By Rinki Pandey August 4, 2025

When you’re running a small business, every payment counts. Traditional payment methods like paper checks can be slow and credit card payments incur high processing fees that cut into your margins. That’s where ACH payments come in. ACH (Automated Clearing House) is a nationwide electronic network for bank transfers, offering a faster and more cost-effective way to move money between accounts.

In fact, if you’ve ever set up direct deposit for payroll or paid a bill online, you’ve probably used ACH without realizing it. The ACH network moves trillions of dollars each year in the U.S., and 2023 saw a record 31.5 billion ACH payments (about 94 transactions per American) – underscoring how ubiquitous and trusted this system has become.

In this article, we’ll break down the basics of the U.S. ACH payments, how they work, how to set them up for your business, and why they can be a game-changer for your cash flow.

What Is ACH (Automated Clearing House)?

ACH is an electronic funds transfer system that connects all U.S. banks and credit unions into one network. It allows money to be transferred directly between bank accounts through batch processing, without the need for paper checks or card networks. The ACH network is governed by the National Automated Clearing House Association (NACHA), which sets rules to ensure transactions are secure and efficient.

ACH payments are often called direct deposits or electronic fund transfers (EFTs) – for example, payroll direct deposit and many online bill pay transactions use the ACH system. Virtually every bank and credit union in the U.S. is reachable via ACH, making it a ubiquitous backbone for electronic payments.

One key reason ACH is so prevalent is its scale and reliability. The modern ACH Network safely processes tens of billions of payments each year. For instance, in 2022 the network processed about 30 billion payments totaling $76.7 trillion, and volumes have grown every year for over a decade.

This “industrial-strength” payment system reaches nearly all U.S. bank accounts, giving both senders and recipients confidence that funds will be delivered accurately and on time. In short, ACH is the standard way to send money bank-to-bank within the United States, whether it’s a business paying vendors, an employer delivering payroll via direct deposit, or an individual paying a utility bill online.

How Does ACH Work?

ACH payments operate through a batch processing system that runs behind the scenes of the banking industry. Instead of sending funds in real-time like a wire transfer, ACH transactions are grouped together and processed at set times during the business day. Here’s a simplified look at how an ACH transfer flows from one account to another:

In practical terms, if your small business is paying a vendor via ACH, you (the Originator) instruct your bank to send a payment. Your bank (acting as the ODFI) transmits the transaction through the ACH Operator, which then delivers it to the vendor’s bank (the RDFI). The vendor’s bank credits their account with the payment.

This type of transaction is an ACH credit, because you’re “pushing” funds out to the other party. Conversely, if you’re collecting a customer’s payment via ACH (for example, a monthly subscription fee), your customer will authorize you to pull funds from their account.

In that case, your business (via its bank) initiates an ACH debit to “pull” money from the customer’s bank and deposit it into your account. In both scenarios, the ACH network handles the behind-the-scenes routing so that the money moves from the payer’s account to the payee’s account securely.

Batch processing and timing: ACH transactions don’t happen instantly; banks collect ACH requests and process them in batches during the day. The ACH network operates only on business days, with multiple settlement windows each day (currently four times per day on weekdays).

This means if you initiate an ACH transfer in the afternoon, it might be queued and processed in the next batch cycle that day or the following morning. Transactions sent on a Friday or right before a holiday may not settle until the next business day when banks are open. (For example, an ACH payment initiated over a weekend will typically be processed on Monday.)

Despite this batch delay, the majority of ACH payments still clear quite quickly – NACHA estimates that about 80% of all ACH transactions settle within one business day or less. We’ll discuss specific timelines and expedited options (like same-day ACH) in a later section.

