions by perhaps offering it as a “pay by bank (no fee)” option. Many businesses find that offering ACH payments (bank transfer) alongside card payments can reduce processing costs and give customers more choice.

(Note: Another comparison is ACH vs paper checks. In short, ACH is superior to checks in efficiency and security – paper checks are slow, labor-intensive, and are actually the payment method most prone to fraud. Migrating from paper checks to ACH can save money and reduce fraud risk for businesses. So wherever you can use ACH in lieu of sending or receiving checks, it’s usually advantageous.)

U.S. Regulations, Security, and Compliance for ACH

Because ACH transactions involve moving money between bank accounts, they are subject to a robust framework of rules and regulations that protect both consumers and businesses. Here are the key points business owners should know about the regulatory and security environment of ACH:

- Nacha Operating Rules: The ACH network is governed by the Nacha Operating Rules, which all participating financial institutions and ACH originators (businesses initiating ACH entries) must follow. These rules cover everything from formatting of transactions to deadlines, and importantly, authorization requirements. For example, Nacha rules require that businesses obtain proper authorization from customers before initiating ACH debits (this could be a signed ACH authorization form or an electronic consent) and retain proof of those authorizations for at least two years after they end.

There are standardized codes (SEC codes) for different types of ACH entries (PPD for consumer pre-authorized payments, CCD for corporate payments, etc.), but you don’t need to know all codes – your bank or payment processor will use the appropriate ones. The key takeaway is that if your business is going to pull money from a customer’s account (ACH debit), you must have clear permission. This protects customers and also protects your business from unauthorized transaction disputes. - Federal Regulation E: When dealing with consumer bank accounts, Regulation E (Electronic Fund Transfer Act) provides certain protections. For instance, if a consumer sees an unauthorized ACH debit from their account, they have 60 days from their bank statement date to report it and get it reversed. The bank will investigate and if it truly was unauthorized, the consumer is made whole and the funds are returned (the loss ultimately falls back to the business that initiated the debit).

As a business, this means you need to be careful with consumer debits – always get authorization and keep good records, and respond promptly if a customer questions a charge. Business bank accounts are not covered by Reg E in the same way, so ACH debits on a business account have a much shorter dispute window (usually only 24–48 hours for the bank to return an item as unauthorized). Knowing your customers and maintaining good communication can mitigate issues here. - Security Requirements: Participating in the ACH network comes with data security obligations. Nacha’s rules mandate that sensitive bank account information (like customers’ account numbers) be protected. Businesses should store and transmit bank details securely (often encryption is required or recommended) and comply with any applicable standards. In addition, many banks offer ACH fraud prevention tools such as ACH blocks or filters – for example, you can block all ACH debits on your account except from certain allowed parties, which can prevent unauthorized pulls.

The good news is that the ACH system itself is highly secure and has very low fraud rates relative to other payment methods. A Federal Reserve study found ACH had one of the lowest fraud rates of any payment type (only a few cents per $10,000 transacted). By comparison, credit cards have a higher incidence of fraud and chargeback, and paper checks are notoriously vulnerable to check fraud. When you use ACH through your bank or a reputable payments provider, you benefit from bank-grade security and authentication procedures. - Compliance and Monitoring: Banks and ACH processors will often monitor ACH transactions for compliance and may have you agree to certain terms (for example, not originating fraudulent or improper ACH entries). If you’re a higher volume originator, you may need to implement annual audits or risk assessments per Nacha rules. Also, note that OFAC (sanctions) compliance applies to ACH just as it does to wire transfers – you must ensure you’re not sending payments to accounts that are on sanctions lists. Most of this is handled by banks’ screening processes, but as a business you should be aware of your transaction counterparties.

- Recent Rule Updates: The ACH network continuously evolves. For example, in recent years Nacha introduced the concept of “Standing Authorization” to make it easier to authorize recurring or future debits in different ways. And notably, as of March 2022, the per-transaction limit for Same Day ACH increased to $1 million, expanding the use of faster ACH for larger payments.

