The Automated Clearing House (ACH) is the backbone of electronic payments in the United States. It’s a nationwide network that moves money between bank accounts, powering everything from direct deposit of payroll to automatic bill payments.

For business owners, Automated Clearing House offers a cost-effective, efficient alternative to paper checks and expensive wire transfers. In fact, the ACH Network handled 33.6 billion payments in 2024 totaling $86.2 trillion, a 6.7% increase in volume over the prior year. This remarkable scale underscores how essential Automated Clearing House has become for U.S. commerce.

In this article, we’ll explore what ACH is, how it works behind the scenes (including technical details like NACHA rules), and how it compares to other payment methods like wire transfers, paper checks, and real-time payments (RTP). Business owners will gain a clear understanding of Automated Clearing House and practical insights into using it for their operations.

What is Automated Clearing House (ACH)?

The Automated Clearing House (ACH) is an electronic funds transfer system that enables banks and credit unions to send money to each other on behalf of customers. It’s often called an “electronic bank transfer” or “direct bank payment”, and it’s governed by the National Automated Clearing House Association (NACHA). In simple terms, Automated Clearing House allows businesses, individuals, and government entities to move money from one bank account to another without using paper checks or card networks.

Common uses of Automated Clearing House include direct deposit of salaries, automatic bill pay, business-to-business (B2B) vendor payments, tax refunds, and more. ACH payments are sometimes referred to as “EFT” (electronic funds transfers) or “eChecks”, but all these terms boil down to the same idea: a digital transfer of funds through the Automated Clearing House network.

A Brief History: The ACH network in the U.S. traces its roots to the late 1960s and was officially established in 1974. It was created to reduce the reliance on paper checks as the volume of check payments became difficult to manage. Over the decades, Automated Clearing House has continually advanced – adding new transaction types, increasing speed, and expanding operating hours.

What started as a next-day payment system has evolved significantly, especially in recent years with Same Day Automated Clearing House (launched in phases from 2016 to 2018) that enables much faster settlements. Today’s Automated Clearing House Network can reach all U.S. financial institutions (over 10,000 banks and credit unions), and even supports international transfers via International ACH Transactions (IAT) standards, though its primary focus remains domestic U.S. payments.

How Does ACH Work?

At its core, ACH is a batch processing system that groups transactions together and settles them at specific intervals. Unlike a credit card transaction that might occur in real-time, Automated Clearing House transactions are processed in batches throughout the day. Here’s a step-by-step look at how an ACH payment moves from one account to another:

- Originator: Every Automated Clearing House transfer starts with an Originator, the entity (a business, individual, or government agency) initiating the payment. For example, if a company is paying its employees via direct deposit, the company is the Originator. If a customer authorizes a business to pull a monthly payment from their account, the business is the Originator of that ACH debit.

- ODFI (Originating Depository Financial Institution): The Originator’s bank is known as the ODFI. This is the bank that receives the payment instructions from the Originator. The ODFI consolidates ACH transactions from all its customers into batches. For instance, a company’s bank will gather that company’s payroll direct deposits (Automated Clearing House credits) or customer bill payments (Automated Clearing House debits), often combining them with Automated Clearing House transfers from other clients, and prepare them for the next step.

- ACH Operator: The ODFI transmits the batch of Automated Clearing House entries to an Automated Clearing House Operator. There are two ACH Operators in the U.S.: the Federal Reserve (FedACH service) and The Clearing House (which operates the Electronic Payments Network, EPN). The Automated Clearing House Operator acts as a central hub or clearing center. Its job is to sort and route each transaction to the appropriate receiving bank.

Think of it like a postal sorting facility for payments – it ensures each Automated Clearing House entry finds its way to the correct destination bank. The U.S. Automated Clearing House system is widely reachable – essentially every bank and credit union is connected – so the ACH Operator can route payments between any two U.S. financial institutions. - RDFI (Receiving Depository Financial Institution): The destination bank that receives the sorted ACH entries is called the RDFI. This is the bank where the beneficiary’s account is held. For example, if you’re an employee receiving a direct deposit, your bank is the RDFI.

The RDFI receives the incoming Automated Clearing House file from the Operator and then credits or debits the appropriate account according to the instruction. In our payroll example, your bank credits your account with your paycheck on the scheduled payday; in a bill payment example, the customer’s bank would debit their account for the amount due. - Receiver: Finally, the individual or business whose account is being credited or debited is the Receiver. In an ACH credit (like payroll), the Receiver is the person getting paid. In an ACH debit (like a bill pull), the Receiver is the biller collecting the funds (and the person whose account is debited is the one who authorized it). Once the RDFI posts the transaction to the Receiver’s account, the Automated Clearing House transfer is complete.