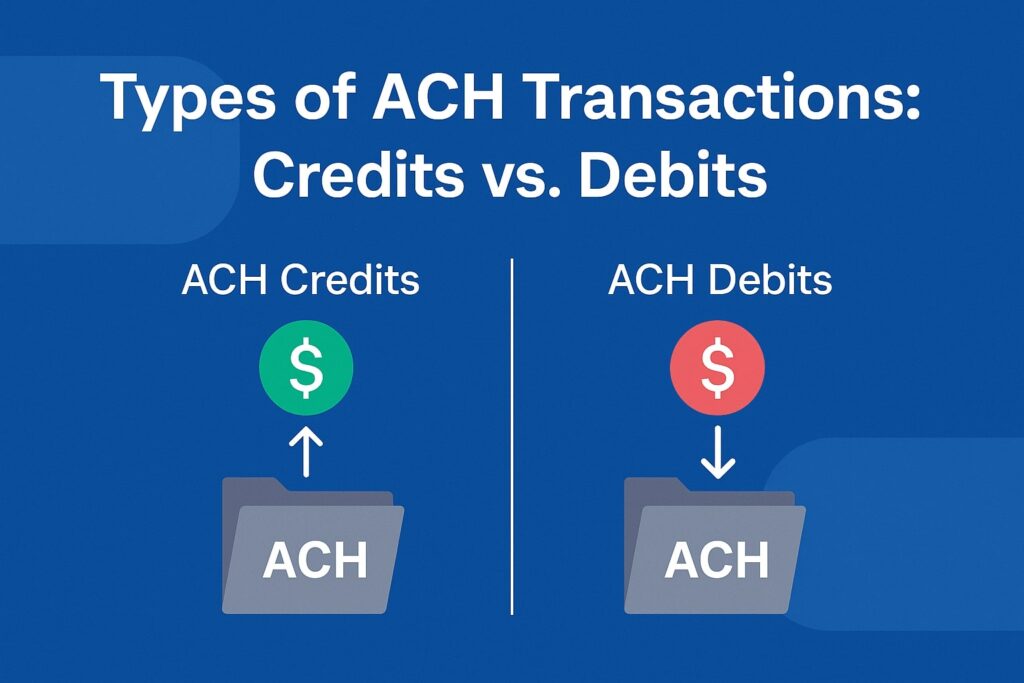

Types of ACH Transactions: Credits vs. Debits

ACH transactions come in two main flavors, which are mirror images of each other:

- ACH Credit (Direct Deposit): An ACH credit is when the sender of funds pushes money into another account. In this case, the payer initiates the transaction. Common examples of ACH credits include payroll direct deposits (an employer pushing wages to employees’ accounts), vendor payments (paying a supplier electronically), government disbursements like tax refunds or Social Security benefits, and person-to-person transfers via banking apps.

For a small business, sending an ACH credit might mean paying your contractors or vendors by transferring funds directly into their bank accounts. The key point is that the money is credited to the recipient’s account. In everyday terms, “direct deposit” is an ACH credit. - ACH Debit (Direct Payment): An ACH debit is when the receiver of funds pulls money from the payer’s account (with authorization). Here, the payee initiates the transaction to withdraw funds from the payer. Typical examples include automatic bill payments – for instance, when your business’s utility company automatically pulls the monthly bill amount from your account, or when you set up recurring customer billing for a subscription service.

Other examples are a gym membership charging members’ bank accounts monthly, or an insurance company pulling a premium payment. In each case, the money is debited from the customer’s account and credited to the business’s account. ACH debits require prior permission; the payer must authorize the payee (often via a signed form or online consent) to initiate the withdrawal.

For small businesses, this distinction is important. ACH credits are commonly used for outgoing payments like payroll, supplier invoices, or reimbursements, where you control the timing and push the funds out.

ACH debits are useful for receiving payments, such as collecting customer invoices or recurring dues automatically – but they do require you to obtain the customer’s explicit authorization (since you’ll be pulling money from their bank). Together, these two types make ACH versatile: it can handle both sides of many transactions that businesses deal with regularly.

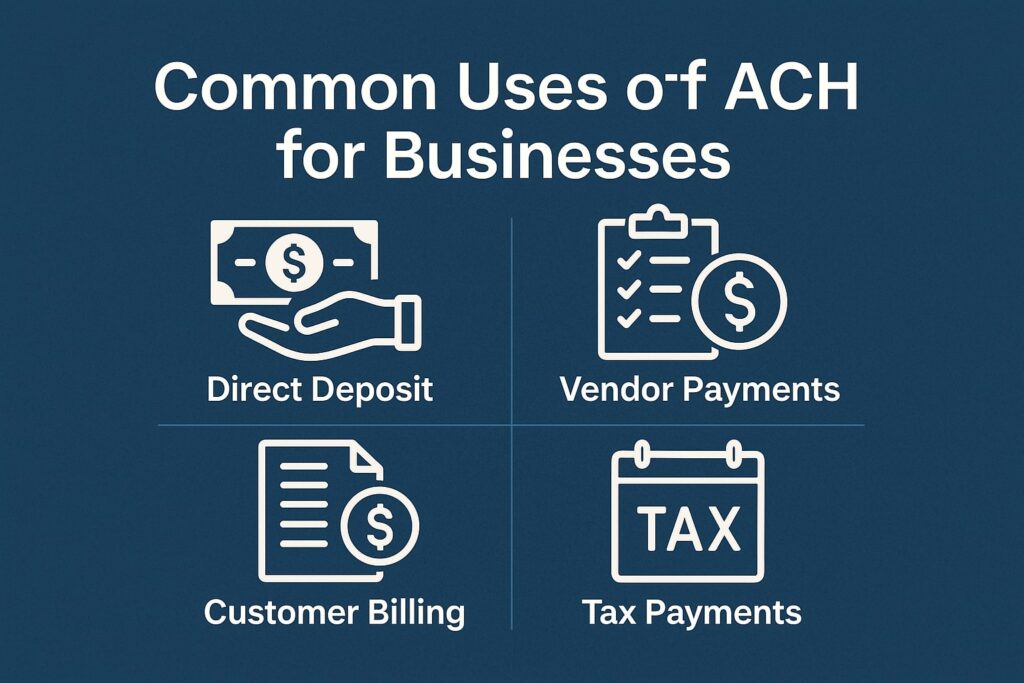

Common Uses of ACH for Businesses

One reason ACH is so valuable to small businesses is the wide range of payment needs it can handle. Some of the most common uses of ACH in a business context include:

- Payroll and Employee Payments: Direct deposit of employee paychecks is one of the best-known uses of ACH. In 2023, over 8.3 billion payroll direct deposits were made via ACH. Beyond salaries, businesses also use ACH to reimburse employee expenses (e.g. travel reimbursements) or to deposit contributions into employee retirement or HSA accounts.

