Recurring ACH payments are automated electronic bank transfers that repeat on a set schedule (such as weekly or monthly). “ACH” stands for Automated Clearing House, which is the U.S. network that processes these bank-to-bank transactions.

This system allows businesses and individuals to move money between accounts without having to manually initiate each payment.

In fact, a majority of U.S. businesses use ACH transfers for routine transactions – in the third quarter of 2023 alone, the ACH network processed 7.8 billion payments (a 3% increase from the same period in the previous year).

From paying employees via direct deposit to collecting monthly customer payments, ACH is a backbone of everyday finance in the United States.

Recurring ACH payments are simply ACH transfers that occur on a recurring basis. Once set up, these payments happen automatically on their schedule. This means you don’t have to remember to mail a check or initiate an online payment each time – the funds move electronically based on the agreed timing.

Common examples include monthly bill payments (utilities, mortgages, gym memberships), subscription fees (streaming services, insurance premiums), retainer payments for freelancers, and even installment plans for large purchases.

Both businesses and consumers benefit from this automation: businesses enjoy predictable cash flow, and consumers avoid late fees by paying on time without extra effort.

In this comprehensive guide, we’ll explain what recurring ACH payments are, how they work, how to set them up, and the pros and cons compared to other payment methods like credit cards and wire transfers.

We’ll also cover important legal and compliance considerations in the U.S. so you can use recurring ACH payments confidently and in accordance with the latest rules.

What Are Recurring ACH Payments?

A recurring ACH payment is an electronic funds transfer that automatically repeats on a set schedule through the Automated Clearing House (ACH) network. The ACH network is the U.S. system that enables direct bank-to-bank transfers, functioning as a modern digital alternative to writing paper checks.

When you set up a recurring ACH payment, you’re authorizing a series of transfers from one bank account to another (for example, from a customer’s checking account to a business’s account) on a regular interval – such as weekly, monthly, or quarterly – without needing further manual input each time.

How it differs from one-time payments

All ACH payments (one-time or recurring) are processed through the same network, but a recurring ACH payment implies an ongoing payment plan or subscription.

For instance, a one-time ACH transfer might be used to pay a single invoice or move money once between accounts. In contrast, recurring ACH is used for ongoing obligations – think of monthly subscriptions or installment payments where the same payor will be debited on a schedule.

After the initial setup, each recurring payment is pulled or pushed automatically per the schedule and amount agreed upon.

Everyday examples: Recurring ACH payments are extremely common in the United States for both personal and business finances. A few typical examples include:

- Direct Deposit of Salaries: Employers use ACH to push payroll deposits into employees’ bank accounts on a repeating cycle (e.g. biweekly). In fact, about 93% of American workers receive pay via ACH direct deposit, showing how ubiquitous this method is.

- Bill and Subscription Payments: Consumers often authorize recurring ACH debits to pay ongoing bills – such as utility bills, rent or mortgage payments, insurance premiums, streaming service subscriptions, or gym memberships.

On each due date, funds are automatically withdrawn from the customer’s account and sent to the biller, ensuring on-time payment. - Retainers and Installment Plans: Freelancers or service providers might bill clients a fixed retainer fee every month via ACH.

Similarly, large purchases (like medical bills or expensive items) are sometimes paid in installments using recurring ACH transfers, spreading the cost over time without the high fees of credit cards. - Memberships and Donations: Organizations like clubs, nonprofits, or subscription services use recurring ACH to collect membership dues or recurring donations. Donors can “set and forget” a monthly contribution that automatically transfers from their bank account.

Geographic scope: It’s important to note that ACH is a U.S.-based payments network managed by the National Automated Clearing House Association (Nacha). Recurring ACH payments are primarily available within the United States.

Other countries have their own similar automated bank transfer systems (for example, the UK’s Direct Debit via BACS, or Europe’s SEPA direct debits), but those are separate from the U.S. ACH.

The U.S. ACH system does not directly support international bank transfers. So, if you need to set up recurring payments overseas, you would typically use different methods (international wires, global payment services, or local country equivalents of ACH).

For U.S.-based businesses and individuals, however, ACH is widely accessible through virtually all banks and credit unions.

How Do Recurring ACH Payments Work?

Recurring ACH payments follow a standardized process every cycle to move money from the payer’s bank account to the payee’s account. Here is a step-by-step look at how recurring ACH payments work:

- Authorization Setup: Everything begins with the payer’s consent. The account holder (payer) must authorize the company or individual (payee) to pull funds from their bank account on a recurring basis.

This usually involves filling out a form or online agreement that grants permission for the automated withdrawals. The authorization form will include details like the payer’s bank routing number and account number, the amount or formula for each payment, and the payment frequency/schedule.

For example, a customer might sign an electronic form allowing “Company X” to deduct $100 on the 5th of each month for a subscription service. Authorization is a critical first step – without it, a business cannot initiate recurring ACH debits from a customer’s account (more on legal requirements for authorization later). - Scheduling the Payments: Once authorization is in place, the payee (the party receiving the money) sets up the recurring payment schedule in their system or through their bank.

They will use the agreed-upon terms from the authorization (such as amount and dates) to program the payments. Businesses often use either their bank’s ACH origination service or a payment processor platform to schedule recurring ACH debits.

For example, a small business owner might log into their payment software and input that $100 should be pulled from the customer’s account on the 5th of every month until further notice. This scheduling can usually be adjusted if needed (e.g., to skip or change a date, or end the schedule) by the payee’s system. - Transaction Initiation: On each scheduled payment date, the payee’s bank (known as the Originating Depository Financial Institution, or ODFI) generates an ACH entry to start the transfer.

In simple terms, the payee’s bank sends an electronic request through the ACH network to debit the payer’s bank account for the specified amount.

This typically happens in batches – the payee’s bank might combine many ACH requests together if multiple payments are scheduled that day, then send them in one batch to the network. - Clearing and Funds Transfer: The ACH network acts as the intermediary that clears and settles the payment. The network will route the transaction to the payer’s bank (the Receiving Depository Financial Institution, or RDFI).

The payer’s bank receives the debit request and automatically checks the account. If the account has sufficient funds, the bank debits (withdraws) the payment amount from the payer’s account.

Those funds are then in transit through the ACH system. The clearinghouse (ACH operator) ensures the transaction details are processed and then credits the payee’s bank in the next scheduled settlement window. - Settlement and Confirmation: The payee’s bank account receives the funds and the payment is settled. The payee’s bank will credit the payee’s account with the amount collected.

Typically, the payee gets a confirmation from their bank or payment processor that the payment was successful and the money is deposited.

On the payer’s side, the transaction will appear on their bank statement (often labeled with the company name and ACH, indicating an electronic payment).

Both parties now have a record of the transfer. If you’re the business receiving funds, it’s good practice to send a receipt or confirmation to your customer as well, noting that their payment for that period was received. - Ongoing Cycle and Monitoring: The above process repeats for each interval (the next week, month, etc.) as long as the authorization remains in effect. Businesses should monitor their recurring ACH transactions regularly.

This means checking that each expected payment comes in, and following up on any that fail (for instance, due to insufficient funds or a closed account).

