The ACH Network is the quiet engine of American banking. It moves salaries on payday, funnels your mortgage payment to your lender, pulls your utility bill, and settles billions in B2B invoices.

In this guide, you’ll learn how the ACH Network actually works, who the players are, what it costs, how long transfers take, and how new rules (like Micro-Entries, WEB debit account validation, and data-security requirements) are reshaping risk and compliance.

You’ll also get practical, U.S.-specific checklists for setting up ACH for payroll, bill pay, subscriptions, and B2B payments—plus an FAQ to keep handy.

What is the ACH Network—and Why it Matters in the U.S.

The Automated Clearing House (ACH) Network is a batch-based electronic payment system that lets U.S. financial institutions push and pull money between bank accounts.

Think direct deposit (ACH credits), auto-debits for bills (ACH debits), business vendor payments, tax refunds, and more. It’s governed by Nacha’s Operating Rules and operated by two central clearing operators: the Federal Reserve (FedACH) and The Clearing House (Electronic Payments Network).

ACH’s strengths are reach (virtually every U.S. bank participates), reliability, and cost-efficiency compared to cards and wires. It also powers “Same Day ACH,” a faster option with multiple daily windows and a per-transaction limit of $1 million, greatly expanding high-value use cases for businesses from 2022.

Unlike card rails that authorize in real-time, ACH batches entries on set schedules. Funds availability and settlement depend on processing windows, bank posting times, and whether you’re sending standard next-day ACH or Same Day ACH.

Despite being “batch,” the network is modern and growing: by Q3 2025, the ACH Network processed 8.8 billion payments totaling $23.2 trillion, with B2B payments growing at a double-digit clip year-over-year—evidence of ACH’s integral role in U.S. commerce.

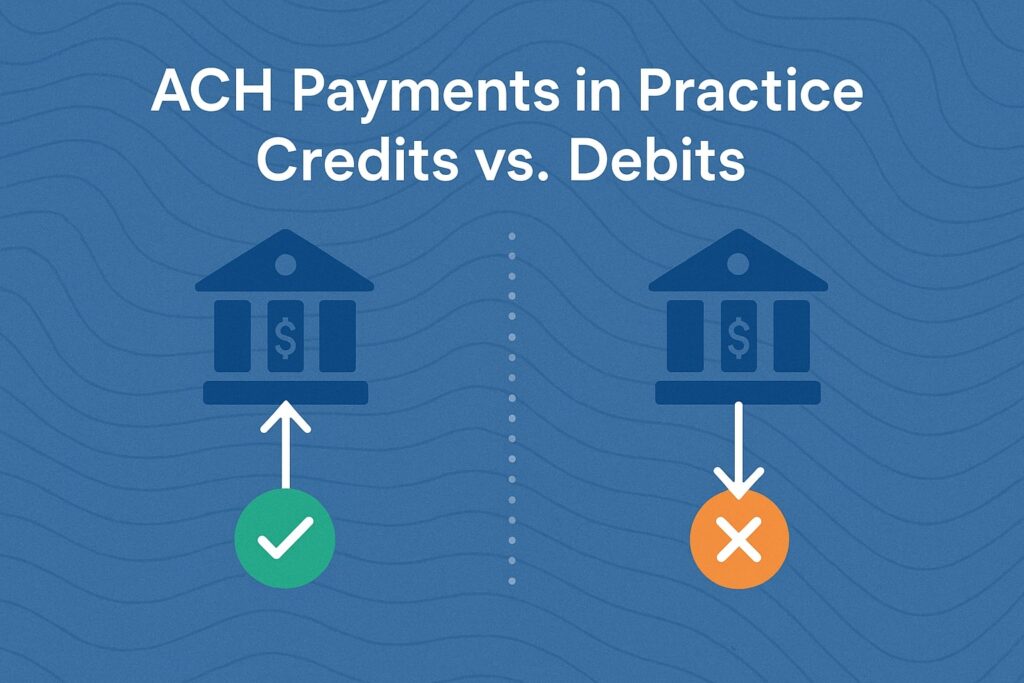

ACH payments in Practice: Credits vs. Debits (and Common U.S. Use Cases)

ACH credits push money from the Originator to the Receiver—classic example: payroll direct deposit. A business (or its payroll provider) initiates a credit file at its bank (the ODFI).