Nacha regularly updates rules to improve efficiency and safety (like account validation requirements to reduce fraud, new return codes for certain situations, etc.). It’s a good idea to stay informed via your bank or Nacha if you originate a lot of ACH payments, but for most small businesses, your bank or payment software will handle compliance in the background.

Overall, the regulatory framework ensures that ACH remains a safe and reliable network for moving money. By following best practices – obtain authorizations, use secure systems, and reconcile your payments – your business can confidently use ACH for payments. Many businesses appreciate that ACH offers security without the high fees of card networks and the oversight helps keep the system trusted.

Practical Use Cases for Businesses

ACH payments can streamline both your accounts payable and accounts receivable processes. Let’s look at some practical use cases and how businesses utilize ACH credits and debits in daily operations:

- Payroll and Employee Payments (ACH Credit): As mentioned, direct deposit via ACH credit is the gold standard for paying employees. Instead of cutting paper checks, your payroll system can issue an ACH credit to each employee’s bank account for their net pay. This ensures employees are paid on time (funds are typically available by 9 a.m. on payday) and it saves time and costs associated with printing and distributing checks. Even reimbursements for expenses can be paid to employees via ACH credit.

- Vendor and Supplier Payments (ACH Credit): Businesses often have to pay suppliers, contractors, landlords, or service providers. Using ACH credit transfers for these B2B payments is efficient. You can set up your vendors in your online banking or accounting software with their routing and account numbers, and send payments directly to their bank.

In 2024, there were over 7.3 billion business-to-business ACH payments, reflecting a growing preference by companies to pay each other electronically. This method is particularly useful for recurring vendor payments (like monthly rent or service fees) – you can schedule ACH payments on due dates so you never miss a payment. - Collecting Customer Payments (ACH Debit): If your business bills customers on a recurring basis (e.g., a subscription service, utility company, or B2B service contracts), you can offer ACH direct debit as a payment option. Customers who opt in will provide you their bank details and sign an ACH authorization. Then, on each billing cycle, you initiate an ACH debit to pull the amount owed from their account.

This is highly convenient for both parties: customers don’t have to remember to pay, and you get your cash flow consistently. Many accounting and invoicing systems (QuickBooks, etc.) now integrate ACH payment options because of the lower transaction fees compared to credit cards. - Receiving Customer-Initiated Payments (ACH Credit from Customer): Alternatively, some businesses set up online payment gateways where customers can initiate an ACH payment (essentially the customer pushes a payment via an ACH credit). For example, a customer paying an invoice might go to a payment page, enter their bank info, and trigger an ACH credit from their account to the business’s account.

The distinction from the above scenario is who initiates – here the customer is actively sending the money (like using online bill pay), which is an ACH credit to the business. This can be useful for one-time bill payments or when the customer prefers to initiate payment. - Internal Funds Transfers and Expense Management: ACH is also used by businesses to move money between their own accounts or to owners. For instance, you might sweep funds from a retail account to a main treasury account via ACH, or the business owner might take a draw that’s transferred to their personal account. These are often done as ACH credits. If you have multiple bank relationships, ACH is a simple way to consolidate funds – many banks allow linked accounts and ACH transfers to yourself either free or for a small fee.

- Tax Payments and Government Filings: Businesses can pay federal and state taxes electronically using ACH. Payroll taxes, sales taxes, and income tax estimates can all be remitted through systems like the Electronic Federal Tax Payment System (EFTPS), which uses ACH debits to pull the tax payment from your account on the scheduled date. This is safer than mailing a check and provides immediate proof of payment. Similarly, if you’re due a tax refund or incentive payment, the government may ACH credit it to your account.

- Customer Refunds or Payouts: If your business needs to pay customers – for example, refunding a purchase or paying out a claim or reward – you can use ACH credits for that as well. Many accounts payable systems can handle both vendor payments and customer refunds via ACH. It’s faster and more secure than mailing refund checks, and customers appreciate getting money directly to their bank.