This whole process happens quickly and efficiently in the background of the banking system. From a business owner’s perspective, you might only see that you initiated a batch of payments with your bank (or payment processor) and later that your vendor or employee confirmed receipt – but in between, the Automated Clearing House network handled the heavy lifting of moving the money through these stages.

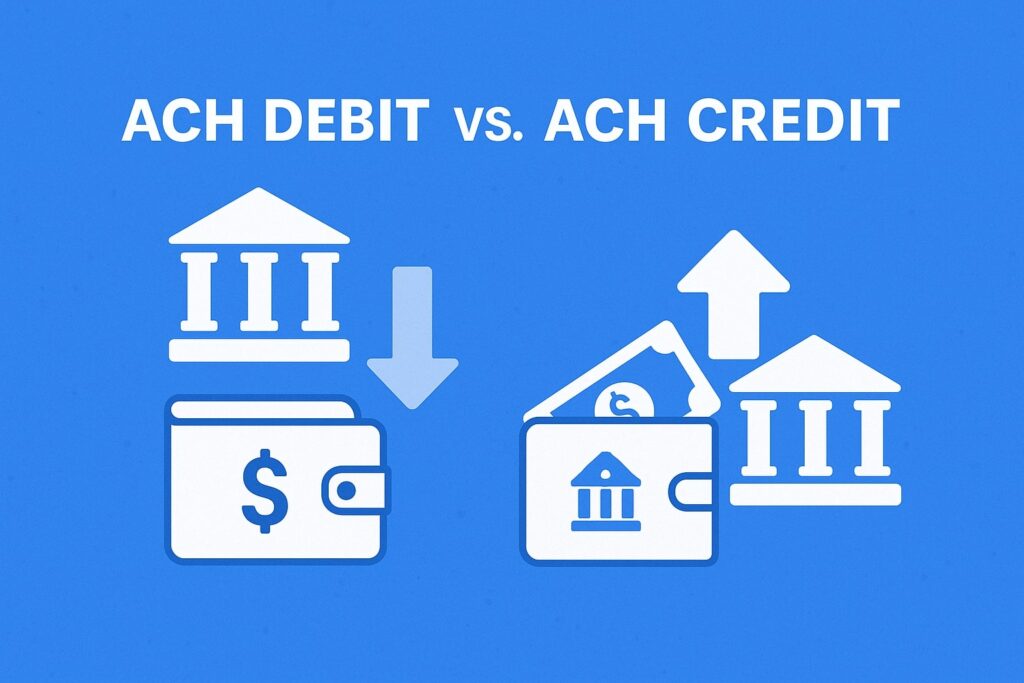

ACH Debit vs. ACH Credit

It’s important to distinguish between two types of ACH transactions: ACH debits and ACH credits. The difference lies in who initiates the payment and the direction of funds:

- ACH Debit (Direct Payment): In an Automated Clearing House debit, the Receiver’s account is debited (funds pulled) and the Originator receives the funds. For example, when a business pulls a monthly subscription fee from a customer’s bank account (with the customer’s authorization), it’s initiating an ACH debit. Another common example is when you set up automatic bill pay and the biller withdraws money from your account.

In Automated Clearing House debit scenarios, the party receiving the money initiates the transaction based on prior authorization. From the perspective of a business owner, Automated Clearing House debits are useful for collecting payments from customers (avoiding the customer “forgetting” to pay). However, Automated Clearing House debits require proper authorization – under NACHA rules, you must have the customer’s consent (such as a signed form or online agreement) to pull funds, and you must retain proof of that authorization. - ACH Credit (Direct Deposit): In an ACH credit, the Originator’s account is debited and the Receiver’s account is credited – essentially the Originator “pushes” funds to the Receiver. Payroll direct deposit is the classic example: a business (Originator) sends out salary payments to employees’ accounts; each employee’s account receives a credit on payday.

Businesses also use Automated Clearing House credits to pay vendors or suppliers: you initiate a payment that deposits money into the vendor’s bank account (often called an Automated Clearing House direct payment or Automated Clearing House credit transfer). From a business owner’s standpoint, Automated Clearing House credits are a convenient way to pay others electronically with certainty about when the funds will arrive (since you control the timing of the push).

Both ACH debits and credits flow through the same network and follow the general process described earlier – the difference is simply the direction of money movement and who initiates it. In fact, about half of the Automated Clearing House Network’s volume is debits and the other half credits. As of recent estimates, slightly over 50% of ACH payments are debits and just under 50% are credits.

