The ACH network is a silent partner in the majority of the day-to-day payments that people and businesses depend on. Nevertheless, really only a few know how it works behind the scenes. ACH transactions have a huge volume of trillions of dollars getting transferred yearly between U.S. financial institutions, with deposits of payroll, refunds of taxes, payments of utilities, and subscriptions among the main ways of transferring money. Although ACH’s magnitude is enormous, the process remains relatively invisible to consumers.

Basically, the ACH system sees it through financial institutions can make electronic transfers among themselves via the nationwide Automated Clearing House network. Whereas card payments and wire transfers are instant, ACH transactions are cleared and settled in batches, which is why they are cheap, very safe, reliable, and the best option for recurring payments. This very reason for efficiency also means that ACH payments, instead of being instant, follow a structured, multi-step workflow.

One of the most important things to know about the processing of ACH payments is that it can be advantageous to businesses depending on how they manage their cash flow, payroll timing, or customer billing. If one is aware of the network’s functioning in terms of delays, returns, and settlement timelines at each stage, then he/she will not be caught unawares. This blog will guide you through the step-by-step process of how the money actually moves through the ACH network so that you will literally be able to follow the payment journey from the time it was first initiated until the bank account gets credited.

ACH Network Overview and Why It Exists

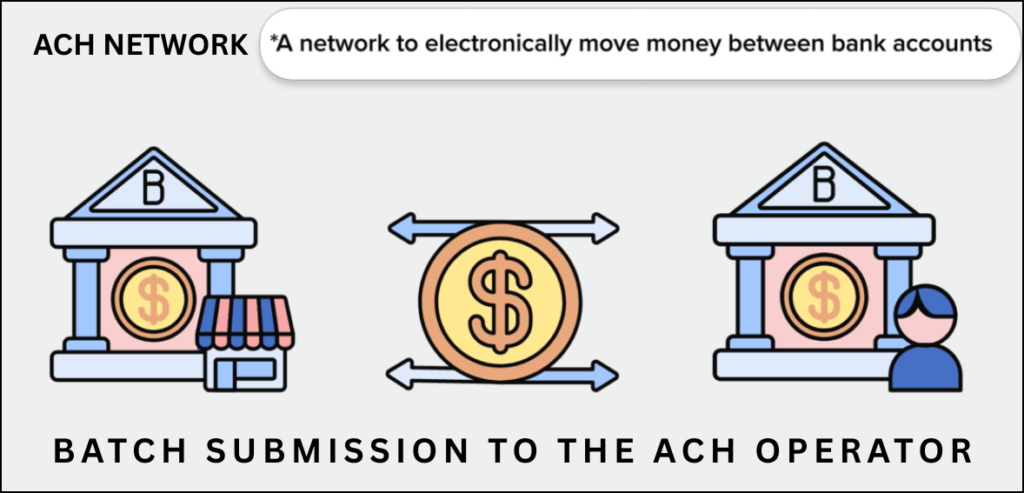

This network can be characterized as a safe and uniform means for the electronic transfer of money between banks across the United States. Before its implementation, a good number of payments were made through paper checks, which, besides being slow and costly, were also subject to errors.

As an Automated Clearing House feature, ACH interlinks numerous financial institutions through a unified clearing process. Rather than transferring money instantly between banks, ACH combines transactions and clears them at regular intervals. This method is responsible for low costs as well as the minimization of operational risk.

The network is utilized for various types of electronic bank transfers, such as salary payments, government assistance, consumer bills, and corporate transactions. Even though it is not instantaneous, the ACH network gives its preference to precision, extensive use, and uniformity— features that render it indispensable to today’s financial infrastructure.

ACH Network Participants and Their Roles

In order to get a full picture of the money transfer using the ACH network, it is necessary to identify the main participants in the process. Each ACH transaction brings in some entities that, together, function like one big Automated Clearing House. The primary participants include:

- Originator: The company or person that starts the payment.

- Originating Depository Financial Institution (ODFI): The bank of the initiator.

- ACH Operator: The main processor that classifies and directs the transactions.

- Receiving Depository Financial Institution (RDFI): The bank of the recipient.

- Receiver: The person or business that gets the money.

Every party involved has clearly defined functions in the processing of ACH payment, which assures that the transactions are subject to uniform regulations. The entire ecosystem is, therefore, very well organized, and this is what enables the network to process huge numbers of transactions in the same way and at the same time build trust.