In all these scenarios, ACH helps automate and simplify transactions. By using ACH, businesses reduce reliance on paper, minimize transaction fees, and improve cash flow timing. For recurring relationships (employees, regular vendors, subscription customers), ACH creates a “set it and forget it” payment flow, which reduces administrative overhead.

It’s no surprise that American businesses and government agencies rely heavily on ACH – for example, 99% of Social Security payments are via ACH rather than mailed checks. The convenience and reliability are hard to beat.

Benefits of ACH for Businesses

Why should businesses use ACH? Here are some key benefits of ACH payments:

- Significantly Lower Costs: ACH transactions generally cost pennies or a few dollars at most, regardless of the transaction size. This is a massive savings compared to credit card fees (which take a percentage cut of each sale) or wire fees. For example, a $10,000 invoice paid by ACH might cost you $1 in bank fees (or even $0), whereas a credit card payment of the same amount could cost $300 in processing fees at 3%. If you process a lot of payments, the cost savings from using ACH can directly improve your bottom line. Even compared to paper checks, ACH saves money – no check printing, postage, or manual processing costs.

- Efficiency and Time Savings: ACH automates payments. Once set up, payments can recur without manual intervention (great for payroll, subscriptions, etc.). No more writing checks, making trips to the bank, or dealing with physical mail delays. Funds move electronically from bank to bank, which speeds up the overall payment cycle. Many banks offer easy ACH origination through online banking portals, and many accounting software platforms integrate ACH for collecting customer payments – this means less data entry and easier reconciliation for your finance team.

- Improved Cash Flow Management: With ACH, you can precisely time when money leaves or enters your account. For outgoing payments (ACH credits), you know exactly which day the funds will be withdrawn and can plan around it. For incoming payments (ACH debits or customer-initiated credits), you can schedule them on due dates.

This predictability helps with cash flow forecasting. Businesses can also consolidate funds faster (transferring from sales accounts to main accounts daily via ACH, for instance) to keep their money working for them. Plus, using ACH for receivables often means you get paid faster than waiting for checks – a customer might take 2 weeks to mail a check, but only 2 days to settle an ACH. The overall result is better liquidity management. - Security and Fraud Reduction: ACH is a secure, bank-regulated network. Transactions are encrypted and authenticated, and every party (banks, businesses, processors) must follow security guidelines. Fraud does happen, but ACH fraud rates are extremely low relative to other forms of payment. In fact, ACH is often cited as having the lowest fraud rate of popular payment types. Contrast this with paper checks, which can be stolen or altered, and credit cards, which can be compromised.

Also, because ACH debits require explicit authorization, there’s a clear record of permission. Businesses can further secure themselves by using ACH debit filters (to block any unauthorized debits on their accounts) and verification services to validate customer accounts. Overall, accepting payments via ACH can lower your exposure to certain types of fraud compared to handling lots of checks or cards. - Convenience for Customers and Partners: Setting up clients or customers on ACH auto-pay can enhance their experience because it automates their payments (no missed due dates, no late fees). Employees appreciate direct deposit (no need to cash a check).

Vendors appreciate timely electronic payments (they don’t have to chase down checks). Offering ACH as an option can make your business easier to work with. Additionally, some customers prefer paying directly from their bank (especially for big amounts) to avoid putting it on a credit card – ACH accommodates that preference. - Scalability and Volume: The ACH network can handle very large volumes of transactions efficiently. If your business grows and you need to process thousands of payments, ACH can scale with you. It’s designed for batch processing, so whether you’re sending out 10 payments or 10,000 payments in a file, it’s all in a day’s work for ACH. This is why payroll processors and large billers rely on ACH. You won’t outgrow it.

In short, ACH offers cost efficiency, reliability, and automation, making it a highly attractive payment method for businesses of all sizes. Whether you’re a small business trying to cut down on credit card fees or a larger enterprise automating payables and receivables, ACH provides a robust solution.