Many ACH debits (like consumer bill payments) are recurring and settle quickly (usually next-day), whereas ACH credits (like payroll) can be scheduled a day or two in advance; NACHA rules actually prevent Automated Clearing House debits from being scheduled more than one business day in the future to protect against stale, unauthorized pulls, while Automated Clearing House credits can be set a bit further ahead (though the majority of ACH credits also now settle within one business day in practice).

Settlement Timing and Processing Schedules

Automated Clearing House is often called a “batch” system because transactions are not processed one-by-one instantly, but rather in groups at set times. Historically, this meant Automated Clearing House payments could take a couple of days to fully settle. Today, however, around 80% of all ACH payments settle within one business day or less, thanks to improvements like Same Day Automated Clearing House and streamlined processing. Here are key points on timing and speed:

- Standard ACH Timing: In the traditional Automated Clearing House cycle, an Automated Clearing House file transmitted by the ODFI during the day would settle (funds actually exchanged between banks) overnight or the next business day. ACH credits were commonly delivered in 1-2 business days, and Automated Clearing House debits usually in 1 day.

For example, if your business runs payroll on Thursday, employees might see the deposit on Friday (next-day). If a customer’s payment is pulled on Monday, it might settle and show in your account by Tuesday. - Same Day ACH: Recognizing the need for faster payments, NACHA launched Same Day ACH in recent years. Initially rolled out in phases (2016-2018) and expanded in 2021, Same Day Automated Clearing House allows many Automated Clearing House transfers to clear within the same business day. Banks now have multiple submission windows: as of March 2021, there are three daily processing cycles for same-day settlement, with the latest deadline at 4:45 p.m. ET for same-day processing.

By rule, any qualifying ACH payment submitted by that cutoff will settle by the end of that day (typically by 5:00 p.m. local time at the RDFI). Same Day Automated Clearing House has grown extremely fast – over 1.2 billion same-day payments were made in 2024 (a 45% increase from the prior year) as businesses and consumers embrace faster transfers. There is a per-payment limit for Same Day ACH (currently $1 million per transaction), which was raised in March 2022 to accommodate larger payments. - Operating Hours: The Automated Clearing House Network operates 23¼ hours every business day, closing only for a brief window each night and on weekends/holidays. In practical terms, this means banks can submit ACH files almost round-the-clock on weekdays. However, settlements occur when the Federal Reserve’s settlement system is open.

Currently, settlements happen four times a day on weekdays (corresponding to a few Automated Clearing House cycles throughout the day). If an Automated Clearing House transaction is initiated over a weekend or holiday, it will typically be processed when the next business day begins. Standard industry practice for things like payroll is to adjust for weekends/holidays – for instance, if payday falls on a Saturday, the deposit is usually made on Friday instead.

For a business owner, what matters is that Automated Clearing House offers flexibility in speed: you can choose standard ACH if timing isn’t critical (to save cost), or Same Day Automated Clearing House for a small extra fee if you need the money moved faster.

By planning your payment schedule with your bank or payments provider, you can ensure vendors are paid or funds received by the needed date. Most banks provide cut-off times each day for Automated Clearing House files – if you upload a payment batch by, say, 5 PM, it might go out in the next cycle.

NACHA’s Role and Operating Rules

You might be wondering who oversees the ACH system. This is where NACHA (National Automated Clearing House Association) comes in. NACHA is a not-for-profit association that governs the Automated Clearing House Network and sets the NACHA Operating Rules that all participants must follow. While NACHA itself doesn’t process payments (the actual processing is done by the banks and Automated Clearing House Operators), it provides the rulebook that keeps the network running smoothly and securely.

Key aspects of the NACHA Operating Rules and compliance that business owners should know include:

- Standard Formats: NACHA sets the standard file formats and message codes for ACH transactions. This ensures that an Automated Clearing House file from any bank can be understood by any other bank. Businesses typically don’t have to handle these formats directly if they use banking software or a payroll provider, but it’s good to know there’s a rigorous standard in place.

- Authorization Requirements: ACH debits (pulling money from someone’s account) require prior authorization. NACHA rules lay out what constitutes proper authorization (e.g., a signed Automated Clearing House agreement, an online checkbox with clear terms, etc.). Businesses initiating Automated Clearing House debits must retain proof of their customers’ authorization and provide it if a payment is disputed. This protects consumers and businesses from unauthorized withdrawals.