The ACH operator routes the entries to receiving banks (RDFIs), which post the funds to employee accounts. This same flow supports vendor payments, government benefits, and tax refunds.

ACH debits pull money with the Receiver’s authorization—classic example: recurring bill pay for utilities, insurance premiums, or subscriptions.

A merchant or biller gets the customer’s ACH authorization (written/electronic/recorded oral where permitted), originates a debit via its ODFI, and funds are pulled from the customer’s account at the RDFI on the due date.

Popular U.S. use cases:

- Payroll and benefits (ACH credit): Affordable, near-universal, predictable.

- B2B vendor pay (ACH credit): Remittance addenda can carry invoice data; Same Day ACH can accelerate cash flow.

- Recurring billing (ACH debit): Great for predictable subscriptions and installment plans.

- Consumer bill pay (ACH debit/credit): Utilities, rent, tuition, and healthcare bills.

- Account funding/cash-out for fintechs: Micro-Entries and WEB debit validation are standard defenses to reduce fraud.

The Four Essential Parties in Every U.S. ACH Payment

- Originator: The business, government, or individual initiating the payment (e.g., an employer or a merchant).

- ODFI (Originating Depository Financial Institution): The Originator’s bank that sends entries into the network and warrants compliance.

- RDFI (Receiving Depository Financial Institution): The Receiver’s bank that posts incoming ACH entries to customer accounts.

- Receiver: The person or entity receiving/being debited or credited.

Nacha’s rules assign warranties and responsibilities primarily to the ODFI for origination quality and to the RDFI for posting and exception handling.

When exceptions occur (incorrect account numbers, insufficient funds, unauthorized debits), standard return codes (R01–R85) and timeframes govern responses, with defined thresholds for return rates—particularly unauthorized return rates capped at 0.5%—to keep network quality high.

Same Day ACH vs. standard ACH: Speed, Limits, and Timing

Standard ACH typically settles next business day (some credits can be made available sooner), while Same Day ACH provides several daily processing windows so qualifying entries can settle and post on the same banking day.

For many U.S. businesses, Same Day ACH can meaningfully accelerate payroll adjustments, just-in-time supplier payments, and urgent customer disbursements without the cost of a wire.

Key points you should know:

- Per-payment limit: Same Day ACH supports transactions up to $1,000,000 (effective March 18, 2022), up from earlier caps—expanding high-value use cases like B2B payouts and payroll off-cycles.

- Windows & posting: Multiple intraday windows exist; RDFIs must make Same Day ACH credits available no later than end-of-day. Posting times still vary by bank. (Check your ODFI’s cutoffs.)

- Eligibility: Most ACH entry classes are eligible, but not all. Your bank/processor will confirm eligibility and cutoffs.

- When to pick which: Use standard ACH for routine, date-certain cash management and lower costs. Use Same Day ACH when time is of the essence but a wire is overkill.

Authorizations, WEB Debits & Account Validation: Your Playbook for Acceptance

For every ACH debit, you must have proper authorization from the Receiver. The format can be written, electronic, or oral (if certain rules are met) and must be retained for the rule-specified period.

When the debit is collected over the internet or an unsecured network (ACH WEB entries), Nacha requires a “commercially reasonable fraudulent transaction detection system” and account validation as part of your anti-fraud controls.

The WEB Debit Account Validation Rule took effect in 2021 and has been enforced, meaning non-compliance can lead to network enforcement actions and fines. Practical options include prenotes, database lookups, and trial deposits (Micro-Entries) to validate account status and access.

Why it matters in the U.S.: WEB debits are now ubiquitous for eCommerce and subscription billing. Strong validation reduces returns (e.g., R03 No Account, R04 Invalid Account, R10 Unauthorized) and keeps your unauthorized return rate below 0.5%, a critical compliance benchmark.

Micro-Entries & Modern Account Verification (ACCTVERIFY)

Micro-Entries are small ACH credits (and optional offsetting debits) used to verify that a customer controls a specific bank account—commonly by asking the customer to confirm the penny amounts. Nacha standardized Micro-Entries with a two-phase rule:

- Phase 1 (effective Sept. 16, 2022): Defines “Micro-Entry”; requires the Company Entry Description “ACCTVERIFY” and recognizable Company Name; sets origination requirements (e.g., credits and any offset debits settle together; aggregate credits must equal or exceed aggregate debits so the customer isn’t net-debited).