Risks and Challenges of ACH Payments

While ACH is generally advantageous, it’s important to be aware of some risks and challenges associated with using ACH:

- Slower Settlement (Timing Risk): Traditional ACH isn’t instantaneous. If your business needs funds immediately or needs confirmation of payment right away, the 1-3 day settlement window can be a drawback. For example, if you ship goods upon receiving payment, waiting for an ACH to clear could delay fulfillment, whereas a credit card authorization is immediate. Same Day ACH mitigates this somewhat, but it may involve additional fees and still operates only during banking hours. Additionally, ACH doesn’t settle on weekends or bank holidays (payments will queue and settle on the next business day), which can be a challenge for timing around long weekends or month-end.

- Payment Failures (NSF or Errors): ACH debits can fail due to non-sufficient funds (NSF) in the payer’s account or incorrect bank information. When you pull a payment, you might not find out until a day or two later that it bounced. This can create the need for re-processing or follow-up with the customer, and possibly incur NSF fees. Likewise, if account numbers or routing numbers are entered incorrectly, payments can be rejected. It’s important to validate bank details and perhaps use account verification services (some modern ACH processors do micro-deposits or instant account verification) to reduce errors.

- Authorization Management: For ACH debits, keeping track of customer authorizations and any changes can be an operational challenge. Customers might revoke authorization or change banks, and you need a process to handle that (to avoid attempting unauthorized debits, which could lead to customer dissatisfaction or even fines under Nacha rules). You also have to securely store authorization forms or recordings. It’s wise to have clear terms in any service contract about ACH payments and how customers can cancel or update payment instructions.

- Lower Consumer Familiarity: Some customers might be hesitant to provide bank account information for ACH payments, out of privacy or security concerns. Unlike credit cards, where fraud liability is on the bank and numbers are easily replaced if compromised, bank account numbers feel more sensitive to some people. Educating customers on the security of ACH and offering it as an option (but not forcing it) can help. Over time, people have grown more comfortable with ACH (as evidenced by millions of people using direct debit for bills), but it’s a consideration in user experience.

- International Limitations: The ACH network is U.S.-centric. If your business needs to collect or send payments internationally, ACH alone won’t suffice. There are programs like FedGlobal ACH that facilitate certain international transfers via partner networks, and some countries have their own “ACH-like” systems, but you often have to rely on wire transfers or specialized payment providers for cross-border payments. This is only a challenge if you deal with cross-border transactions; for purely domestic businesses, ACH works nationwide.

- Risk of Reversals or Fraudulent Pulls: Although ACH fraud rates are low, it’s not zero. Unauthorized ACH debits can occur if a bad actor obtains someone’s bank details. For example, if an employee’s login to your payroll system was compromised, someone could attempt to redirect payments. Also, there have been cases of fraudsters tricking companies into switching supplier bank details (business email compromise scams) to divert ACH payments. Businesses must maintain internal controls – verify any requested banking detail changes and monitor account activity. The good news is banks often offer alert services for ACH transactions and the ability to return fraudulent debits if caught quickly. Still, vigilance is necessary.

- Chargeback/Dispute Handling: In the rare event a customer disputes an ACH payment (say they claim it was unauthorized), your business may have to refund and resolve it out of band, since there isn’t a robust chargeback arbitration process like credit cards have. Usually, disputes are handled by simply reversing the transaction.

If you believe a customer’s dispute is wrong (e.g., they did owe you and they are trying to claw back via the bank), you might be out of luck if it’s a consumer – banks tend to side with consumers under Reg E for unauthorized claims. This emphasizes why having authorization and communication is key. For B2B, this is less of an issue because if a business client authorized an ACH, they typically can’t just yank it back without cause (and if they do, you’ll know within 24-48 hours).

Despite these challenges, most can be managed with sound procedures and choosing the right banking partner or payment processor. Many businesses find that the benefits outweigh the risks, especially when mitigating steps are in place (like using same-day ACH for time-sensitive items, maintaining a cash buffer for any payment that might bounce, and implementing strong fraud controls).