- Return Codes and Timeframes: If something goes wrong – say an account has insufficient funds, is closed, or a transaction was unauthorized – Automated Clearing House has a system of return codes. The RDFI can return an ACH entry to the ODFI with a code explaining why (e.g., NSF for non-sufficient funds). NACHA rules define the timelines for returns. In general, most returns happen within 1-2 business days of the original transaction.

However, an unauthorized debit to a consumer account can be returned even after that (consumers have up to 60 days to dispute an unauthorized Automated Clearing House under federal Regulation E). Business accounts have shorter windows for ACH disputes, so as a business owner, you should reconcile and report any issues quickly. - Risk and Fraud Controls: NACHA regularly updates rules to combat fraud. For example, in March 2021 NACHA began requiring that originators of online Automated Clearing House debits (WEB entries) implement account verification for new payers – a response to growing fraud in e-commerce ACH debits.

Additionally, NACHA has penalties for institutions that have excessive numbers of returned items (to discourage abuse of the system). If a company keeps sending Automated Clearing House debits that bounce or get disputed, their bank (the ODFI) is expected to address it, and NACHA can levy fines for rule violations. The bottom line is that there is a governance structure ensuring ACH payments remain reliable and safe for all users.

NACHA’s governance has been key to Automated Clearing House’s success: it balances innovation (like enabling faster payments) with security (through rules and compliance requirements). It’s worth noting that NACHA coordinates with the Federal Reserve and other stakeholders on improvements.

For instance, the expansion of Same Day Automated Clearing House and increasing transaction limits were done in consultation with financial institutions to meet market needs. As a business owner, you generally won’t need to delve into the weeds of the rulebook, but understanding that ACH is a regulated network with uniform rules should give you confidence in its consistency and reliability.

Benefits of ACH for Businesses

Why do businesses large and small use Automated Clearing House? Here are some of the major advantages of ACH payments for a company:

- Cost Savings: ACH transfers are much cheaper than paper checks or wire transfers. According to industry data, an ACH payment typically costs around $0.20 to $0.50 (sometimes up to around $1), whereas a paper check can cost a few dollars when you factor in paper, printing, mailing, and processing costs.

In fact, sources cite that Automated Clearing House transfers average about $0.40 in fees, versus $2 to $4 (or more) per check. Wire transfers are even more expensive, often $15–$30 for domestic wires and more for international. The low cost of Automated Clearing House makes it ideal for routine payments like payroll, vendor invoices, or subscription billing, where paying by check or wire would rack up unnecessary expenses. - Efficiency & Convenience: ACH is largely automated and digital. No more chasing signatures on checks, making trips to the bank, or waiting for mail delivery. A business can initiate dozens or thousands of payments in one go through online banking or accounting software, and those funds transfer electronically.

This saves a huge amount of time for finance staff. It also speeds up receivables – for example, instead of waiting for a check to clear, a business can receive an ACH credit and be confident the money will be in its account by the next day. Government and businesses alike have found Automated Clearing House improves timeliness of payments. - Recurring Payments Made Easy: If your business needs to collect recurring payments (membership fees, subscriptions, installment payments, etc.), Automated Clearing House is a perfect solution. Customers can authorize an ACH debit once, and then you can pull payments on the schedule (monthly, quarterly, etc.) without them needing to take any action each time.

This increases on-time payment rates and makes life easier for your customers too (no need to remember to mail a check). Many payroll systems also run recurring direct deposits via Automated Clearing House, so each pay cycle is automated. - Secure and Reliable: ACH transactions are very safe when proper procedures are followed. Funds move directly between banks over encrypted networks – there’s no physical document that can be lost or stolen in transit. ACH payments are actually considered less susceptible to certain types of fraud than checks, which can be altered or counterfeited.

A telling statistic in a 2022 survey, 66% of organizations reported being victims of check fraud, whereas only 37% experienced Automated Clearing House debit fraud. This is partly because checks contain your bank account and routing numbers in plain text and pass through many hands, whereas Automated Clearing House data is handled bank-to-bank securely. Additionally, every ACH payment has clear records (you’ll see the sending/receiving company names on bank statements), aiding transparency and traceability. - Customer Preference & Ubiquity: In the U.S., ACH is everywhere – virtually every bank account (checking or savings) can send and receive Automated Clearing House. Your employees likely expect direct deposit (over 95% of U.S. workers are paid via direct deposit) because it’s fast and dependable.