- Vendor and Supplier Payments: Rather than mailing checks, businesses can pay suppliers, landlords (for office rent), or utility bills through ACH transfers. This ensures the vendor receives funds directly in their bank account, typically within 1–2 days, which can improve vendor relationships and simplify accounts payable.

- Customer Invoice Payments: ACH can be a convenient way to let customers pay invoices or bills. For instance, a freelancer or small service provider might let clients pay via ACH (sometimes called e-check) by providing their bank routing and account number, avoiding credit card fees. Similarly, many B2B payments between companies are done via ACH.

- Recurring Billing and Subscriptions: If your business charges customers on a recurring schedule (e.g. monthly memberships, subscriptions, or installment plans), ACH debits allow you to automate those payments. Customers can sign an ACH authorization form to let you pull the agreed amount each cycle, reducing late payments and providing predictable cash flow.

- Government Payments and Taxes: Businesses can pay federal or state taxes through ACH (for example, using the Electronic Federal Tax Payment System), and they can receive government payments (like Small Business Administration loan disbursements or tax refunds) via ACH. The government heavily utilizes ACH – Social Security benefits, for example, are disbursed via ACH direct deposit.

- Personal transfers linked to business: Owners often use ACH to move money between business and personal accounts (when taking draws or making capital contributions) because it’s easy and free at many banks. Additionally, popular services like PayPal, Venmo, and Zelle rely on ACH under the hood to transfer funds to and from bank accounts, so a small business owner withdrawing PayPal funds to their bank is actually using ACH.

In summary, ACH is like the workhorse of non-cash payments: it handles everything from everyday payroll and bill payments to online sales and subscription billing. Understanding these use cases can help you spot opportunities to replace slower or costlier methods (like checks or cards) with ACH transfers in your own operations.

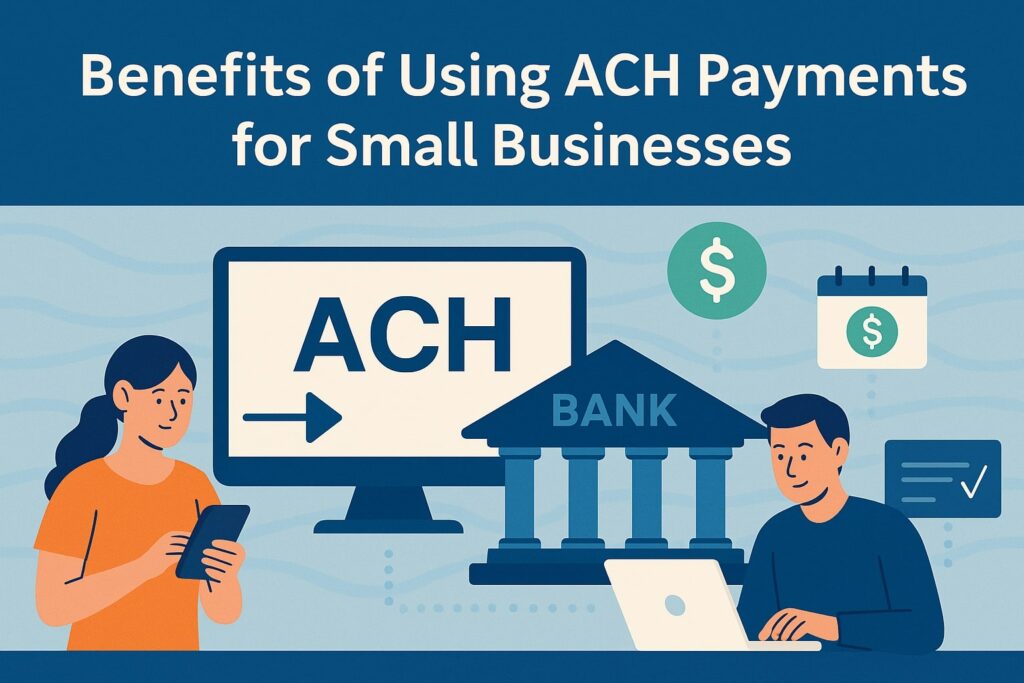

Benefits of Using ACH Payments for Small Businesses

Why should a small business consider using ACH? There are several compelling advantages of ACH payments over traditional methods:

- Lower Cost – ACH payments typically carry minimal fees compared to credit card processing or even the hidden costs of checks (printing, postage, and time). Many banks charge only a small flat fee per ACH transaction (often around $0.20 to $1.50, roughly $0.40 on average) or a low percentage, which is far cheaper than credit card fees that run ~2–4% of the transaction.

ACH is also much cheaper than wire transfers. To put it in perspective, an ACH transfer might cost a few cents to a dollar, whereas mailing a check can cost a few dollars when you factor in supplies and labor. Over time and volume, these savings are significant. - Faster Access to Funds – Unlike mailed checks that can take days to arrive and clear, ACH transactions settle relatively quickly, usually within one or two business days (and sometimes the same day). This faster turnaround means you get your money sooner, improving cash flow.