ACH Processing Times and Settlement

One of the most common questions about ACH is how long it takes for payments to process. The answer is: it depends on the type of ACH and timing of submission, but generally 1 to 3 business days is the standard. Let’s break down the timing:

- Standard ACH Transfers: Traditionally, a regular ACH payment (credit or debit) submitted today will settle on the next business day or the day after. For example, if you initiate an ACH credit to a vendor on Monday, the debit hits your account Monday and the vendor’s bank will usually post the credit by Tuesday (or Wednesday at the latest). Many ACH payments are next-day by default. Some banks might quote 2-3 days because they account for processing time or risk buffers.

According to Plaid, ACH credits typically reach payees in two business days on average. Square also notes 3-5 days in some cases, which likely includes some cushion for worst-case scenarios or small banks. In practice, for business banking, you’ll often see the money move within one or two days. - Same Day ACH: The ACH network introduced Same Day ACH in recent years for faster settlement. If you submit a payment (credit or debit) within the Same Day ACH cutoff windows, it can settle the same business day, often within hours. Originally, Same Day ACH had lower dollar limits, but now it supports transactions up to $1 million each. There are typically multiple clearing windows: morning, mid-day, and afternoon.

For example, if you originate a Same Day ACH debit at 10 AM, it might settle by 1 PM or 5 PM that day depending on the window. Same Day ACH is great for urgent payments like last-minute payroll or correcting a missed payment. Many banks charge an extra fee for same-day processing, but it’s usually modest. By 2025, Same Day ACH volumes have grown significantly (over a billion payments in 2024) as more businesses take advantage of faster ACH. - Cut-off Times: Every bank has cut-off times each day for ACH files. If you miss the day’s last cut-off, your payment will go out the next business day. Common cut-off times are around 5 PM ET for next-day ACH and maybe noon or 1 PM for same-day ACH (varies by bank). As a business, it’s good to know your bank’s deadlines. If you want an ACH credit to settle the next day, you might need to initiate it by, say, 8 PM ET (if the bank offers late processing). If it’s submitted later, it might add an extra day.

- Weekends and Holidays: The Federal Reserve’s settlement service does not operate on weekends or federal holidays for ACH. That means if you submit an ACH on Friday with next-day timing, the next business day is Monday (assuming no holiday). Payments submitted on Saturday or Sunday are typically processed Monday night and settled Tuesday.

Always account for banking holidays – for instance, ACH transfers around Thanksgiving or Christmas might take longer due to bank closures. Nacha and the Fed are exploring expanded hours in the future (possibly even weekend ACH processing down the line), but as of now, it’s Monday-Friday business days only. - Bank Availability of Funds: After settlement between banks, each receiving bank has its policy on when to make funds available to the recipient. Most banks make ACH credits available immediately on the settlement day (especially for things like payroll). Some might hold atypical large credits for manual review, but that’s rare. For ACH debits (from the payer’s perspective), the bank will show the debit on the day it’s effective and count it in the available balance typically right away.

To illustrate a typical timeline: If you run payroll via ACH credit effective on Friday (payday), you might initiate those payments on Wednesday or Thursday. They get processed and by Friday morning, employees see the deposit. If you’re pulling a customer’s payment via ACH debit due on the 15th of the month, you might submit it on the 15th (or the prior evening’s file) and you’ll know by the 16th or 17th if it settled or bounced. The exact rhythm depends on how your bank batches things.

Frequently Asked Questions (FAQ)

Q: How long does an ACH transfer take to complete?

A: A standard ACH transfer usually takes 1 to 3 business days to fully complete. In many cases, the receiving party will see the funds in their account the next business day or the day after initiation. For example, initiate on Monday, receiver has it by Tuesday or Wednesday. Same Day ACH can speed this up, settling payments the same day (if sent by the cutoff).

Remember that weekends and bank holidays do not count as processing days – ACH transfers initiated on a Friday may not settle until Monday. Always check with your bank’s processing schedule; some banks may hold non-payroll ACH credits an extra day, but this is not common.