ACH Network Step One: Payment Authorization

Authorization is the first step in every ACH network transaction. A sender should always get the express consent of the receiver before starting any electronic bank transfers. Depending on how the payment is made, the authorization can be written, electronic, or oral.

This is a necessary step as the whole Automated Clearing House system is based on trust and reversibility. Transactions might be returned or contested if there is no authorization. In the case of continuous payments like subscriptions or wages, the authorization is often considered active until the sender takes the step to cancel it.

Therefore, clear authorization not only protects the parties involved but also ensures the integrity of the ACH payment processing. It, moreover, brings the institution into compliance with the network rules and, thus, may eliminate the risk of returns and penalties later in the process.

ACH Network Step Two: Payment Initiation

Authorized previously by the receiver, the originator then proceeds to the bank or payment processor for the transaction to be executed. The stage of the ACH network still has no money moving; it only takes the payment instructions. The originator gives the following information:

- Bank routing number of the receiver

- Account number

- Transaction amount

- Type of payment and date of effect

These directions comply with Automated Clearing House standards. This action converts a payment request into a properly organized ACH entry, which is subsequently processed. Here, precision is of utmost importance because even small errors can lead to either the delay of the electronic bank transfer or the return of the money.

ACH Network Step Three: ODFI Processing

The transaction is sent to the Originating Depository Financial Institution (ODFI) right after the initiation. The ODFI is a controlling entity within the ACH network. The bank ensures that:

- The originator has permission

- There are enough funds or credit limits available

- Transaction data conforms to ACH formatting rules

DOFI, after validating, sorts the transaction with others that are due for processing. This sorting method is a characteristic aspect of ACH payment processing, which assists the Automated Clearing House in handling a large number of transactions in an efficient manner.

ACH Network Step Four: Batch Submission to the ACH Operator

An ODFI sends the transaction batches to an ACH Operator, which can be either the Federal Reserve or a private clearing operator. Thus, the ACH network initiates its centralized processing.

The operator categorizes the transactions according to the banks they are to be sent to and gets them ready for dispatch. The ACH does not process each transaction one at a time; rather, it operates with large amounts of transaction data that may include several thousand payments.

This method regarding batches allows for electronic interbank transactions at a low cost, yet it also brings into play the question of timing. The processing intervals and cut-off times dictate when a transaction is to go to the next phase.

ACH Network Step Five: Clearing and Sorting

Clearing is considered one of the main operations of the ACH network. At this stage, the ACH Operator sorts out transactions and determines the amounts that are owed between banks and other financial institutions.

The netting takes place among the Automated Clearing House as it nets debit and credit for each participating bank instead of moving money for each transaction separately. This not only minimizes the money that has to be transferred but also saves time. Hence, increasing efficiency and lowering settlement risk.

Clearing gives assurance that the system of ACH payment processing would not be affected by high volumes of transactions, as is the case with other payment systems. Additionally, it takes the responsibility of presenting the transactions to the receiving banks in a manner that is uniform and predictable.

ACH Network Step Six: Delivery to the Receiving Bank

Once the clearing process is done, the transactions are sent to the Receiving Depository Financial Institution (RDFI). Now this network has an obligation towards the bank of the receiver. The RDFI:

- A credit or debit is now a part of the receiver’s account.

- Looks into the transactions to find out if any need to be returned.

- Funds are accessible to the receivers based on policy.

The time for this varies according to the bank and the type of transaction. Some electronic bank transfers are posted immediately, whereas others might take one or two business days. This step is critical for customer experience in ACH payment processing.

ACH Network Step Seven: Settlement Between Banks

Settlement refers to the actual movement of funds between different banks. The Federal Reserve accounts are used for settlement purposes, where net positions calculated earlier are used by the ACH network for the settlement process.

The Automated Clearing House system guarantees that each bank either pays or gets the right net amount. The process of centralized settlement reduces risk and keeps liquidity requirements at a manageable level.

Settlement, though hidden, is nonetheless the moment when ACH transactions between banks become final.

ACH Network Step Eight: Funds Availability to the Receiver

When the settlement comes to an end, the funds are totally accessible to the receiver, and it all depends on the bank’s policies. For the user, this is the time when the electronic bank transfer is considered completed. Availability relies on:

- Type of transaction (credit or debit)

- Bank processing calendars

- Risk and fraud prevention measures

The ACH network values reliability more than instant speed, and that is the reason why the processing of ACH payments usually takes one to three business days.