For example, instead of waiting a week for a check to arrive and clear, an ACH payment might be in your account by the next morning. Faster settlement also lets you know sooner if a payment failed (for instance, due to insufficient funds) so you can address it promptly. Overall, ACH helps speed up the payments process compared to the lag of paper-based payments. - Convenience & Efficiency – ACH payments reduce manual work. There’s no need to print and sign checks, stuff envelopes, pay for postage, or run to the bank to deposit checks. Everything is handled electronically from your computer or phone. You can batch payments and schedule them in advance (say, schedule all your bills or payroll for the month), leveraging the automated nature of ACH.

This automation not only saves time but also means you’re less likely to miss a payment deadline – you can set recurring ACH payments for regular expenses so they happen automatically. Whether you’re in the office or working remotely, you can initiate ACH transfers online, making it a very flexible solution for busy business owners. - Fewer Errors – Because ACH data is handled electronically, there is less room for human error compared to writing checks or manually entering credit card info. You won’t have issues like illegible handwriting or transcription errors that can occur with paper payments. The standardized format of ACH and the fact that account numbers are validated means a lower error rate and fewer payment exceptions to troubleshoot. In short, digital payments streamline record-keeping and reduce mistakes.

- Easy Recurring Billing – If your business bills customers regularly (weekly, monthly, etc.), ACH is ideal for setting up recurring payments. Once customers fill out an ACH authorization form, you can automatically draft their account for the agreed amount each cycle. This greatly reduces late payments or the need to chase down customers, and it helps **stabilize your revenue stream.

For customers, it’s “set it and forget it,” and for you, it’s assured cash flow. Compared to recurring credit card charges, ACH debits avoid problems like expired or canceled card numbers. Customers are far less likely to change their bank accounts frequently, so recurring ACH payments tend to be more reliable over the long term. - Security & Fraud Protection – ACH payments are more secure than paper checks in several ways. With electronic transfers, there’s no physical document that can be lost or stolen from the mail. Each ACH transaction is encrypted and transmitted securely through the banking system.

This limits exposure of sensitive information compared to mailing checks (which contain your account number and routing number in plain sight). Additionally, the ACH network and NACHA rules provide protections: for instance, if an unauthorized ACH withdrawal occurs, consumers have the right to dispute it and banks must investigate, and ACH transactions can be traced and reversed in cases of error or fraud under certain conditions.

From the business side, using ACH means fewer paper checks floating around with your signature – reducing opportunities for check fraud. Overall, the controlled, electronic nature of ACH, combined with regulatory safeguards, makes it a very secure payment method for both parties. - Professionalism and Customer Preference – Offering ACH payment options can enhance your business’s image. It shows that your company keeps up with modern, convenient payment methods. Customers and vendors appreciate when you can pay or be paid electronically without hassle. For example, many clients prefer the convenience of not having to cut a check or provide credit card details for every transaction.

By accepting ACH (sometimes called “eCheck” payments online), you provide a smooth, professional payment experience that can set you apart as easy to do business with. Also, some customers who might hesitate to give a credit card (due to interest or debt) are perfectly happy to pay from their bank account. In short, supporting ACH can expand the payment choices for your customers and partners, potentially making transactions easier and relationships stronger.

Potential Drawbacks and Limitations of ACH

While ACH is extremely useful, it’s important to understand its limitations so you can use it appropriately. Here are a few potential drawbacks or considerations with ACH payments:

- Processing Speed: ACH is faster than mailing a check, but it’s not instantaneous. Standard ACH transfers typically take 1–2 business days to settle (sometimes 3 days depending on the banks and type of transaction). If you need to send money immediately and with certainty (for example, a same-day closing on a real estate deal or an emergency overseas transfer), a wire transfer might be more appropriate.

Same-Day ACH is available for many payments, which significantly speeds up clearing – often to the same business day – but it may come with additional fees and cutoff times (and it’s still limited to banking hours). In short, ACH is fast for routine payments but not real-time like a wire or certain card transactions. - Not 24/7 (Business Days Only): The ACH network currently processes transactions only when Federal Reserve banks are open. This means no ACH settlements on weekends or federal holidays. If you initiate a transfer on Friday night, it won’t move until Monday.

This timing issue can affect cash flow planning – for example, if a customer pays you on a Saturday via ACH, you’ll typically see the funds on Monday or Tuesday. In contrast, newer payment systems (like certain instant payment apps or the emerging FedNow service) can move money outside of banking hours. But with ACH, you need to account for banking calendars in your payment schedule. - Transaction Limits: ACH is designed for a broad range of payments, but it has some limits. NACHA rules currently cap individual Same-Day ACH transactions at $1 million, which is plenty for most small businesses. Regular ACH transfers can exceed that, but your bank or processor might set limits on how much you can send or receive per day, especially when you’re first starting to use ACH.

These risk-based limits (to prevent fraud or big mistakes) can usually be increased over time. It’s a good idea to ask your bank about any ACH dollar limits or volume limits that apply to your account. - Authorization Requirements: When pulling funds from someone else’s account (ACH debit), you must have authorization. This usually means the customer or payer signs an ACH authorization form or provides consent (electronically or on paper) that clearly states the amount and schedule of withdrawals.