Q: What fees do businesses pay for ACH transactions?

A: ACH fees are very low compared to other payment methods. Many business banking accounts offer a certain number of ACH transactions per month for free or a nominal fee. If a fee applies, it’s often in the range of $0.20 to $1.50 per transaction. Some providers charge a flat monthly fee for unlimited ACH. In any case, it’s pennies on the dollar.

For incoming ACH payments, banks typically do not charge a fee to the receiver (so when customers pay you via ACH, you usually aren’t charged by your bank; you’d only pay a fee if you’re using a third-party payment processor that charges one).

Contrast this with credit card processing fees (usually 2-3% of the amount) – ACH is dramatically cheaper. There are also no fees for the payer to send an ACH in most cases (e.g., your vendor likely incurs no charge receiving your ACH, and you might not incur a charge sending it, depending on your bank).

Q: Are ACH payments safe and secure?

A: Yes, ACH payments are considered very secure. They move over the regulated banking network, not the open internet. Financial institutions and processors use encryption and secure systems to protect data. Additionally, the required use of authentication (like verifying micro-deposits or using secure portals to link bank accounts) makes it hard for unauthorized parties to initiate ACH transactions. Fraud rates for ACH are extremely low – only a few cents per $10,000 transacted, per industry studies.

However, no payment method is 100% risk-free: businesses should protect sensitive bank information and use fraud mitigation tools (like ACH debit blocks or alerts). From the customer’s perspective, giving their routing and account number is about as safe as writing a check (since that information is on every check). And consumers are protected by law if an unauthorized ACH withdrawal occurs (they can dispute and recover funds). Overall, when handled properly, ACH is a trusted and safe way to transfer money.

Q: Can an ACH payment be reversed or canceled?

A: Once an ACH transaction is sent for processing, it is generally final, but there are a few exceptions. If you, as the originator, realize a mistake (wrong amount, duplicate transaction, wrong account, or incorrect date), Nacha rules allow you to submit a reversal within 5 business days of the settlement date. This can pull the money back if the funds are still available in the receiver’s account. There’s no guarantee of recovery, but the attempt is allowed in those limited scenarios.

For unauthorized consumer debits, the consumer’s bank can reverse the transaction if the consumer disputes it within 60 days of its posting – this is effectively a forced return for unauthorized debit. Outside these cases, you can’t just “stop” an ACH once initiated (unlike a check you might stop before it’s cashed). If you scheduled an ACH in advance, you often can cancel it before it’s been processed (e.g., cancel a future-dated payment a day prior).

But after it’s processed, the only recourse is a reversal as noted or a new ACH to send the money back. Therefore, always double-check ACH details before sending. And if a customer sent you money by ACH in error, the proper way to return it is to issue a new ACH credit back to them or have them initiate a reversal request through their bank.

Q: Do I need the other party’s permission to pull money from their account (ACH debit)?

A: Absolutely yes. If you are going to initiate an ACH debit from someone else’s bank account, U.S. regulations and Nacha rules require that you have their explicit authorization. This could be a signed form, an electronic consent box they checked, or some similar record. The authorization should outline the amount (or how it’s determined, if variable), the timing/frequency (e.g., monthly on the 1st), and to whom they are giving permission. For recurring debits, one authorization can cover all occurrences, but it must be clear they can revoke it.

For a one-time debit, the authorization can be specific to that transaction. If you don’t have authorization and you attempt a debit, the account holder can dispute it and you’ll likely lose the money and possibly face penalties. In summary, never pull funds via ACH without consent. ACH credits (you sending money out) don’t require permission in the same way – you’re voluntarily sending money to someone. But even then, you typically have an underlying agreement (like you owe a vendor or you’re paying a refund to a customer who expects it).

Q: Can I use ACH for international payments?