Many vendors and suppliers also prefer Automated Clearing House because it goes straight to their bank, eliminating trips to deposit checks. By using Automated Clearing House, businesses can meet modern payment expectations and even improve relationships (for example, paying suppliers via Automated Clearing House can be faster than mailing checks, which they will appreciate). - Cash Flow Management: With Automated Clearing House, you can predict when funds will leave or enter your account, which aids in cash flow planning. If you issue checks, you never quite know when the payee will deposit them (it could be the same day or weeks later), which complicates cash management. ACH debits and credits are usually set to clear on known dates. Also, with Same Day Automated Clearing House available, businesses have a faster option when needed (e.g., a last-minute payroll correction or emergency vendor payment can be done same-day).

- Environmental and Administrative Savings: Replacing paper payments with electronic ones means less paper waste and often less manual work. No checks to print, no envelopes, no postage – all of which not only cost money but also time. Automated Clearing House integrates well with accounting systems, enabling easy reconciliation (many banks provide reporting for ACH transactions that you can import into accounting software). This automation reduces the chance of human error that comes with manually handling checks or cash.

In summary, ACH offers a blend of low cost, security, and convenience that is very attractive for routine financial transactions. It’s particularly well-suited for domestic payments that are not extremely time-sensitive (if you need instant, there are other methods discussed later). For the vast majority of payroll, vendor payables, accounts receivable, and tax payments, Automated Clearing House hits the “sweet spot” of being fast enough, cheap, and dependable.

Potential Drawbacks and Considerations

No payment method is perfect for every situation. Here are some limitations or risks of ACH to keep in mind, especially as a business owner:

- Speed Constraints (No True Instant Settlement): While Automated Clearing House is much faster than mailing a check, standard Automated Clearing House is not real-time. Even with faster processing, most ACH payments will clear next day or within a day, not within seconds. Same Day Automated Clearing House speeds this up to a few hours, but ACH still operates only during banking days/hours (no weekends, no holidays for settlement).

If your business needs to send or receive money urgently outside of business hours – for example, late on a Sunday – Automated Clearing House won’t reach the other side until at least Monday. Newer instant payment options (like RTP or FedNow) fill this gap, as we’ll discuss, but they have their own limitations. For critical, time-sensitive payments (like closing on a property the same day), businesses often still use wire transfers or RTP instead of Automated Clearing House. - Reversals and Uncertainty for Received Payments: When you receive an ACH payment, you generally trust that it’s secure. However, Automated Clearing House transactions can be reversed or returned under certain conditions, which is different from a wire where funds are final. For instance, if a customer’s ACH payment bounces due to insufficient funds, you might not know until a day or two after you thought you got paid. Or if a consumer disputes an unauthorized charge, the money could be pulled back from your account.

This is why many businesses wait a couple of days before treating an ACH debit from a customer as “cleared.” The ability to reverse is a double-edged sword – it provides protection in case of errors or fraud, but it also means ACH credits you receive are not guaranteed final until any return window closes. In contrast, a wire transfer is largely irrevocable once done.

Business owners should design their processes with this in mind (e.g., if you’re receiving Automated Clearing House from customers, monitor for returns; if you’re shipping goods upon receiving ACH, consider waiting until the payment settles without return). - Transaction Limits: ACH isn’t ideal for very large, one-off payments. While there’s technically no cumulative dollar limit for ACH transfers, there are practical limits. Many banks impose a cap on Automated Clearing House transfers for businesses (especially for new or small businesses) to manage risk. Also, as mentioned, Same Day ACH has a $1 million per payment limit.

If you need to send a multi-million dollar payment, a wire transfer may be more appropriate as it can handle virtually any amount in one go. That said, the $1 million limit covers the vast majority of typical business transactions, and standard ACH can be scheduled in multiple batches if needed for larger amounts. - International Payments are Limited: ACH is predominantly a U.S. system. If you need to pay overseas vendors or receive funds from international clients, Automated Clearing House alone may not suffice. NACHA’s IAT standard allows international ACH payments by converting them through U.S. correspondent banks, but in practice many businesses will use wire transfers or other international payment platforms for cross-border needs. ACH is best thought of as a domestic payment workhorse; for global transactions, other channels might be needed.

- NACHA Compliance Requirements: As touched on earlier, if your business originates ACH entries (especially debits), you have to comply with NACHA rules. This isn’t so much a “problem” as it is a responsibility – for example, obtaining and storing authorizations, securing sensitive bank data, and staying below return rate thresholds. Banks and payment processors typically guide businesses through these requirements.