Obtaining and storing these authorizations is an extra step for businesses using ACH debits. It’s not a flaw per se – it’s a vital consumer protection – but it does mean you can’t just pull money from clients arbitrarily. The upside is once you have authorization, subsequent debits are easy to manage. - Risk of Returns or Reversals: ACH payments are not guaranteed funds until they clear. If you accept an ACH payment from a customer and their bank account has insufficient funds, the transaction can bounce (be returned), similar to a bounced check. Common ACH return reasons include insufficient funds, closed accounts, or invalid account numbers.

Returns typically happen within 1–2 business days after the payment’s due date. Additionally, in cases of error (like you accidentally debited the wrong amount) or unauthorized transactions, ACH rules allow for reversals under certain conditions. For example, if a wrong amount was sent, the originator can initiate a correcting reversal within five business days.

From a business perspective, this means you should monitor your bank notifications in the days after an ACH payment, to catch any returns. It’s wise to wait for final settlement before treating an ACH payment as cleared funds (especially for large amounts). The return rate in ACH is generally low, but it’s a factor to be aware of – unlike a wire, which once sent is final, an ACH debit from a customer could potentially be pulled back if contested or if funds fail. - Domestic Use Only: ACH is a U.S.-only network. Standard ACH transfers cannot be sent to international banks. If you need to pay overseas vendors or receive payments from foreign clients, you’ll typically use international wire transfers or other payment systems, not ACH.

(There is a concept of International ACH Transactions (IAT), but those are essentially handled by converting to other networks and are more complex.) So, think of ACH as the solution for domestic payments in USD. For cross-border payments, you’ll need to explore other methods or services. - Onboarding and Setup: Using ACH for your business may require a bit of setup. Many banks ask businesses to enroll in their ACH origination service or platform. This could mean filling out forms or agreements, and possibly a short wait for approval. Some banks charge a monthly fee for business ACH services or require maintaining a certain account balance to waive fees.

Additionally, if you use a third-party payment processor to handle ACH (for example, Stripe, PayPal, or QuickBooks Payments), you might pay separate fees or go through their setup process. While these are usually one-time or minimal hurdles, they are considerations. The good news is once you’re set up, using ACH becomes very straightforward for day-to-day operations.

Despite these limitations, ACH remains an extremely efficient system for the vast majority of routine business payments. Understanding the drawbacks simply helps you use it where it makes sense and choose other methods when ACH isn’t the best fit (for instance, very urgent or international payments).

How to Set Up ACH Payments for Your Business (Step-by-Step)

One of the advantages of ACH is that once you’re set up, it’s easy to use. Here’s a step-by-step guide to getting started with ACH payments in your small business, including both sending payments (ACH credits) and collecting payments (ACH debits):

- Open a Business Bank Account: Ensure you have an active U.S. business checking account to use for ACH transactions. Most banks offer ACH capabilities through their business accounts.

If you don’t already have a dedicated business account, open one first, as this will be the account from which funds are sent or received. (Some payment processors can act as an intermediary, but you’ll ultimately need a bank account linked for settlement.) - Enable ACH with Your Bank or Provider: Contact your bank to enroll in their ACH payment services or enable ACH transfers through online banking. Many banks have a specific ACH authorization process – this could involve agreeing to certain terms or limits. Alternatively, you can choose a third-party payment processor or software (such as a payroll service, accounting software, or merchant provider like Stripe/Square) that supports ACH payments.

Enable ACH (sometimes called “electronic bank payments” or “eCheck”) in that platform. Compare options based on fees and features. If you plan to do recurring debits, a provider that automates those might be especially useful. - Gather Necessary Banking Information: Whether you are sending or pulling payments, you’ll need specific details for the other party. For outgoing payments (ACH credits), obtain the payee’s routing number, account number, the name on the account, and the account type (checking or savings).

You might collect this via a vendor form or voided check. For incoming payments (ACH debits), you need your customer’s banking details (routing number, account number, name) just the same. In either case, double-check the numbers for accuracy – one wrong digit will result in a failed transfer. - Obtain Authorization for ACH Debits (if applicable): If you will be initiating an ACH debit from a customer’s account (pulling funds), you must have their permission. Have the customer sign an ACH authorization form or provide consent electronically. The authorization should clearly state the amount (or how amounts are determined), the timing (e.g. a one-time debit on date X, or recurring debits monthly), and their bank details.

Keep this authorization on file (it can be paper or a digital record). For recurring payments, a one-time consent covers the series. If you’re only going to receive ACH credits (the customer pushes money to you), authorization isn’t needed – the act of them sending the payment serves as authorization. But for debits, this step is critical for compliance. - Initiate a Payment or Invoice: Now you’re ready to use ACH. If sending a payment (ACH credit) through your online banking or ACH software, enter the payee’s bank information and payment amount into the system. You may be able to save beneficiaries for future use.

Double-check the scheduled date and amount, then submit the payment. If requesting payment from a client (ACH debit), you will instruct your bank or payment processor to pull the specified amount from the customer’s account – this often involves creating a “debit” entry using the customer’s details you gathered. In some cases, if the customer prefers, they might instead push an ACH credit to you.