ACH Network Returns and Exceptions

Not every ACH transaction goes through without a hitch. This has a well-organized return process that is used to deal with mistakes or controversies. The most frequent causes of returns are:

- Not enough money in the account

- Wrong account number

- Transaction not authorized

Returns are guided by rigid schedules that are set by the Automated Clearing House regulations. This very flexibility, which is inherent to the ACH payment processing, ensures it is safer for both consumers and businesses, although the process becomes more complex.

ACH Network vs Real-Time Payments

Analyzing the differences between the ACH network and real-time payment systems demonstrates the distinct function of ACH. The first one is mainly concerned with batch efficiency and cost control, while the latter one is with the immediacy of payment. The ACH system still keeps its place at the top despite faster options because of:

- Lower costs to a great extent

- Infrastructure that is generally accepted

- Clear rules

Predictability and reliability are a priority over speed for many recurring electronic bank transfers that are recurring.

ACH Network Security and Compliance

The ACH network’s core is built on security. The transactions in the Automated Clearing House network are protected by encryption, access controls, and compliance monitoring.

NACHA rules on authorization, data security, and risk management must be adhered to by participants. These protocols solidify the trustworthiness of ACH payment handling even at large volumes.

Robust compliance systems are those that not only block fraud but also allow smooth movement of money through electronic banking.

ACH Network Use Cases for Businesses

Businesses look upon the ACH network as a reliable, low-cost payment method that supports daily operations and long-term planning. The main applications include payroll, vendor payments, subscription billing, and tax payments, which all benefit from the convenience of automated scheduling and the advantage of lower-fee transactions.

For companies working with tight cash flow, ACH payment processing offers reliability and clarity, hence it becomes less difficult to predict the cash flow of outgoing and incoming funds. The Automated Clearing House, with its high transaction volume capacity, provides reliability for businesses to grow their payments without incurring high processing costs like those associated with card networks or wire transfers.

ACH Network Use Cases for Consumers

The ACH network is an integral and daily interaction for most, if not all, consumers, though often the consumers are not aware of this power used in the background for major financial transactions. The network is behind the movement of money between banks for all direct deposits for wages and pensions, bill payments, and even some peer-to-peer transfers that happen regularly.

The electronic bank transfers are all about convenience, lower prices, and being sure they work as promised. Equally, strong consumer protections are inherent in ACH technology news – among them are the requirements for prior approval and the consumers’ rights to get refunds. They all serve to protect consumers from erroneous charges, unauthorized deductions, and some kinds of payment disputes.

ACH Network Processing Timelines Explained

Mastering the timeline of ACH network use is an essential part of the game for businesses whose operations depend on exact cash flow management. Transactions are processed not by instant settlement, but by the submission deadlines, the batch processing schedules, and the posting policies of individual banks.

Eligible payments can receive same-day ACH alternatives with quicker delivery for transactions of a time-sensitive nature. However, standard ACH payment processing continues to operate on multi-day cycles. Awareness of these timelines aids both the business and the consumer in making timely payments correctly, avoiding delays. Hence, minimize the risk of returns or overdrafts.

Conclusion

The ACH network has not evolved in such a way as to be capable of instant payments, but it is still one of the most dependable and effective methods for transferring money within the United States. An Automated Clearing House (ACH) moves the payment through a series of carefully designed steps where precision, volume, and low cost are the main focuses. Each of the phases, viz. authorization, batching, clearing, settlement, and returns, has its own importance in guaranteeing safe electronic bank transfers.

In the case of both companies and customers, knowing the network functioning gives them power over timing, cash flow, and risk control. With the advancement of payment technology, ACH can still be considered as the backbone of daily financial transactions—silently, reliably, and at a huge scale.

FAQs

What is the ACH Network?

This network comprises an electronic infrastructure that permits the transfer of funds from one U.S. bank to another through the process of batch processing.

What is the payment processing period of ACH?

Usually, the regular ACH payments are settled in a timeframe of one to three business days only if the concerned banks follow their planned processing.

What kind of payments go through the ACH network?

ACH network is predominantly utilized for payroll, payments of bills, refunds of taxes, and depositing money directly into the bank account.

Would you say the ACH network is secure?

Yes, the system does use encryption, authorization protocols, and compliance measures to ensure the safety of the transactions.

Are ACH payments reversible?

Certain ACH transactions are allowed to be reversed or returned within a specified period for reasons of mistakes or unauthorized activities.

Leave a Reply