If a scheduled payment is missed or returned, the payee may contact the payer to resolve the issue or arrange a different payment method for that instance. We’ll discuss in a later section how to handle such exceptions and what can cause an ACH payment to fail.

Summary of the process: The recurring ACH flow can be summarized as Authorize → Schedule → Initiate → Debit/Credit (Clearing) → Settle/Confirm, and then repeat. All of this happens electronically through banking systems.

From the payer’s perspective, after the initial setup, their involvement is minimal – they just need to ensure the account has funds and review their statements.

From the payee’s perspective (e.g., a business), recurring ACH provides a hands-off way to collect payments, though it does require setting up the infrastructure with a bank or payment service.

How Long Do ACH Payments Take to Clear?

One common question is how quickly the money moves in a recurring ACH payment. ACH payments are not instant – they typically take a few days to fully clear and settle.

In general, a recurring ACH transaction will move from the payer’s account to the payee’s account in about 3 to 5 business days. Here’s the typical timeline:

- Day 0 (Initiation): The payment is initiated on the scheduled date. Often, businesses initiate the ACH debit one business day before the due date as a lead time.

For example, if a payment is due on the 1st of the month, the debit might be sent on the 31st (or earlier if the 1st falls on a weekend) to ensure it processes in time. - Day 1 (Processing/Batching): The ACH network aggregates the request with other transactions and processes them, usually overnight or in the next available batch window.

By the next business day morning, the payer’s bank will have debited the account (reducing the payer’s balance) and the funds are en route to the payee’s bank. - Day 2 (Settlement): Typically by the second business day, the payee’s bank receives the transaction and the ACH system settles the payment between the banks.

At this point, the payee’s bank has the money, but some banks may hold the funds briefly until fully cleared. - Day 3 (Funds Available): In many cases, by the third business day, the funds are available in the payee’s account.

Some banks might make the money available sooner (especially for established, low-risk transactions), while others wait until they are confident there are no issues. - Possible Day 4-5: In some cases, if there are any processing delays or if the transaction missed a cutoff time, it might add another day.

Also, if a weekend or bank holiday occurs during this timeline, the process pauses until the next business day (ACH does not operate on weekends/holidays).

Overall, you can expect an ACH payment to complete within 3 business days on average, though it could be as quick as the next day or as slow as five days in certain cases.

It’s wise for businesses to plan cash flow around this timing – for instance, don’t schedule a supplier payment via ACH on the due date itself, as it will arrive a couple of days late. Instead, initiate recurring ACH debits a few days before bills are due.

Same-day ACH

There are options to speed up ACH transfers via Same Day ACH processing windows, which NACHA introduced to accelerate some payments. If an originator (the sender) opts for same-day service (and pays any applicable fees), an ACH transfer can settle within the same business day.

However, in practice, many recurring payments use the standard ACH processing since they are predictable and not urgent. Same-day ACH might be used for one-off urgent payments or payroll adjustments, but for routine recurring billing, businesses often schedule with normal ACH timelines in mind.

Not all banks or processors automatically use same-day processing, and there are cutoff times and dollar limits (currently, around $1 million per payment) for same-day ACH. If faster settlement is critical for a recurring payment, talk to your bank or payment provider about enabling same-day ACH on those transactions.

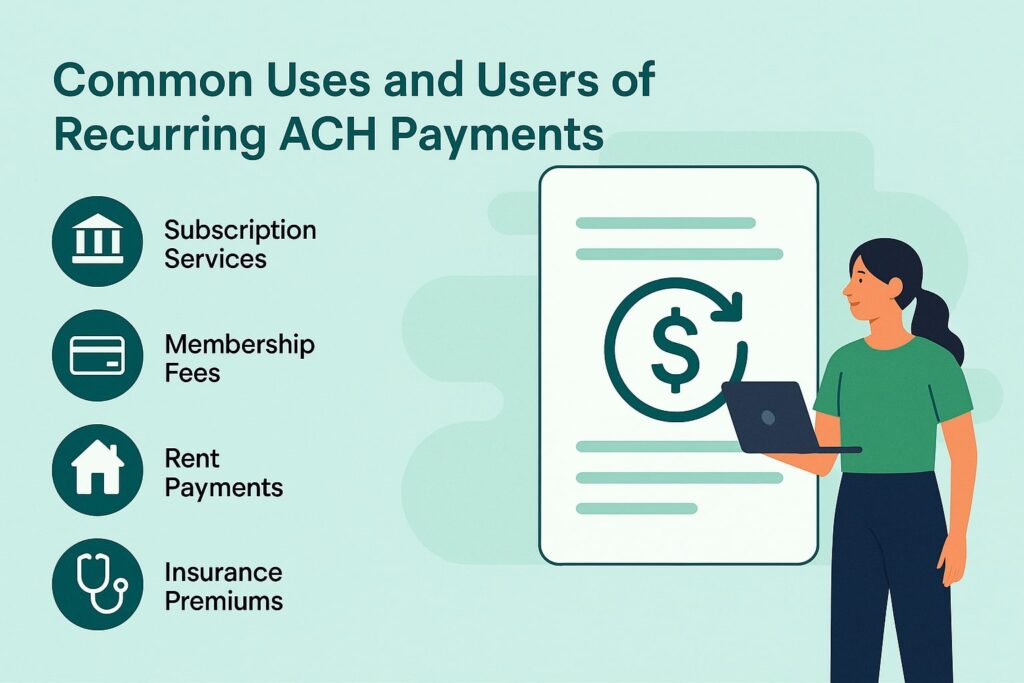

Common Uses and Users of Recurring ACH Payments

Recurring ACH payments are versatile and used by various types of people and organizations. Here we highlight how different users can leverage recurring ACH transfers:

- Small Business Owners: For small businesses, recurring ACH is a reliable way to collect payments from customers or pay regular expenses. Businesses can set up recurring ACH billing for services like monthly maintenance contracts, subscription boxes, daycare tuition, or membership fees.

This means not having to chase customers for checks or worry about expired credit cards. The business knows revenue will come in on schedule, improving cash flow stability.

Small businesses also use recurring ACH on the payables side – for example, scheduling monthly rent to their landlord or making lease payments via ACH, so they never miss a due date. Compared to card payments, ACH fees are much lower, which helps maintain profit margins on recurring revenue. - Freelancers and Consultants: Independent workers often have ongoing agreements with clients (for instance, a consultant on retainer or a freelancer who bills the same amount each month).

Recurring ACH payments allow freelancers to automate their invoicing. Instead of sending an invoice and waiting for a check or manual online payment, the freelancer can arrange (with the client’s permission) to auto-debit the client’s account on a set day.

This ensures they get paid promptly for recurring work, without awkward reminders. It’s a win-win since the client doesn’t have to remember to pay each invoice – the process is hands-off.

Many online invoicing and accounting platforms (like QuickBooks, FreshBooks, etc.) now support ACH payment collection for invoices, often with an option to “save this account for automatic future payments.” - Consumers: Everyday people benefit from recurring ACH mainly through automatic bill payments and deposits. A common scenario is signing up for AutoPay for bills – for example, a utility company or insurance provider might offer a discount or simply the convenience if you allow them to auto-draft your bank account each month.