In that scenario, you would simply provide the customer with your business’s routing and account number (and perhaps a memo or invoice number), and they initiate the payment on their side. Many businesses include ACH payment instructions on their invoices (e.g. “Pay via ACH to Account XYZ at Bank ABC, routing number 123456789, account number 00012345”). - Set the Payment Details and Schedule: Specify the amount of the transfer and the date it should occur (if not immediate). For one-time payments, you might initiate it to go out today or on a future due date. For recurring payments like payroll or subscriptions, most systems allow you to schedule repeating ACH transactions (e.g. every 1st of the month). Be mindful of weekends/holidays when scheduling – usually you choose the effective business date for the transfer.

If using your bank’s portal, you might see an earliest available date based on cut-off times. Enter any additional info required (such as an addendum or payment description if needed for your records). - Review and Confirm the Transaction: Before finalizing, review all details: the names, amounts, dates, and account numbers. It’s easier to correct an error now than after sending. Once everything looks correct, submit the ACH transaction. Your bank or provider will process it in the next batch cycle. For a credit, your account will be debited on the send date; for a debit, the customer’s account will be debited and your account credited per the schedule.

- Record and Reconcile: After the ACH is initiated, record the payment in your accounting system (if it’s not integrated). When the transaction settles (usually within 1-2 days), verify that the funds have debited/credited the respective accounts. It’s good practice to reconcile your bank statements regularly to ensure all ACH payments were processed correctly.

If any ACH payments are returned or rejected (due to a typo in the account number or insufficient funds, for example), you’ll receive a notice with a return code. Resolve any issues by contacting the payor or updating information, then you can re-initiate if appropriate.

Setting up ACH might sound technical, but in most cases, your bank’s online banking interface or your payment software will guide you through these steps with user-friendly forms. The initial setup (entering payee info or linking accounts) is the most time-consuming part, and even that is not difficult. After that, making an ACH transfer is usually as easy as filling out an online form.

If you’re unsure how to begin, don’t hesitate to talk to your banker – most banks are happy to help business customers enable ACH capabilities. They can provide details on enrollment, any fees or limits, and the specific procedures on their platform. Once enabled, you can start digitizing payments that you might have otherwise done by check, gaining the efficiency and cost benefits we discussed earlier.

Practical tip: It might be wise to do a small test transaction the first time you set up a new ACH payee or debit arrangement. For example, send a $1 payment or have the customer pay $1 via ACH to confirm the details are correct. Some services even do “micro-deposits” – two tiny deposits – to verify account ownership. After that, you can confidently proceed with larger payments.

ACH Processing Times: Standard vs. Same-Day

One of the most common questions about ACH is: How long do transfers take? As mentioned, typical ACH payments clear in 1–2 business days. Here’s a closer look at timing:

- Standard ACH: In the traditional schedule, an ACH transaction initiated on Day 1 will often settle on Day 2 (the next business day) or Day 3 at the latest. For example, if you run payroll on Wednesday, employees usually see the direct deposit in their accounts by Thursday (if submitted early) or Friday. ACH credits (like direct deposits) can be scheduled one or two days in advance; ACH debits (like bill payments) are generally only allowed to post on the next business day by rule.

In practice, many ACH payments (both credits and debits) now settle next-day. In fact, NACHA reported that about 80% of all ACH transactions settle within one business day or less. The remaining might take two days if they missed certain cutoffs or were scheduled intentionally with a delay. Always check with your bank for their specific cut-off times (often late afternoon) – if you initiate after the cutoff, your transaction will go in the next day’s batch, effectively adding an extra day. - Same Day ACH: To accelerate transfers, the ACH network introduced Same Day ACH in recent years. Same Day ACH allows certain payments submitted by specific deadlines to settle the very same business day. Initially launched in 2016 and expanded since, Same Day ACH has grown popular for urgent needs.

There are usually multiple submission windows (morning, mid-day, and early afternoon) for same-day processing; if you submit an ACH entry by, say, 1:00 PM Eastern Time (depending on your bank’s schedule), it could settle by 5:00 PM that day. Both ACH credits and debits are eligible for same-day processing, with the exception of very large transactions (above $1 million) which are excluded.

As of 2022, the per-payment limit for Same Day ACH was raised to $1 million, which covers the vast majority of transactions. Keep in mind banks may charge a slightly higher fee for same-day service, and you must meet the cutoff – otherwise it falls back to next-day. Same Day ACH is extremely useful for last-minute payroll adjustments, emergency vendor payments, or any time you need to get funds moved faster than usual. - Early Funds Availability: An interesting aspect of ACH timing is that receiving banks often make ACH credits (like payroll) available to customers at the start of the due date. For example, many employees find their direct deposit available early in the morning on payday. Banks can even post deposits a bit early (sometimes late the night before) as a customer service gesture, because they know the funds are on the way.

This means from the end-user perspective, ACH can feel very prompt. However, as a business sender, you still need to initiate the payment a day or two prior to ensure it arrives on time. For ACH debits, note that NACHA rules do not allow dating a debit more than one banking day in the future – in other words, you can’t pull funds from a customer’s account say a week later than the initiation; debits are intended to clear quickly or not at all.

Frequently Asked Questions (FAQs)

Q1: How long do ACH transfers take to clear?