A: Not directly in the same way as domestic. The ACH network is primarily for U.S. bank accounts. If you need to pay an overseas vendor or receive payment from a non-U.S. client, typically you cannot just send an ACH. Instead, you might use a wire transfer or an international payment service (like SWIFT transfers). There is something called an International ACH Transaction (IAT), and the Federal Reserve offers FedGlobal ACH for certain countries, but these are handled through partner networks and often the sender or receiver must specifically opt for that service.

It’s not as ubiquitous or straightforward as domestic ACH. For practical purposes, think of ACH as U.S.-only. If you have frequent international transactions, consider using your bank’s wire service or a fintech platform that converts currency and sends local bank transfers in other countries. Those might mimic the effect of ACH in a local context (e.g., SEPA in Europe is analogous to ACH, but you need a foothold in Europe or a service that can access it). For a typical small business, whenever “international” comes up, the answer is usually wire transfer or specialized payment provider, not ACH.

Q: What’s the difference between ACH and Direct Deposit?

A: Direct Deposit is actually a type of ACH payment. The term “Direct Deposit” usually refers to ACH credit transactions that deposit funds into an individual’s account – most commonly payroll, but also things like government benefits or tax refunds. It’s called “Direct Deposit via ACH” because it is an ACH credit push from, say, an employer’s payroll account to the employee’s account. ACH is the broader name of the network and payment system; direct deposit is one popular application of it (focused on pushing payments to consumers).

Another term you might hear is “EFT” (electronic funds transfer) – in the U.S., EFT often is used interchangeably with ACH for bank transfers. So, if someone asks for an EFT payment, they usually mean an ACH transfer. But technically, direct deposits (ACH credits) and direct payments (ACH debits) are all under the ACH umbrella. The main difference is just the context: direct deposit is typically payroll or disbursements to individuals, whereas ACH could be any kind of transfer.

Conclusion

ACH debits and credits are two fundamental tools in modern business banking, each suited to different purposes. To recap, an ACH credit is a push payment – great for sending funds like payroll, vendor pay, or one-off transfers. An ACH debit is a pull payment – ideal for collecting funds such as customer payments or routine bills, once proper authorization is in place. Both leverage the efficient ACH network, offering low fees and reliable processing for domestic transactions.

For business owners, the decision on which to use comes down to who needs to initiate the transaction and for what purpose:

- If your business is disbursing money (paying employees, suppliers, or issuing refunds), you’ll be using ACH credits. This gives you control over timing and ensures recipients get paid seamlessly. It’s a direct deposit into their accounts – convenient and traceable.

- If your business is collecting money (charging customers or receiving regular payments), setting up ACH debits can streamline your receivables. You gain the ability to pull what is owed on the schedule you set (with the client’s agreement), improving your cash flow consistency. It reduces late payments and the manual effort of chasing invoices.

In many cases, a balanced approach is best. A company might pay all its bills and payroll via ACH credits, while also enrolling customers in an ACH direct debit program for recurring charges. By using both, you create an end-to-end electronic cash flow that minimizes paper and maximizes efficiency.

When deciding between ACH and other payment methods (like wires or credit cards), consider cost, speed, and customer preference. ACH saves money and is perfect for predictable transactions. Wires are there for urgent or cross-border needs. Cards can coexist for point-of-sale or consumer choice, but ACH should be leveraged whenever you want to avoid those hefty card fees.

In conclusion, ACH debits vs. credits is not an “either/or” battle – they are complementary tools. The real benefit comes from understanding the difference and deploying each appropriately:

- Use ACH credit when you pay others or move money out.

- Use ACH debit when others pay you and you can initiate the transfer.

By doing so, your business can take full advantage of the ACH network’s convenience, low cost, and reliability. Given how deeply entrenched ACH is in the U.S. (handling payroll for the vast majority of workers and trillions in B2B payments), mastering ACH can significantly improve your financial operations. Embrace ACH for what it’s best at, and you’ll find it’s a powerful ally in managing your business finances – whether you’re pushing out funds, pulling them in, or both.

Leave a Reply