- Phase 2 (effective Mar. 17, 2023): Requires commercially reasonable fraud detection for Micro-Entries, including monitoring forward and return volumes.

U.S. businesses should adopt Micro-Entries (or comparable validation) alongside WEB debit controls. Benefits include easier onboarding, lower exception handling, and stronger compliance posture.

Risk is Shifting: Credit-push Fraud & Nacha’s Framework

Historically, ACH risk programs focused on unauthorized debits. Today, credit-push fraud (e.g., vendor impersonation, payroll redirection, and business email compromise) is a top threat. Once a legitimate sender is tricked into pushing money to an attacker’s account, recovery is hard.

In response, Nacha published A Risk Management Framework for the Era of Credit-Push Fraud, calling for greater education, collaboration, and layered controls across the payment flow, including better anomaly detection, validated payee details, and rapid response processes when fraud strikes.

What to do in the U.S. context:

- Use out-of-band verification for supplier banking changes.

- Implement payment hold and review queues for high-risk, first-time, or profile-changed payees.

- Monitor behavioral signals (IP/device/velocity) for online payment instructions.

- Establish a playbook for ACH recalls, RDFI notifications, and law-enforcement referrals.

Data Security Requirements: Protecting Account Numbers at Rest

Nacha’s Supplementing Data Security Requirements expand the ACH Security Framework to require certain large, non-FI Originators, Third-Party Service Providers, and Third-Party Senders to render deposit account data unreadable at rest (e.g., encryption, tokenization) once they hit defined annual ACH volume thresholds.

Phase-in began in 2022, with additional milestones following, emphasizing stronger data-at-rest protections alongside traditional transit security. If you’re a high-volume U.S. originator or a service provider, review whether you fall in-scope and confirm your technical controls and audits align.

Returns, Disputes & Thresholds you Must Know (with U.S. Numbers)

Every ACH exception is coded with a standard return reason (e.g., R01 Insufficient Funds, R02 Account Closed, R03 No Account, R10 Unauthorized). Nacha sets quality thresholds every U.S. originator should monitor:

- Unauthorized Return Rate Threshold: 0.5%.

- Administrative Return Rate Level: 3% (e.g., account data errors).

- Overall Return Rate Level: 15%.

Exceeding levels/thresholds triggers ODFI monitoring, inquiries, and potential enforcement. Keep an eye on aging, entry class mix (e.g., WEB vs. PPD), and your onboarding/authorization controls to stay compliant and avoid fees and reputational risk.

ACH vs. Wires vs. Cards vs. Instant Rails (FedNow/RTP): Where ACH Fits

- ACH: Low cost, ubiquitous reach, batch settlement; Same Day ACH closes speed gaps for many use cases up to $1M per payment. Ideal for payroll, B2B, recurring bills, and high-value but not urgent payments.

- Wires: Real-time finality and high fees; best for urgent, high-value B2B and real estate settlements.

- Cards: Real-time authorization, higher fees, interchange complexity; best for consumer purchases and refunds with chargeback rights.

- Instant rails (FedNow/RTP): Real-time 24/7 finality; great for payouts and just-in-time funding where immediacy matters, but coverage and use cases are still expanding. ACH remains the broadest low-cost bank-to-bank option in the U.S. for scheduled and recurring flows.

Setting up ACH Acceptance (U.S.) – Operations, Compliance & UX Checklist

Banking & origination setup

- Select an ODFI or payment processor with strong ACH capabilities (Same Day windows, robust reporting, return code automation, and risk tools).

- Configure cutoff times, settlement calendars, and funding preferences.

- Ensure NACHA-aware data formats (SEC codes like PPD, CCD, WEB) and addenda support for B2B remittance.

Authorizations & validation

- Capture clear ACH authorizations (e-signature, IP/time stamps for WEB; recorded scripts for TEL if used).

- Implement WEB debit account validation and fraud screening—this is required and enforceable.

- Use Micro-Entries (“ACCTVERIFY”) or equivalent for bank account verification, and monitor volumes/returns per Phase 2.

Risk management & monitoring

- Track return rates (unauthorized ≤ 0.5%) and build alerts.

- Monitor velocity, first-payment risk, and device signatures for online debits.

- Establish credit-push fraud controls for outbound credits and supplier changes.