However, non-compliance can result in fines or termination of your Automated Clearing House origination privileges. In recent years, NACHA has focused on requiring stronger fraud prevention (like account verification for online debits) and setting standards for data security. Business owners should be prepared to implement these measures, which might involve using verification services or ensuring encryption of bank account info. - Error Resolution and Support: If an ACH payment goes awry (wrong account number entered, etc.), resolving it isn’t always instant. Automated Clearing House entries that go to a valid but incorrect account can be tricky to retrieve – it often requires cooperation from the unintended recipient or their bank. While NACHA has processes like NOCs (Notifications of Change) to correct account info and ACH return codes to handle many errors, it’s possible to have situations where money is in limbo.

By double-checking account details and using validation tools, businesses can minimize these errors. But it’s fair to say ACH doesn’t have the dispute resolution infrastructure of, say, credit cards (where you can chargeback a transaction through the card network). In most cases, though, Automated Clearing House errors are infrequent and processes exist to fix them; it just may take a bit of time.

Overall, the drawbacks of Automated Clearing House are manageable and often just the flip side of its advantages. ACH’s ability to be reversed for certain reasons is part of what makes it safer for consumers. Its lack of instant 24/7 speed is being mitigated by new payment innovations.

As a business, understanding these limitations ensures you use Automated Clearing House in appropriate situations – for routine payments where its strengths shine – and choose alternative methods when you need immediacy or absolute certainty of finality.

ACH vs. Other Payment Methods

ACH is a versatile payment rail, but how does it stack up against other options like wire transfers, paper checks, and Real-Time Payments (RTP)? Each method has its place. Below is a comparison of key features to help illustrate the differences:

| Feature | ACH (Automated Clearing House) | Wire Transfer | Paper Check | Real-Time Payments (RTP) |

|---|---|---|---|---|

| Settlement Speed | Batch processing – Typically next-day or 1–2 business days for standard ACH; same-day settlement available for eligible payments. | Fast (Same-day) – Domestic wires settle within minutes to hours on the same day (Fedwire/CHIPS operate during business hours). International wires may take 1–2 days. | Slow – Physical checks must be mailed, deposited, and cleared. Can take several days (mail transit + 1-2 day bank clearing). | Instant – Payments settle in real-time, 24/7/365. Funds are available immediately to the recipient, even nights and weekends. |

| Operating Hours | Business days, ~23 hours/day (network closed briefly overnight). No settlement on weekends/holidays (transactions queued for next business day). | Business days, during bank operating hours (Fedwire: typically 8am–6pm ET on weekdays). Not available nights, weekends, or bank holidays. | N/A (Physical) – Checks can be written anytime, but deposit processing depends on bank hours. Clearinghouses operate on business days. | 24/7 Continuous – RTP networks never close, supporting transactions anytime (including weekends and holidays). |

| Cost per Payment | Low cost – Often pennies per transaction (roughly $0.20–$1 typical). Banks may charge a small fee or bundle it free in business accounts. | High cost – Typically $15–$30 for domestic wires (banks charge per wire) and higher for international (often $40+). Premium cost for speed/finality. | Varies/high – Material + labor costs make each check cost ~$2–$4 on average (including printing, mailing, handling). Banks may charge for check deposits too. | Low-moderate – RTP transactions might cost around $0.25–$1 for banks to process. Some banks pass on a small fee to businesses; others may include it in account services. Currently cheaper than wires, but slightly more than standard Automated Clearing House. |

| Transaction Limits | Per Payment: $1 million limit for Same Day ACH; no explicit network cap for standard Automated Clearing House (but banks may set limits for their customers). Best for small to mid-sized payments (commonly used for anything from a few dollars up to hundreds of thousands). | Very high/No true limit – Wires can handle large sums (multi-million or more) in single transfers. Ideal for high-value transactions like corporate treasury or real estate closings. | No fixed limit – You can write a check for any amount, but practicality and risk make very large checks uncommon. Checks above ~$10k may face holds and verifications. | Moderate – RTP in the U.S. initially had lower limits; as of 2023–2024, the limit is often around $1 million per transaction (and increasing as network evolves). Suitable for most business payments but not extremely large values yet. |

| Reversibility | Reversible under certain conditions – ACH entries can be returned or reversed for errors or unauthorized transactions. There are defined return timeframes (e.g., NSF returns within 2 days; consumer unauthorized debit within 60 days). This provides an “undo” mechanism, but also means a transaction isn’t final until that window passes. | Irreversible once settled – Wires are final payments. Once a wire is sent and credited, it’s extremely difficult to revoke. This reduces fraud disputes but means senders must be very sure of details. | Can bounce or be stopped – A check can bounce (insufficient funds) or be canceled via stop-payment request. Also subject to fraud (forgeries). So a check isn’t guaranteed good until it fully clears, which can take a few days or more. | Irreversible – RTP payments are final and irrevocable once executed. There is instant confirmation of funds, and no chargeback mechanism, which is good for recipients but requires trust in the sender. |