This spares you the hassle of writing checks or logging in to pay, and it guarantees you won’t incur late fees as long as your account has funds.

Consumers also receive recurring ACH credits such as government benefits (Social Security is paid via ACH direct deposit) and investment account transfers (e.g., automatically moving money from checking to a savings or brokerage account each month as part of a budget plan).

Recurring ACH can thus help with personal budgeting – automating your savings or ensuring your bills are covered without manual effort. - Accountants and Finance Teams: For finance professionals, recurring ACH payments simplify accounts receivable and accounts payable processes. An accountant for a business might set up customers on recurring ACH billing to reduce the time spent on collections.

They can also schedule the company’s routine payouts (like vendor payments, loan payments, or subscription software fees) via ACH. This reduces paperwork (fewer checks to cut) and creates a clear digital paper trail that can be easily reconciled in accounting systems.

Accountants appreciate that recurring ACH payments provide predictable timing – they know exactly when cash will be debited or credited, which aids in cash flow forecasting and management.

Additionally, using ACH for regular payments can reduce transaction costs significantly compared to wire transfers or credit card fees, which is a direct savings to the company. - Large Organizations and Payroll: Bigger companies and government agencies rely on recurring ACH for payroll (direct deposit) and other large-scale repetitive payments.

Payroll is a classic example of recurring ACH credit transactions: an organization might have a cycle where every other Friday, a batch of ACH credits goes out to all employees. This is far more efficient and secure than distributing paper paychecks.

Similarly, recurring ACH debits are used by lenders to collect monthly loan payments from thousands of borrowers automatically – a process vital to banks and loan servicers to ensure on-time collection.

Use case spotlight

One area where recurring ACH has grown is in subscription-based businesses – everything from streaming services to monthly subscription boxes and SaaS software providers.

While many subscriptions bill customers’ credit cards, an increasing number of businesses give the option to pay by ACH (direct debit from a bank). Customers who choose ACH often do so to avoid maxing out credit cards or because they prefer not to incur credit card debt for a subscription.

For businesses, an advantage of ACH here is that bank accounts rarely “expire” – unlike credit cards, which might expire or get replaced every few years, bank account numbers tend to remain the same for a long time (the average U.S. checking account is kept open for 17 years).

This means fewer interruptions in recurring billing due to changed payment info, leading to lower customer churn for the business.

In summary, recurring ACH payments are used by many groups for a simple reason: they make repetitive transactions easier for both sides.

Whether you’re an individual making sure your bills get paid automatically, or a business ensuring you receive dues on time, ACH provides a low-cost, reliable way to automate those transfers and keep things running smoothly.

Benefits of Recurring ACH Payments

Why choose recurring ACH payments over other methods? Here are some key benefits of using recurring ACH, for both businesses and consumers:

- Convenience and Time Savings: Once set up, recurring ACH payments are “set it and forget it.” For payers, there’s no need to remember due dates or manually initiate each payment. Bills are paid on time automatically, which is extremely convenient.

For businesses, automation means far less administrative work – no need to generate and send repetitive invoices or process checks every billing cycle. This frees up time to focus on more important tasks rather than chasing payments.

Essentially, each recurring payment runs in the background with minimal intervention, reducing human error and the risk of forgetting a payment. - Predictable Cash Flow: Recurring ACH provides steady and predictable revenue for businesses. Knowing that, for example, on the 1st of every month a certain amount of revenue will arrive via ACH helps in planning budgets and managing finances.

It smooths out cash flow since you can rely on a schedule of incoming funds. Individuals can also benefit from predictability – automatic transfers can help ensure you always contribute to savings or investments on a schedule, building good financial habits. - Lower Transaction Fees: ACH transfers are highly cost-effective compared to many other payment methods. For consumers, there’s usually no fee at all to make or receive an ACH payment.

For businesses, the cost is typically just a few cents or a small percentage per transaction, often capped at a low amount. For example, some payment processors charge around 0.5% per ACH transaction with a maximum fee of $5–$6.

In many cases, ACH fees range from $0 to $3 per payment. This is significantly cheaper than credit card processing fees (which are around 2–4% of each transaction) or wire transfers (which can cost $15–$35 each).

Therefore, businesses can save a lot on payment processing by encouraging ACH for recurring payments – especially for high-ticket items or high volume billing. - Fewer Late Payments (Improved Reliability): Because payments are automated on the due date, there is much less chance of a payment being late or missed.

Customers who opt for recurring ACH are less likely to forget a bill, meaning businesses deal with fewer collections issues and late fees.

Timely payments keep the accounts receivable clean and reduce the need for follow-ups or dunning notices. For the payer, this also means avoiding late fees or service interruptions since the bill is taken care of automatically. - Better Customer Retention: Offering ACH as a payment option can enhance customer satisfaction. Some customers prefer paying from their bank account (especially those who don’t want to use credit cards or who may not have a credit card).

ACH payments can be seen as a hassle-free way to pay, which improves the overall user experience. Moreover, as noted, bank account details change less frequently than credit card details, so customers on ACH are less likely to unintentionally churn due to payment method failures (like an expired card).

This means businesses can maintain long-term relationships with those customers with fewer hiccups in billing. - Enhanced Cash Management: With recurring ACH, businesses can more easily forecast and manage cash. You know exactly when money will leave or enter your account, enabling better scheduling of your own obligations.

It also reduces the risk of overdrafts for businesses if managed properly, since you can plan transfers on dates that align with your cash availability.

For consumers, it can help align bill payments with paydays – for instance, scheduling important payments just after you receive your paycheck via direct deposit. - Security and Fraud Protection: ACH payments are generally considered secure. They move through the banking system, which employs encryption and authentication protocols to protect data.

Unlike mailing a check (which can be lost or stolen from the mail), ACH is electronic and less exposed to those risks. Additionally, because ACH pulls from bank accounts, there’s no exposure of sensitive credit card numbers with each transaction – the bank info is provided once at setup and typically stored securely by the business or processor.

There are also federal safeguards and regulations for ACH transfers (we’ll detail those later), giving consumers recourse in case of unauthorized transactions.

Overall, while no payment method is 100% fraud-proof, ACH’s track record is strong, and recurring ACH in particular is low-risk when proper authorizations are in place. - Cost Savings and Efficiency for Large Volumes: If you handle a large number of recurring transactions, ACH’s low fees become a huge advantage. Consider a company billing 1,000 customers $100 each every month.

If done by credit card at ~3% fee, it would cost about $3 per transaction, or $3,000 in fees monthly. By ACH at perhaps $0.20 or 0.5%, the fee might be a few hundred dollars at most – a significant saving.

Furthermore, processing in batch through ACH is efficient – thousands of payments can be handled automatically without individual manual processing, reducing labor costs. - Eco-Friendly (Paperless): Moving money electronically via ACH means reducing paper use (no more paper checks, envelopes, stamps, etc.). Companies can cut down on mailing invoices or bills by simply notifying customers of upcoming ACH drafts.