Data security & audits

- If you’re a high-volume non-FI originator or a TPS/TPSP, encrypt/tokenize account numbers at rest to meet the Supplementing Data Security rule timelines.

- Review SOC/ISO evidence with your vendors and document internal controls.

Customer experience

- Set clear payment descriptors and support touchpoints to reduce disputes.

- Offer Same Day ACH selectively for premium/urgent scenarios; communicate posting expectations.

Timing Deep-dive: How Long ACH Really Takes in the U.S.

ACH timing isn’t only “network speed.” It’s a combination of origination cutoff, ACH operator windows, RDFI posting policies, and funds availability rules. With standard ACH, expect next-day settlement for most entries.

With Same Day ACH, eligible entries sent before a given window can settle and be made available the same business day (credits must be available by the RDFI’s end-of-day).

For payers and payees, the practical advice is to ask your bank or processor for cutoff schedules and holiday calendars—and to plan cash flow with a small buffer for bank posting nuances.

Pricing & Total Cost of Ownership (TCO): What U.S. Teams Should Model

ACH unit fees are typically a fraction of card interchange or wire fees. Your TCO should include:

- Per-item fees: ACH credit/debit entries; incremental fee for Same Day ACH.

- Addenda & data handling: Some processors price addenda or remittance separately for CCD/CTX.

- Risk & returns: Reserve requirements, return-handling fees, and potential network enforcement costs if thresholds are exceeded.

- Compliance & security: Account validation tools, Micro-Entry monitoring, and data-at-rest encryption if you’re in scope.

Because ACH is so cost-effective at scale, many U.S. subscription, B2B, and invoice-heavy businesses migrate high-ticket or recurring card payments to ACH to improve margins and reduce churn linked to card expirations.

ACH for Payroll (U.S.) – A Step-by-Step Implementation

- Collect employee authorizations (PPD credit) with routing/account details.

- Validate account (e.g., Micro-Entries) especially for first-time setup or bank changes.

- Transmit payroll file to your ODFI by the cutoff—use Same Day ACH for off-cycle corrections or urgent payments up to $1M per payment.

- Reconcile posted entries and handle exceptions (RDFI NOCs, returns).

- Secure data at rest and limit access to payroll banking credentials per Nacha’s supplemental security posture if you’re in scope.

ACH for Recurring Billing & Subscriptions (U.S.) – Reduce Churn and Risk

- Use WEB (internet) or PPD (prearranged consumer) based on your channel.

- Present clear consent with terms, revocation process, and contact info.

- Validate accounts (WEB rule) and layer fraud screening to reduce R10/R11 unauthorized returns.

- Offer Same Day ACH in limited cases (e.g., reinstatements) where speed aids retention.

- Monitor unauthorized return rate ≤ 0.5%, and implement proactive outreach when returns spike.

ACH for B2B Vendor Payments (U.S.) – Level Up Remittance & Controls

- Standardize vendor banking collection with out-of-band verification for changes (phone-back to known contacts).

- Prefer ACH credits (CCD/CTX) with rich remittance addenda for automated cash application.

- Use Same Day ACH for just-in-time deliveries, urgent reconciliations, or discounts—benefiting from the $1M limit per payment where needed.

- Deploy credit-push fraud defenses: confirmation-of-payee steps, dual approval, daily anomaly reports, and a rapid recall playbook.

Compliance Calendar: What’s “Latest” in ACH Rules that U.S. Teams Ask About

- Same Day ACH per-payment limit: $1,000,000 (effective Mar 18, 2022). This materially expands use cases for high-value, urgent transactions.

- WEB Debit Account Validation (effective 2021; enforceable thereafter). Requires commercially reasonable account validation for internet-initiated debits.

- Micro-Entries (Phase 1 in 2022; Phase 2 in 2023). Standardizes “ACCTVERIFY” and mandates fraud monitoring of Micro-Entry activity.

- Supplementing Data Security Requirements (phased from 2022). Large non-FI originators/TPS/TPSPs must render account data unreadable at rest; additional milestones continue to roll out.

- Risk Management Framework for Credit-Push Fraud (late 2022, ongoing focus). Broad industry guidance to mitigate vendor impersonation and similar schemes.

- Network growth (2025). ACH volumes and values continue to rise, underscoring the importance of modern controls and automation.