| Security & Fraud | Secure, low fraud incidence – Encrypted bank-to-bank transmission. Requires account info (which, if obtained illicitly, can be misused – but overall ACH fraud rates are relatively low). ACH debits require authorization, limiting unauthorized pulls. However, Automated Clearing House does have some fraud risks like incorrect routing or account takeover, so businesses should use verification and monitoring. | Secure, but fraud can be costly – Wires are sent bank-to-bank with strong verification steps. Fraud typically occurs via social engineering (e.g., business email compromise tricking someone into wiring to a scammer). Because wires can’t be recalled, a fraudulent wire can lead to irrevocable loss. Thus, strict controls (call-back verifications for wire instructions, etc.) are used. | Higher fraud risk – Checks are paper documents with your account and routing number plainly visible. They can be stolen, altered (“check washing”), or counterfeited. According to the AFP, checks are the payment method most often targeted by fraud. Positive pay and other bank fraud prevention services can mitigate risk, but those add cost. Overall, Automated Clearing House or electronic methods are safer than checks. | Highly secure – RTP was designed with built-in fraud checks. The sending bank confirms sufficient funds in real-time and provides instant confirmation to the receiver. The irrevocability removes certain fraud vectors (no chargeback fraud). However, senders must be vigilant to not send money in response to scams, as there’s no recourse after sending. |

| Common Use Cases | Salaries, vendor payments, bills, B2B and B2C transactions – Ideal for routine, recurring payments or any transfer where low cost is a priority and same-day or next-day is fast enough. Examples: payroll direct deposit, customer ACH payments on an invoice, monthly subscription charges, tax payments. | Large or urgent transfers, international payments – Used when speed or high-value capability is critical. Examples: closing on a home purchase (down payment via wire), sending money to a supplier abroad, moving large treasury funds between banks. Often one-time or infrequent payments where the fee is acceptable relative to the amount. | Legacy and specific scenarios – Still used for certain B2B payments and by those slow to adopt electronic methods. Examples: paying tradespeople or small vendors who haven’t set up electronic payments, writing checks for legal purposes (some jurisdictions require checks for certain trust disbursements), or situations where a physical check is needed as a receipt. Usage is steadily declining each year as more businesses transition to Automated Clearing House and electronic methods. | Instant payments needs – Situations requiring immediate clearing and confirmation. Examples: real-time B2B payments to suppliers for just-in-time delivery, instant payroll for gig workers at end of day, P2P payments through mobile apps (some use RTP under the hood). RTP (offered by The Clearing House) and the new FedNow service (offered by the Federal Reserve, launched 2023) are creating new use cases for instant business payments. |

Table: Comparison of ACH with wire transfers, paper checks, and Real-Time Payments (RTP), highlighting key differences in speed, cost, finality, security, and usage.

As the table shows, Automated Clearing House hits a sweet spot for many typical business transactions due to its low cost and adequate speed. Wires and RTP are faster and final, but come at higher cost or require both parties’ banks to be on the network (RTP coverage is growing but not yet universal).

Checks, once dominant, are now often the least attractive option due to their manual nature, higher fraud risk, and processing delays. Even the U.S. government is pushing to reduce check usage – an initiative was noted to eliminate federal check payments in favor of electronic methods due to cost savings and fraud reduction.

ACH vs. Wire Transfers: If you need to ensure funds are delivered the same day with no risk of reversal, a wire may be preferable. For example, many businesses use wire transfers for closing large deals or sending deposits where the recipient demands cleared funds immediately. However, you pay a premium for this speed and certainty.

For everyday payments like payroll or vendor bills, wires are usually overkill – that’s where Automated Clearing House shines, saving you money. Additionally, wires can be sent internationally directly, whereas ACH is domestic (with exceptions via IAT). In many cases, businesses maintain the ability to do both: use Automated Clearing House by default, and wires when absolutely necessary (time-critical or very large payments).

ACH vs. Checks: Replacing checks with ACH can yield significant benefits. Automated Clearing House is faster (no postal delay), cheaper per transaction, and more secure. Checks expose your bank account info and can be forged or misused; in fact, banking details on checks have been a source for fraudsters to initiate unauthorized ACH debits, so reducing check usage also reduces that risk.

For a business still writing lots of checks, moving to Automated Clearing House can save on the order of a few dollars per payment in hard costs, and even more in staff time. The only advantages of checks might be simplicity (anyone can write a check without needing bank setup) and certain legal use-cases or customer preferences.