This not only saves money on paper and postage but is also environmentally friendly. It’s a small “green” benefit that aligns with sustainability initiatives. - Flexibility in Amounts (AutoPay vs. Fixed): Recurring ACH can handle both fixed recurring amounts and variable amounts with proper authorization.

For instance, AutoPay for utility bills might pull a different amount each month based on usage (with the customer’s prior consent for variable billing), whereas a subscription is a fixed amount each time.

The flexibility means it can accommodate various billing models – fixed subscriptions, usage-based bills, installment plans, etc., all through the same network.

In summary, recurring ACH payments offer low costs, high convenience, and reliable automation, making them extremely beneficial especially for routine payments. They simplify life for individuals by automating bill pay, and they provide businesses with a cost-effective tool to streamline revenue collection and expense payments.

Drawbacks and Challenges of Recurring ACH Payments

While recurring ACH payments have many advantages, it’s important to be aware of their limitations and challenges. Here are some potential drawbacks to consider:

- Slower Processing Time: ACH is not instant, and this delay can be a drawback if you need funds immediately. Unlike credit card payments which are authorized almost instantly, an ACH transfer typically takes 3–5 business days to fully settle.

This means businesses might have to wait a few days to actually access the money from a payment. If you’re relying on a payment to cover a near-term expense, the lag can be inconvenient.

For urgent payments or last-minute needs, ACH might be too slow (in those cases, a wire transfer or card payment could be more appropriate despite higher costs).

Businesses must plan around the ACH timing – for example, initiating payroll or vendor payments a couple of days early so that they clear by the due date.

The processing time also means that if a customer’s payment fails (e.g., for insufficient funds), you might not find out until a few days after the attempt. - Risk of Insufficient Funds and Payment Returns: Because ACH pulls from bank accounts, there’s a chance a scheduled payment might bounce if the payer doesn’t have enough money in their account.

An insufficient funds (NSF) situation can result in the payment being declined or returned by the payer’s bank. When this happens, the business doesn’t get paid, and they may incur a returned item fee from their bank.

They’ll also need to reach out to the customer to resolve the issue, possibly having to attempt the debit again or arrange another payment method. Repeated failed payments can strain customer relationships and create additional work (collections, fees, etc.).

For consumers, if an ACH debit is returned NSF, their bank might charge an overdraft or NSF fee as well. Thus, keeping track of account balances and timing is crucial. - Customer Bank Account Changes: If a customer closes their bank account or switches banks and forgets to notify the business, recurring ACH payments will start failing.

Unlike credit cards which notify merchants of updated card info through updater services, bank account changes rely on the customer to inform the biller. Customers may close or change accounts without notice, causing transactions to be rejected.

It then falls on the business to contact the customer and obtain new payment details, which is an extra administrative burden. There’s also a risk of unintended payment disruption during the gap. - Setup and Onboarding Effort: Implementing recurring ACH payments requires an upfront effort. Businesses need to obtain proper authorizations (signed forms or equivalent) from customers and set up the technical capability to send ACH entries (often by partnering with a payment processor or their bank).

This setup can involve paperwork and possibly some cost or vetting from the bank (banks often require businesses to apply for ACH origination services). The initial integration and compliance checks can be time-consuming.

From the customer’s perspective, signing up for ACH might be slightly less convenient upfront than, say, entering a credit card.

They have to provide bank routing and account numbers and may need to fill out a form or agreement – a step some find cumbersome. However, this is typically a one-time hassle and then the automation pays off. - Limited to Domestic Transactions: As mentioned earlier, ACH is mainly a U.S. system. If a business has international clients or needs to collect payments from bank accounts abroad, ACH isn’t directly an option.

You would need alternative methods (international ACH services, wires, or local debit arrangements). This limited reach can complicate things for companies with global customers – they might have to maintain multiple payment methods.

In short, ACH has limited international reach, which can be a drawback in an increasingly global economy. - Transaction Limits: Some banks or processors impose limits on ACH transactions, either per transaction or daily/monthly volume limits.

For example, a bank might limit ACH transfers to $25,000 per transaction for risk reasons. If you have very high-value recurring payments (say $50,000 monthly), you might need to split them or get a special arrangement.

These ACH limits can be restrictive for large transactions. Wire transfers, in contrast, can often handle much larger amounts in one go (but with higher fees).

It’s important to check with your provider what limits apply to your ACH transactions, especially if you plan to use it for big payments. - Potential for Errors and Reversals: Occasionally, mistakes happen – perhaps an incorrect amount is debited or a payment is duplicated. Correcting an ACH error can be a lengthy process.

If a wrong amount was pulled, the business might need to issue an ACH credit back to the customer or handle a refund.

ACH does allow for reversals in limited circumstances (such as if a payment was made in error or was a duplicate), but reversals must be initiated within five business days and meet specific criteria.

Investigating and resolving any ACH discrepancies requires coordination with banks and can take time. During that period, funds might be in limbo or the customer might be inconvenienced. - Customer Disputes and Chargebacks: Although ACH payments are authorized, customers do have rights to dispute transactions in certain cases.

For consumer ACH debits, a customer can dispute an unauthorized recurring payment (say they never agreed to it, or the amount was wrong) and request a refund.

Under banking rules and Regulation E, a consumer has 60 days from the statement date of an ACH debit to dispute it as unauthorized and get it reversed.

When a dispute (often called an ACH chargeback in this context) occurs, the business might lose that payment and have to work out the issue with the customer.

Handling disputes can be challenging – it might result in lost revenue and require time to research the customer’s claim, gather proof of authorization, etc.

The good news is that disputes are less common in ACH than with credit cards, but they can happen (for example, if a customer forgot they signed up, or genuinely didn’t authorize it). - Fraud Risk and Security Responsibilities: ACH transactions are generally secure, but they are not completely immune to fraud. If an unauthorized party obtains someone’s bank account information, they could attempt fraudulent ACH withdrawals.

Businesses therefore must implement security measures to detect and prevent fraud – such as verifying bank accounts before activating recurring billing, monitoring for unusual payment requests, and using encryption to store bank data.

Nacha rules require certain security practices, especially for internet-initiated debits (like verifying the first payment for new accounts to combat fraud). All this means businesses have to stay vigilant.

If fraud occurs, resolving unauthorized debits can be troublesome for both the customer (who has to go through the dispute process) and the business (which might incur losses or penalties if they were the source of a fraudulent debit). - Compliance and Regulatory Burden: Using ACH comes with rules that businesses must follow (explored more in the next section). There are Nacha operating rules around authorizations, notifications, and data handling that must be adhered to.

Non-compliance can lead to fines or being barred from ACH processing. For small businesses without dedicated legal or compliance teams, keeping up with these requirements can be challenging.

Examples include maintaining proof of authorization for each recurring payment, abiding by formatting rules for ACH files, and staying updated on rule changes (like new security requirements).

While payment processors often assist with compliance, the ultimate responsibility lies with the business originating the payments. In short, regulatory compliance is an ongoing commitment when leveraging ACH, and this adds a layer of complexity. - Customer Perception and Trust: Some customers might be hesitant to share their bank account information for recurring payments due to privacy concerns or fear of being overcharged.