Troubleshooting & Optimization: Keeping ACH Clean and Fast

- Elevated unauthorized returns? Re-examine authorization language, confirmation emails/SMS, and WEB validation steps. Segment first-payment debits for stricter screening.

- Administrative returns (R03/R04) too high? Implement IBAN-style check digit analogs (routing/account format checks), use Micro-Entries before first debit, and give customers a profile-update flow pre-billing.

- Slow posting? Ask your bank for Same Day ACH windows and cutoffs; align job schedules and export times.

- Security scope creep? Inventory where account numbers are stored and apply encryption/tokenization to meet supplemental data-at-rest requirements when in scope.

- Credit-push fraud alerts? Require verified contacts for vendor banking changes, implement payment holds, and rehearse your ACH recall and escalation runbook.

Key Terms (U.S. ACH Terminology you’ll See Everywhere)

- ACH Credit / ACH Debit: Push vs. pull entries through the ACH Network.

- SEC Codes: Standard Entry Class codes like PPD, WEB, TEL, CCD, CTX describing channel/use case.

- ODFI / RDFI: Originating vs. Receiving Depository Financial Institution (your bank vs. your customer’s bank).

- NOC: Notification of Change—RDFI’s structured way to suggest corrections (e.g., updated account/routing).

- Return Codes: Standard reasons for exceptions (e.g., R01 NSF, R03 No Account, R10 Unauthorized).

- Same Day ACH: Intraday windows enabling same-day settlement up to $1M per payment.

- Micro-Entries (“ACCTVERIFY”): Small test credits (and optional debits) used for account verification.

- WEB Debit Account Validation: Required screening/validation for internet-initiated debits.

FAQs

Q1) Is ACH “instant”?

Answer: No. ACH is batch-based. Same Day ACH can settle the same business day if you meet cutoff times and entries are eligible, but it is not a 24/7/365 instant rail. Posting still depends on RDFI end-of-day availability rules. For true instant payments, compare FedNow/RTP.

Q2) What’s the current Same Day ACH limit?

Answer: $1,000,000 per payment (since March 18, 2022). This applies to both credits and debits where eligible.

Q3) Do I have to validate accounts for online ACH debits?

Answer: Yes. The WEB Debit Account Validation requirement mandates a commercially reasonable validation and fraud detection program for internet/unsecured-network debits. Micro-Entries, database checks, and other tools are common approaches.

Q4) What are acceptable unauthorized return rates?

Answer: Keep unauthorized returns at or below 0.5%. There are also administrative (3%) and overall (15%) return rate levels that can trigger inquiries. Monitor these metrics continuously.

Q5) Are Micro-Entries required—and what is “ACCTVERIFY”?

Answer: If you use Micro-Entries, Nacha rules standardize their format. The Company Entry Description must be “ACCTVERIFY,” and Phase 2 requires fraud detection monitoring of those entries.

Q6) How is Nacha addressing modern fraud?

Answer: Nacha’s Risk Management Framework for the Era of Credit-Push Fraud emphasizes education, collaboration, and layered defenses for vendor impersonation and similar scams. Build controls for supplier banking changes and rapid response for recalls.

Q7) Do I need to encrypt bank account numbers at rest?

Answer: If you’re a high-volume non-FI Originator, TPS, or TPSP (crossing defined volume thresholds), Nacha’s Supplementing Data Security Requirements require rendering account data unreadable at rest. Phased milestones began in 2022; confirm your scope and timelines.

Q8) Is ACH still growing in the U.S.?

Answer: Yes. The network continues to scale in both payments and value—Q3 2025 alone saw 8.8B payments totaling $23.2T—driven by B2B expansion and broader adoption of digital bill pay and payroll.

Conclusion

The ACH Network remains the backbone of U.S. account-to-account payments. With Same Day ACH enabling up to $1M per payment, and volumes growing across payroll, B2B, and subscription billing, the opportunity is to combine ACH’s unmatched reach and cost-efficiency with modern controls.

Get the basics right—authorizations, WEB debit account validation, Micro-Entry standards, return-rate monitoring, and data-at-rest protection—and layer in credit-push fraud defenses for outbound B2B flows.

Done well, ACH improves cash flow, reduces payment costs, and delivers a clean customer experience. And because Nacha continues to evolve rules and guidance, make it a habit to revisit your policy, technology, and training at least annually against the latest requirements and volumes.

Leave a Reply