Answer: Standard ACH transfers typically clear within one to two business days. In many cases you’ll see the funds the next business day after initiation. The exact timing depends on when the transaction was submitted and the banks’ processing schedules. For example, an ACH payment initiated Monday morning often arrives in the recipient’s account on Tuesday. If it’s initiated later in the day or after the bank’s cutoff, it might settle on Wednesday.

Same Day ACH can clear funds the same business day, provided you meet the cutoff times – this is useful for urgent payments. Keep in mind that weekends and federal holidays do not count as “business days” for ACH, so a transfer sent on Friday might not fully clear until Monday. Overall, ACH is much faster than mailing checks (which can take a week or more to be delivered and processed), but it isn’t instant like some wire transfers or peer-to-peer payment apps.

Q2: What information do I need to send or receive an ACH payment?

Answer: To send an ACH payment (ACH credit) to someone, you will need the recipient’s bank routing number (the 9-digit ABA number for their bank) and their account number, plus the account holder’s name and account type (checking vs savings). These details are typically found at the bottom of a voided check or can be obtained from the payee. Some businesses collect this info using a vendor onboarding form.

To receive an ACH payment (ACH debit or credit), you’ll need to provide your routing and account number to the payer (or have the customer provide theirs if you are pulling the funds). In addition, if you are initiating an ACH debit from a customer’s account, you must have their authorization to do so – usually in writing or electronically. This authorization will include the amount (or method of determining it), timing (one-time or recurring), and the customer’s bank details.

Q3: How is ACH different from a wire transfer?

Answer: Both ACH and wire transfers move money between bank accounts, but they differ in speed, cost, and process. Wire transfers are typically real-time (or same-day) transfers that are processed individually. When you send a wire, it goes directly from your bank to the recipient’s bank with no batching – often within minutes or a few hours – and once sent, the funds are usually available and irreversible.

Wires are great for urgent or high-value transfers, including international payments, but they are expensive (bank fees for a domestic wire often range from $15 to $30 or more). ACH transfers, on the other hand, are batch processed and not instant – they generally take a day or two as discussed. However, ACH is much cheaper (often pennies or a few dollars at most per transaction, and many banks offer free ACH for business accounts).

ACH is best for routine, non-urgent payments like payroll, vendor bills, and subscriptions. One way to think of it: ACH is like sending mail through a bulk mail service – low cost and goes out on the regular schedule – whereas a wire is like sending something overnight express – fast but pricey. Also, international transfers: standard ACH only works within the U.S., while wires can be sent internationally (though at higher fees and with foreign exchange involved).

Security-wise, both methods are secure; in fact, ACH is often considered very safe because of the built-in authorization process and encryption. But from a risk perspective, once a wire is sent it’s gone, whereas ACH transactions can sometimes be returned or reversed if there’s an issue (within a short window). For most small business needs, ACH handles the bulk of payments inexpensively, and you’d reserve wires for situations where speed or international reach is essential.

Q4: Are ACH payments secure?

Answer: Yes – ACH payments are highly secure. The ACH network has multiple layers of security and rules in place to protect users. First, all ACH transactions require known bank account details and, in the case of debits, explicit authorization, which reduces fraudulent or unauthorized transfers. The data transmitted through ACH is encrypted and goes through the Federal Reserve or accredited operators, not open networks.

This means your bank account information is handled in a closed, regulated system. By using ACH, you also avoid the risks of paper checks (which can be stolen, altered, or duplicated). Additionally, NACHA operating rules provide protections: if an unauthorized ACH debit occurs on a consumer account, the account holder generally has 60 days to dispute it and get it reversed, which provides peace of mind (business accounts have shorter dispute windows, so businesses should monitor accounts).

Banks themselves often have monitoring in place for unusual ACH activity, similar to fraud checks on cards. It’s also worth noting that because ACH transfers settle between known bank accounts, the incidence of fraud tends to be lower than credit card fraud. Bottom line: sending or receiving money via ACH is as safe as any electronic banking transaction – and far safer than mailing checks – provided you keep your banking information secure and only transact with trusted parties.

Q5: Can an ACH payment be canceled or reversed if there’s a mistake?

Answer: It depends on the timing and the scenario. If you schedule an ACH payment in advance (say, a bill pay) and realize you need to cancel it, you can usually do so before it’s processed – for example, cancel a day or two ahead through your bank’s online system. But once an ACH is in the clearing process, reversing it is not as simple as flipping a switch, except in certain allowed cases.

NACHA rules allow ACH reversals only for specific reasons: if the payment was a duplicate, if it was processed for the wrong amount, or if it was sent to the wrong account, and in each case, the reversal must be initiated within 5 banking days of the original settlement date. This is typically done by the originator’s bank. So, if your business accidentally paid someone twice or added an extra zero to an ACH payment, you could work with your bank to issue a reversal entry. The receiving party’s bank would then pull the money back out of their account.

For unauthorized transactions (like fraud or an ACH debit a customer didn’t agree to), different rules apply: consumers can dispute an unauthorized ACH debit within 60 days, in which case it becomes a “return” (code R10 or R11) and the funds are returned to the consumer’s account. Businesses have a shorter window (typically 24–48 hours) to contest unauthorized debits on their accounts.