They might trust credit cards more because of the well-known consumer protections or simply habit. So, businesses may need to educate customers on the safety of ACH or provide incentives (like a small discount for ACH autopay) to encourage its adoption.

Overcoming this initial trust barrier is a minor challenge in some cases, although the growing familiarity with ACH (through things like online bill pay and fintech apps) is making customers more comfortable over time.

In weighing these drawbacks, many businesses still find that the benefits outweigh the challenges for recurring ACH. Most challenges can be managed with proper planning: buffer in processing time, actively communicate with customers, maintain compliance, and have contingency plans for failed payments.

Understanding these potential issues means you can put measures in place (like reminding customers to update expired account info, or keeping a line of credit for cashflow while waiting for ACH settlements). Now, let’s compare ACH with other payment methods to see where it stands.

Recurring ACH vs. Other Payment Methods

How do recurring ACH payments stack up against other common payment methods like credit card payments or wire transfers? Below is a comparison highlighting key differences in suitability for recurring transactions, cost, speed, and other factors:

| Aspect | Recurring ACH Payments | Recurring Credit Card Payments | Wire Transfers |

|---|---|---|---|

| Suitable for Recurring? | Yes – ACH is designed for automated, recurring transfers. Commonly used for subscriptions, bill payments, payroll, etc. | Yes – credit/debit cards can be stored on file for recurring billing (e.g., monthly subscriptions). However, cards can expire or be canceled, requiring updates. | Not typically. Wires are generally one-off payments; scheduling a recurring wire is rare due to high cost and manual setup. |

| Cost to Business | Low cost. ACH fees are minimal: often just a few cents or a fraction of a percent per transaction, sometimes capped (e.g., max ~$3–$5 per transfer). Many banks don’t charge consumers for ACH. | Higher cost. Card processing fees typically range ~2%–4% of each transaction (plus ~$0.30). Businesses lose a slice of every payment to fees, which adds up for recurring charges. | High cost. Domestic wires often cost ~$15–$35 per transfer for the sender (and sometimes $10–$20 for the receiver). International wires cost more. Not economical for routine payments. |

| Speed of Transfer | Standard: 1–3 business days to settle (ACH batches process during the day/night). Same-day ACH is available for faster processing if needed (funds can arrive the same day if sent in special windows). | Fast Authorization: Transactions are authorized in seconds; the merchant typically sees confirmation instantly. Settlement of funds to the merchant usually occurs within 1–2 business days. From the payer’s perspective, the card charge is immediately reflected in available credit. | Immediate (near real-time): Wires are processed in real-time or same-day for domestic. Once sent, funds can be available within minutes to hours if within the same country. There’s no concept of recurring batch – each wire is individually sent and received swiftly. |

| Risk of Failure/Dispute | Possible ACH returns: If payer’s account has insufficient funds or is closed, the ACH will bounce back (usually within 1–2 days of initiation). Consumers can dispute unauthorized ACH debits within 60 days, which can claw back funds. | Chargebacks: Cardholders can dispute charges (e.g., as fraudulent or unwanted) typically up to 60–120 days or more, depending on card network rules. Chargebacks reverse the payment and often incur fees for businesses. Cards can also decline if over limit or frozen. | Irrevocable (mostly): Once a wire is completed, it’s generally final. Errors or fraud in wires are hard to reverse. No chargeback mechanism; banks can rarely reclaim funds after the fact except in cases of clear mistakes. This finality means no ongoing dispute risk, but also no protection if something was wrong. |

| Ease of Setup & Automation | Setup: Requires bank account info (routing & account number) and a signed authorization for recurring debits. Many billing systems support ACH automation once the account is linked. Automation: Very easy after setup – payments are pulled on schedule without manual effort each time. | Setup: Requires collecting customer’s card details and permission to charge it periodically. This is often user-friendly (web forms, saved card on file). Automation: Easy – businesses can automatically charge the saved card on schedule. But need to handle card updates (expire every 3–4 years, etc.). | Setup: Manual for each payment. Typically requires initiating each wire via bank (online or in branch) – entering details each time, or at best using a template. Some banks allow scheduled recurring wires, but the high fees and need for manual review make it uncommon. Automation: Very limited – wires are best for intentional, one-time sends. |

| Consumer Perspective | Directly from bank account, no debt involved. Must provide bank info and trust the company to debit as agreed. No rewards or points (unlike some credit cards), but also no interest or credit risk. Good for those who prefer using funds they have and avoiding credit. | Draws from credit line (or debit account if using a debit card). Easy to set up and familiar to consumers. Many like earning credit card rewards on payments, but running a balance accrues interest. Risk of overspending if using credit. Consumers often feel protected by card fraud liability rules for disputes. | Typically used for large, important payments (house closing, etc.), not day-to-day bills. Consumer must initiate or actively approve each wire. High trust and finality – you wouldn’t set a recurring wire lightly. Mostly irrelevant for normal consumer subscriptions due to cost and hassle. |

| Security | Highly secure network with bank-level encryption; data is handled by banks and processors with strict standards. Account info is sensitive but given once to a trusted party. Fraud incidence is low, and banking regulations protect against unauthorized pulls to some extent. | Card networks have robust security (encryption, tokenization of card info on file). However, card numbers can be stolen or misused, and merchants must keep card data secure (PCI compliance). Fraud on cards is more common, but consumers have zero-liability protections. | Wires are secure in transit, but if sent to the wrong account (or a fraudster), money can be lost with little recourse. No recurring storage of data needed since each wire is authorized anew. Generally secure as long as banking instructions aren’t compromised by scams (like phishing). |

Table: Comparison of recurring ACH payments vs. credit card recurring payments and wire transfers. We see that ACH stands out for recurring use due to its low cost and easy automation, whereas credit cards offer speed and familiarity at a higher cost, and wires are fast but impractical for routine schedules.

What about paper checks?

Before electronic methods, many recurring payments were handled by mailing checks. ACH has largely replaced that for convenience and speed. Unlike a check that you have to write and mail each time, an ACH debit happens automatically.

This means no postage, no mail float, and less chance of lost payments. It’s also easier to track digitally. Therefore, for U.S. domestic payments, ACH is generally superior to paper checks for recurring transactions in almost every way.

In conclusion, recurring ACH payments are often the most cost-effective choice for routine transactions, especially for larger payments or large quantities of payments.

Credit cards might still be favored for certain situations (like small consumer subscriptions or where customers insist on using a card for rewards), but they come at a premium cost.

Wires are excellent for urgent, high-value, or international transfers, but they are overkill for repetitive domestic billing. Many businesses offer multiple options; for example, they might let customers pay by ACH (bank draft) or by credit card, and some even incentivize ACH by waiving a convenience fee or offering a discount for using a bank draft.

How to Set Up Recurring ACH Payments (Step by Step)

Setting up recurring ACH payments involves both the payer (who is authorizing the payments) and the payee (who will receive the funds). Below is a step-by-step guide, primarily from the perspective of a business or freelancer setting up recurring ACH to collect payments from customers. We’ll also touch on how consumers can set up their own recurring ACH payments for bills.

For Businesses or Freelancers – Setting Up ACH Autopay from Customers

- Choose an ACH Payment Solution: First, decide how you will process ACH payments. Options include using your bank’s ACH services or partnering with a third-party payment processor (such as Stripe, PayPal, GoCardless, Helcim, etc.) that supports ACH debits.

Many modern invoicing or subscription billing platforms have ACH capability built-in. If you go through your bank, you may need to apply for an ACH originator service and potentially use software to upload payment files.

Using a payment processor can simplify things as they handle much of the technical work (usually for a fee per transaction). Pick the solution that fits your volume and technical comfort – for small businesses, a payment service or accounting software integration is often easiest. - Obtain Customer Authorization: This step is crucial. You must get each customer’s explicit permission to debit their account on a recurring basis. Typically, you’ll provide an ACH authorization form (paper or electronic) for them to fill out and sign.

The form should clearly state the payment amount (or how it’s determined), frequency (e.g., “on the 1st of each month”), start date, and how to cancel. It will also request the customer’s bank routing number and account number, plus their name and date.

If the authorization is done online or over the phone, ensure it meets Nacha’s standards (for phone authorizations, you need either a written confirmation or recorded verbal consent). Keep a record of this authorization – Nacha rules require you to retain it (usually for two years after the last payment) as proof. - Set Up the Recurring Payment Schedule: Using your chosen ACH platform, input the customer’s bank details and schedule the recurring transactions.

For example, in a billing software, you’d create a subscription or recurring payment profile: enter the customer’s bank info, the amount to charge, and the billing interval. If using your bank’s system, you might schedule a repetitive transfer.

Double-check the details (especially that the routing and account numbers are correct – one transposed digit can cause failures). Some processors will do a test to confirm the account is valid before the first live debit – this helps reduce errors and is required in some cases for web-initiated payments. - Provide Confirmation to the Customer: Once scheduled, it’s good practice to send the customer a confirmation of the recurring payment arrangement. This might be a copy of the authorization or a simple email stating: “Thank you for enrolling in ACH auto-pay.

We will debit $XX on April 10, 2026 and each April thereafter. You will receive a receipt after each payment.” This reassures the customer and serves as documentation of the terms. It should also include instructions on how to cancel or make changes (for example, a contact number or email for your billing department). - Ensure Compliance Measures: Make sure you are following any compliance requirements. For instance, if the payment is set up online, you are required to use a “commercially reasonable” method to verify the account and to employ fraud detection – these are part of Nacha’s security rules.

Also, if you’re debiting a consumer’s account, be aware of Regulation E requirements (we’ll discuss them in the next section) which include providing the customer a way to revoke authorization. Many processors bake compliance into their tools, but it’s wise to be informed. - Process and Monitor Payments: Once everything is set up, the recurring ACH payments will start processing on schedule. Monitor your payment reports, especially for the first payment or two, to ensure they are successful.

If a payment is returned (failed), you’ll typically get a return code indicating why (NSF, invalid account, etc.). Set up notifications if possible, so you’re alerted to any failed transactions and can address them promptly.

Most businesses will re-attempt an NSF debit once (perhaps a few days later) or as allowed by their ACH agreement. - Maintain Records: Keep a file (digital or paper) of each customer’s ACH authorization and a log of payments. This helps with any disputes or inquiries. It’s also required by Nacha that you be able to produce proof of authorization if a payment is questioned.

Also retain any communications with customers about changes or cancellations. Having a clear audit trail is part of best practices for ACH. - Handle Changes or Cancellations: If a customer needs to change their bank account for payments, you’ll need to obtain a new authorization (or at least update the details and have it acknowledged).

If they want to cancel auto-pay, they have the right to do so – make sure you process cancellations promptly to avoid any unauthorized debits after a revocation. In your system, cancel the schedule and confirm to the customer that it’s been stopped.

It’s wise to have a written policy for how customers can revoke authorization (e.g., require a written notice or an email 3 days before the next payment, etc., as long as it’s reasonable).

For Consumers – Setting Up Automatic ACH Payments for Your Bills

If you’re an individual looking to set up a recurring ACH payment to automatically pay a bill (like utilities, mortgage, etc.), the process looks a bit different:

- Through the Biller: Most companies (utilities, phone providers, insurance, etc.) offer an “AutoPay” option. You typically log into the company’s website or fill out a form, provide your bank routing and account numbers, and agree to let them draft your account each month for the amount due.

They will then take care of setting up the recurring ACH on their side. You should get a confirmation of the schedule (e.g., “We’ll debit your account on the 15th of each month for the amount due on your bill.”).

Make sure you understand if the amount can vary (for bills that change each month) and that you’re comfortable with that. Once done, just ensure you keep enough balance in your account before the debit date. - Through Your Bank (Bill Pay): Alternatively, you can use your own bank’s online bill pay service to push payments out. When you set up a payee in online banking, in many cases the bank will send an ACH credit to the company (or a paper check if electronics aren’t available).

You can schedule these to recur. For example, you could tell your bank “Send $100 on the 10th of each month to ABC Insurance, account number 1234” and the bank will handle it. This is slightly different since it’s not the company pulling from you, but rather you pushing to them.

It’s a useful approach if you prefer to control the timing from your side. However, not all companies can receive electronic payments from your bank – if not, the bank might mail a check, which is slower. - Review and Adjust as Needed: As a consumer, keep an eye on your bank statements to verify the payments are happening correctly. If a bill amount changes significantly or an extra payment is taken in error, contact the biller promptly.

Remember, you can usually stop a payment by notifying your bank at least three business days before the scheduled transfer (under U.S. law, banks must honor a stop-payment request on preauthorized transfers if given 3 days notice).

And you can cancel the arrangement entirely by revoking authorization with the biller (and you might also inform your bank to block future transfers to be safe).

Overall, setting up recurring ACH is straightforward: it’s often just a one-time form or online setup and then it runs on autopilot.

The key is always clear authorization and communication – know the who, what, when of the payments being made. In the next section, we’ll delve into those authorization rules and other compliance aspects in more detail.

Legal and Compliance Considerations (U.S. ACH Rules & Regulations)

Recurring ACH payments are subject to certain laws and network rules designed to protect consumers and ensure the integrity of the banking system. If you’re a business (or even a consumer) using ACH, it’s important to understand these legal and compliance requirements:

Nacha Operating Rules

The ACH network is governed by rules established by Nacha (the National Automated Clearing House Association). All banks and businesses that use ACH must adhere to these rules. Key Nacha requirements for recurring ACH include:

- Authorization Requirement: You must have authorization from the account holder for ACH debits. For recurring entries, this authorization generally needs to be in writing and signed (or similarly authenticated, like electronically signed).

The authorization should clearly state it’s for recurring payments, the timing, and the amount (or how amount is determined).

If authorization is done orally (e.g., over a recorded phone line), Nacha rules – reinforced by the 2021 “Meaningful Modernization” update – require either a written notice sent after or compliance with the voice authorization standards (including recording the call and providing revocation instructions).