Also, an originator (like your business) can send a stop payment request to your bank for an upcoming ACH debit if you know, for instance, that an invoice you scheduled should no longer be paid – similar to stopping a check. In practice, if an error occurs, act immediately: contact your bank’s ACH department as soon as you notice the issue.

They can advise if a reversal is possible. Outside the formal reversal window, your only option might be to ask the counterparty to send the money back voluntarily. In summary, ACH transactions aren’t easily “canceled” once in motion, but there are procedures to correct mistakes or address unauthorized debits within defined time frames.

Q6: Do ACH payments work on weekends or holidays?

Answer: No, the ACH network does not process payments on weekends or federal holidays. The system operates Monday through Friday during banking hours. If you initiate an ACH transfer on a Saturday or Sunday, it will be queued and begin processing on Monday (or the next business day in case of holidays). The same goes for bank holidays – for example, an ACH submitted on Thanksgiving Day will wait until Friday or the next business day to move.

It’s important to plan around this. For instance, many payroll departments will schedule the payday ACH credit for the Friday before a weekend if payday would normally fall on a Saturday, to ensure employees get paid on time. Similarly, billers will not set ACH due dates on a weekend; they’ll use the following Monday as the effective date in such cases. One additional point: while the interbank processing doesn’t occur on weekends, you might still see pending credits in your account (some banks show an upcoming Monday deposit over the weekend).

But the actual settlement of funds happens on the business day. If you need to send money urgently on a non-business day, ACH won’t be able to do that – you’d need to look at other options (like certain peer-to-peer payment apps or real-time payment networks). However, the constraint of weekends is common to most traditional banking transactions, not just ACH.

Q7: Can I use ACH for international payments?

Answer: Standard ACH is designed for domestic transfers within the United States. If you need to pay someone in another country or in foreign currency, ACH alone won’t suffice. International payments typically go through the wire transfer system or other international networks like SWIFT.

That said, there is something known as an International ACH Transaction (IAT), which is a specific ACH format used when an ACH payment involves a foreign bank (for example, a U.S. bank might send an IAT that converts to a foreign clearing system). But as a small business owner, you won’t commonly originate IATs unless your bank specifically offers that service – and even then, it might be easier to just send a wire for an international payment.

Also, services like Wise or PayPal can facilitate cross-border payments by leveraging various networks, but those are outside the traditional ACH channel. So, the simple answer is: No, ACH is generally domestic-only. If you send an ACH to a bank routing number, it must be a U.S. bank. For international vendors or clients, discuss wire transfers or other payment platforms as the solution.

Q8: What are the fees for ACH payments?

Answer: One of the attractive features of ACH is the low cost. Many small business owners find that ACH fees are negligible compared to credit card fees. Banks often charge a flat fee per transaction (commonly in the range of $0.20 to $1.00 per ACH payment. Some banks bundle a number of ACH transactions for free with certain accounts, or charge a monthly fee for unlimited ACH.

Third-party payment processors might charge a percentage (often around 0.5% to 1% of the transaction) capped at a few dollars. For example, a processor might charge 1% up to a maximum of $5 per ACH payment – which is much cheaper than 3% on a $1000 credit card charge (which would be $30). There can also be fees for returns (e.g. if an ACH bounces, a bank might charge ~$5-10 NSF fee, similar to a bounced check fee).

If you opt for Same Day ACH, some banks charge an extra fee (maybe a dollar or two more) for the expedited service. It’s good to check your bank’s fee schedule or the processor’s pricing. As a ballpark, the typical ACH cost is around $0.40 per transaction according to industry averages.

In contrast, the average paper check is estimated to cost a couple of dollars in materials and labor, and credit card processing is 2-3% of the amount. This stark difference is why ACH can save you a lot in payment processing costs over time. So while there may be some small fees associated with ACH, they are among the most affordable payment methods for businesses.

Conclusion

ACH payments are the unsung hero of the American payments landscape – they quietly power direct deposits, bill payments, and countless business transactions every day. For small business owners, understanding and leveraging ACH can lead to faster payments, lower fees, and less administrative hassle in managing money.

In this guide, we covered how ACH works (through the banking network under NACHA’s rules), the types of ACH transfers (credits vs. debits) and their use cases, the benefits (from cost savings to convenience and security), as well as practical steps to set up ACH payments for your business. The key takeaways are that ACH is fast (though not instant), inexpensive, and reliable for domestic transfers. By moving away from paper checks and embracing electronic transfers, you can streamline your cash flow – getting funds where they need to be with minimal delay and effort.

Remember that while ACH has a slight learning curve (mostly in the initial setup and understanding timing), most banks and financial software make it straightforward. Don’t hesitate to reach out to your bank for help enabling ACH capabilities. With a one-time setup, you’ll open the door to easier payroll runs, quicker bill payments, and happier vendors and customers who appreciate the ease of electronic payments.

In a business where every dollar and every day counts, ACH provides a fundamental tool to manage your finances efficiently. Embracing ACH payments can ultimately save you money, reduce errors, and give you greater control over your company’s financial transactions – a smart move for any modern small business owner.

Leave a Reply