In short: no matter how it’s obtained, document that the customer agreed to these recurring debits. - Consumer’s Right to Receive a Copy: If the customer requests a copy of their authorization, you need to be able to provide it. This ties into recordkeeping – keep the signed authorization (paper or digital) on file for at least two years after the last payment, per Nacha rules.

- Revocation (Cancellation) Rights: A customer has the right to revoke an ACH authorization. Nacha rules say that the authorization is to remain in effect until the customer revokes it, and the authorization form should spell out how they can revoke it.

Once revoked, you (the business) should not initiate further debits. Failing to honor revocations can lead to disputes and potential rule violations. - Prenotifications (Optional): Nacha allows an optional process called a “prenote” – a zero-dollar test transaction you can send at least 3 days before the first real debit to verify the account info.

Prenotes are not mandatory, but some businesses use them to ensure account details are correct (the receiving bank will respond if the account/routing is invalid, for example). Alternatively, many use micro-deposits or instant verification nowadays to confirm accounts. - Timely Processing of Returns: If a debit is returned (like NSF or account closed), Nacha rules specify timelines for re-presenting entries or handling certain returns.

For instance, an NSF can be re-submitted up to two more times (often companies will try again in a few days, but best practice is to get customer permission for reattempt to avoid surprise double-dips). - Unauthorized Return Rate Thresholds: Nacha monitors the percentage of ACH transactions that get returned as “unauthorized.”

If a business has too many unauthorized returns (for example, customers saying “I didn’t authorize this” – return reason code R10/R11), it can trigger warnings, fines, or suspension from the network.

This threshold currently is 0.5% for unauthorized returns. Similarly, there are thresholds for overall returns and data quality issues. Essentially, this means you must only debit people who authorized it, and keep those disputes very low.

If you get an unauthorized claim, you should reach out to the customer and double-check your processes. - Data Security: If you store customers’ bank account information (account numbers, etc.), Nacha rules require that you protect this sensitive data.

Since 2021, Nacha has a rule that account numbers stored electronically by businesses must be rendered unreadable when stored (i.e., encrypted at rest) to prevent data breaches.

If you’re using a reputable payment processor, they will handle this securely on your behalf. But if you somehow keep that info in your own system, you need proper encryption and access controls. - WEB Debit Account Verification: A relatively new Nacha rule requires that for ACH debits authorized over the internet (WEB entries), the business must use an “account verification” method for the first payment.

This is to prevent fraud (e.g., someone using a stolen account number). Methods include things like micro-deposit verification, instant account authentication via a service like Plaid, or checking an account validation database. If you have an online sign-up for recurring ACH, ensure you incorporate such a step.

Regulation E (Electronic Fund Transfer Act)

In the U.S., consumer electronic payments (which include ACH debits from consumer accounts) are protected by the Federal Reserve’s Regulation E. Key points from Reg E for recurring ACH:

- Preauthorized Transfer Consent: Reg E requires that preauthorized electronic fund transfers (EFTs), like recurring ACH debits, have the consumer’s written authorization (or similarly authenticated consent) and that a copy is provided to the consumer.

This aligns with Nacha’s rules. So both the network rules and federal law demand proper authorization. - Consumer Right to Stop Payments: A consumer can stop a specific payment by notifying their bank at least three business days before the scheduled transfer.

For example, if a debit is coming on the 15th, the consumer can tell their bank by the 12th, “stop that payment.” The bank will then block it (and typically charge the consumer a stop-payment fee).

This is a safety net if the consumer is unable to quickly reach the merchant or just wants to ensure a particular payment doesn’t go through (perhaps due to a dispute with the merchant).

As a business, you might not know this happened until you receive a return code from the bank indicating a stop payment. - Error Resolution and Unauthorized Charges: If a consumer sees a recurring ACH debit on their statement that they believe is unauthorized or incorrect, they can dispute it with their bank.

Under Reg E, they generally have 60 days from when the bank sent the statement showing the problem transaction to notify the bank of the error. The bank then must investigate and, if it indeed was unauthorized, recredit the consumer’s account.

Common scenarios: the consumer revoked the authorization but charges kept coming, or they never signed up in the first place.

From the business side, if you receive an “unauthorized” return, you should cease future debits and might need to resolve directly with the customer. Also, too many unauthorized disputes can lead to Nacha compliance issues as noted. - Receipts and Statements: For preauthorized transfers that vary in amount (not the same each time), Reg E requires that the company notify the consumer of the amount and date at least 10 days before the transfer, if it’s outside a range the consumer agreed to.

Alternatively, some agreements set a range or a method to find out the amount (like “we will debit your utility bill amount, which you can see on your monthly statement or online”).

Most recurring ACH debits are fixed amounts, but if not, be aware of this notice requirement. Consumers will also see each ACH on their periodic bank statements, which acts as a record.

Penalties for Non-Compliance

Ignoring the rules can be costly. Nacha can impose fines for rule violations – starting from a few thousand dollars and rising for repeated or egregious issues.

In extreme cases, a company could be banned from using ACH if they pose a risk to the network (for instance, if they engage in fraudulent debits or have excessive unauthorized returns).

On the legal side, consumers could take legal action (or regulators could) if a company systematically doesn’t follow EFTA/Reg E (there are statutory damages for not obtaining proper authorization, etc., though that’s uncommon if you adhere to standard practices).

Additionally, banks themselves often require compliance via the contracts you sign for ACH services – a bank might terminate your ACH origination service if you generate too many problems.

In summary, to stay compliant with recurring ACH payments:

- Always get and document the customer’s permission (authorization) before the first debit.

- Give the customer a way to cancel future payments, and honor such requests promptly.

- Use secure methods to handle bank data and consider account verification tools to prevent fraud.

- Monitor your return/dispute rates and address any issues causing unauthorized returns.

- Provide receipts or statements as needed and be transparent with customers about their payments and rights.

Following these guidelines keeps your ACH processes running smoothly and maintains trust with your customers.

It also aligns with the “people-first” approach – respecting customers’ control over their accounts and keeping them informed, which in turn enhances your credibility (an important aspect of E-E-A-T: Experience, Expertise, Authority, and Trustworthiness).

(Note: The above is general information and should not be considered legal advice. For specific situations, especially if you handle large volumes of ACH, consulting the Nacha rules or a payments attorney is wise.)

Frequently Asked Questions (FAQs)

Q1. What is a recurring ACH payment in simple terms?

A1. A recurring ACH payment is an automatic electronic transfer of funds that happens on a regular schedule via the ACH network.

It’s like setting up an auto-pay – once you authorize it, your bank sends or withdraws money at set intervals (e.g. monthly) without further action needed. It’s commonly used for things like subscription fees, recurring bills, or paycheck deposits.

Q2. How do I set up a recurring ACH payment?

A2. To set one up, you generally provide your bank account details (routing and account number) to the party you want to pay or get paid from, and you sign an authorization for recurring withdrawals.

For example, to auto-pay a utility bill, you can give the utility company a voided check or enter your bank info on their website and agree to the monthly drafts.

Businesses can set up recurring ACH collections through their bank or a payment processor by obtaining customer authorization and scheduling the payments in a billing system. Essentially, it involves an initial signup form and then the payments will be automated each cycle.

Q3. Are recurring ACH payments safe to use?

A3. Yes – recurring ACH payments are generally very safe. They run on the banking system’s secure networks with encryption and authentication protocols.

There are also regulations to protect consumers in case of unauthorized transactions (you can dispute fraudulent or incorrect charges and get your money back in many cases).

Unlike handing over a check (which has your account info visible) or cash, ACH transfers happen quietly and securely bank-to-bank.

However, you should always only set up ACH with trusted parties and monitor your bank statements. Businesses must keep your data secure and follow strict rules, which adds to the safety of ACH.

Q4. How much does it cost to make a recurring ACH payment?

A4. For consumers, most of the time it’s free – banks usually don’t charge individuals for ACH transfers (for example, there’s no fee when your insurance company auto-debits your premium via ACH).

For businesses, ACH is very low cost compared to other methods. They might pay around $0.20 to $1 per transaction or a small percentage fee (often capped at a few dollars).

In contrast, credit card recurring payments would cost them a few percentage points of the amount each time. So ACH is a cost-saver for businesses and typically fee-free for the paying customer.

Q5. How long do recurring ACH payments take to process?

A5. They usually take around 1–3 business days to complete, and sometimes up to 5 days depending on timing. For example, if your payment is scheduled on a Friday, the debit might show up on Monday and the funds reach the recipient by Tuesday.

ACH doesn’t process on weekends or bank holidays, so those don’t count in the timeline. Some payments can go through the same day if sent early and marked for same-day processing, but most recurring payments are set a couple of days in advance to ensure they arrive on time.

Q6. What if I need to cancel a recurring ACH payment?

A6. You can cancel (revoke) a recurring ACH authorization at any time. The best way is to notify the company or party that’s debiting your account and follow their cancellation procedure (e.g., submit a written request or an online form).

It’s wise to do this at least a few days before the next scheduled payment. Additionally, you have the right to contact your bank and issue a stop payment order for the specific authorization – if you do this at least three business days before the next debit, the bank will block it.

Always verify that the cancellation was processed; you should get confirmation from the biller. After cancellation, any further ACH debits from that company should not occur – if they do, you can dispute them as unauthorized.

Q7. Can ACH payments be set up for international transfers or only within the U.S.?

A7. Standard ACH payments (including recurring ones) are for U.S. bank accounts only – the network is domestic. You cannot directly ACH money from a U.S. bank to a foreign bank through the normal ACH system.

For international recurring payments, some specialized services or “international ACH” arrangements exist, or more commonly, businesses use wire transfers or local bank debit systems in each country.

If you have, say, a recurring rent payment to a landlord overseas, you’d likely use an international money transfer service rather than ACH. Always check the best method for cross-border payments, since ACH won’t work in that case.

Q8. How do recurring ACH payments compare to recurring credit card payments?

A8. Both can accomplish the same goal of automatically paying bills, but there are differences. ACH pulls directly from a bank account, usually at a lower cost (no hefty card processing fees) and with a few days processing time.

Credit card payments charge your line of credit, often instantly, and you might earn rewards points – but the merchant pays higher fees (which sometimes get passed to you in prices or convenience fees).

ACH payments won’t contribute to credit card debt and don’t have card expiration issues, whereas credit card autopay might fail if your card expires or gets replaced (requiring you to update the info).

Also, if you’re maxed on your credit limit, an ACH from your bank might be preferable to ensure payment. On the flip side, credit cards offer strong dispute rights and zero liability for fraud – with ACH, while you still have protections, it’s a direct hit to your bank balance if something goes wrong until it’s resolved.

Many people use ACH for large or regular bills (like mortgage, rent, utilities) and reserve credit cards for variable or discretionary spending.

Q9. Will I get notified for each recurring ACH payment?

A9. This depends on the biller or platform. It’s common to receive email notifications or receipts each time an ACH payment is processed (for instance, “Your account was debited $120 for your utility bill on 10/05”).

Some services even send a reminder a few days before the debit. However, not all do – because the payment is automatic, they might only show it on your monthly statement. It’s a good idea when signing up to check if there’s an option to receive reminders or receipts.

If you need a receipt for each payment, most companies can provide one either by email or accessible through your online account with them. Businesses should note that providing a receipt or confirmation is part of good customer service and, in some cases, a compliance best practice (especially if amounts vary).

Q10. What happens if a recurring ACH payment date falls on a weekend or holiday?

A10. If the scheduled date falls on a non-business day (weekend or bank holiday), the ACH debit will typically occur on the next business day. For example, if your usual schedule is the 15th of each month, but in April the 15th is a Sunday, the ACH would likely be initiated on Monday the 16th.

Some billers might pull it slightly earlier on the prior business day – it depends on their policy (they will usually disclose this in the terms). Always check with the specific company; however, standard practice is next business day.

This is another reason to keep an eye on timing and not assume the money left your account on a Saturday – it might not actually debit until Monday.

Conclusion

Recurring ACH payments are a foundational tool in U.S. finance, enabling seamless, automated transactions that benefit both payers and payees.

By understanding what they are and how they work, you can harness their advantages—such as lower costs, timely payments, and reduced administrative burden—to improve your financial routines or business operations.

From small business owners ensuring they get paid on time, to freelancers simplifying client billing, to everyday consumers automating their monthly bills, recurring ACH transfers offer a reliable and efficient solution for managing repeat payments.

In this 101 guide, we covered the key points: we learned that recurring ACH payments move money directly between bank accounts on a schedule with the proper authorizations in place. We broke down the process steps and typical timeline (usually a few days) so you know what to expect.

We also compared ACH with alternatives like credit cards and wires – highlighting ACH’s strengths in cost and convenience, as well as its limitations (like being U.S.-only and not instant).

Importantly, we delved into the legal side, emphasizing the need for clear authorization and compliance with Nacha rules and federal regulations to keep everything above board and secure.

As with any financial tool, there are pros and cons. ACH isn’t ideal for every situation (for instance, an emergency same-day payment might call for a wire), but for the majority of recurring transactions, it strikes an excellent balance of economy and efficiency.

By focusing on people first – ensuring customers are informed, consent is obtained, and their experience is smooth – businesses can use ACH to build trust and loyalty (customers appreciate hassle-free, error-free billing).

Simultaneously, maintaining strong E-E-A-T principles (demonstrating expertise and trustworthiness by following best practices and regulations) will safeguard your operations and reputation when using ACH.

In summary, recurring ACH payments can be thought of as the quiet workhorses of the payment world: not flashy, not instantaneous, but dependable and cost-effective. They keep cash flowing and the wheels of commerce turning with minimal friction.

Whether you’re collecting subscription revenue, paying your team, or just making sure your electric bill is paid automatically each month, recurring ACH is a friend you’ll be glad to have in your financial toolkit.

With this knowledge, you can confidently set up and manage recurring ACH payments, leveraging their benefits while staying mindful of compliance and customer care. Here’s to on-time payments and smoother financial operations for all!

Leave a Reply