But even those are fading as electronic payments become standard. Many accounting systems and banks offer bill payment services that effectively convert your payments to ACH or electronic methods, phasing out the need to manually cut checks.

ACH vs. RTP (Real-Time Payments): RTP is the new kid on the block (launched in the U.S. in 2017 by The Clearing House) and, along with the Federal Reserve’s FedNow (launched in 2023), represents the move toward instant payments. The RTP network allows money to move from one bank to another in seconds, at any time.

This is a game-changer for certain uses – for instance, businesses can pay contractors as soon as a job is done, or reconcile invoices in real-time. RTP also carries more remittance information (rich messaging) which can simplify reconciliation.

However, to use RTP, both the sender’s and receiver’s banks must be participants in the RTP network. As of 2025, a majority of U.S. accounts are reachable via RTP, but not all (adoption is still ongoing across smaller banks). Also, RTP payments are final – there’s no reversal – which means they aren’t suited for scenarios where you might need to pull money back (where Automated Clearing House’s reversible nature is actually an advantage, like certain consumer payments).

Cost-wise, RTP is more expensive for banks than ACH but far cheaper than a wire; many banks price it modestly to encourage use. Over time, we may see instant payments become the norm for many transactions, but currently Automated Clearing House offers a very robust and widely compatible solution, especially when absolute instant speed isn’t required.

In summary, business owners should choose the payment method that fits the context:

- Use Automated Clearing House for routine, non-urgent, or high-volume payments where cost efficiency is key (payroll, vendor payables, subscriptions, etc.).

- Use wires for high-value or extremely time-sensitive payments, or international transfers where ACH isn’t available.

- Use RTP/FedNow when you need instant payment capabilities and both parties’ banks support it – it’s great for immediate needs and improving cash flow timing.

- Use checks only when no electronic option is available or when a physical instrument is required – and recognize the added costs and risks.

Most likely, as a business owner in the U.S., you’ll find ACH to be your workhorse for the majority of transactions, with an occasional wire or real-time payment as a complement.

Frequently Asked Questions

Q: How long do ACH transfers take to complete?

A: Standard Automated Clearing House transfers typically take 1 to 2 business days to post, depending on whether it’s an ACH credit or debit. ACH debits (like bill payments) often settle by the next business day. ACH credits (like direct deposits) usually settle within one business day as well, or two days at most in some cases. With the advent of Same Day Automated Clearing House, many transfers can be completed the same day they are initiated (funds available by end of day).

In fact, NACHA reports that 80% of all ACH payments now settle within one day or less. However, Automated Clearing House does not operate on weekends or bank holidays, so a transfer initiated on Friday might not fully settle until Monday (unless sent via same-day if eligible). Always check with your bank for their cut-off times – for example, if you submit an Automated Clearing House file in the evening, it might miss that day’s window and process the next day.

Q: Are ACH payments safe and secure for my business?

A: Yes, ACH payments are considered very safe. They move through the banking system over secure networks, and banks have verification and fraud detection measures in place. Unlike checks, there’s no physical document that can be lost or altered – everything is digital and encrypted. NACHA’s rules require that ACH transactions be authorized and that banks protect account data. While no payment method is 100% free of fraud risk, Automated Clearing House fraud rates are relatively low.

A common fraud scenario to be aware of is if someone steals your bank account information (e.g., from a check or a data breach) and tries to debit your account – but even then, consumers have strong protections (they can dispute unauthorized debits) and businesses can work with banks to recover funds if acted on quickly. It’s also worth implementing additional safeguards: for example, use Automated Clearing House block or filter services on your accounts (your bank can block all ACH debits except those you pre-authorize, useful for preventing unauthorized pulls).

Overall, with basic precautions, Automated Clearing House is a highly secure way to pay or get paid. Industry experts often note that ACH carries less fraud risk than checks, which is one reason many organizations are shifting from checks to ACH.

Q: What are the NACHA rules and do I need to worry about them as a business owner?

A: NACHA Operating Rules are essentially the rulebook for how ACH transactions must be handled by banks and businesses. If you are initiating Automated Clearing House payments through your bank or a payment processor, that institution will ensure the transactions comply with NACHA rules.

The main things you, as a business originator, should be aware of include: obtaining proper authorization for any ACH debit (have your customer sign a form or agree electronically and keep that record), retaining records of payments and authorizations, and not initiating fraudulent or improper transfers.

Also, be mindful of the timing (e.g., don’t date an Automated Clearing House debit for more than one day in the future). If you exceed certain thresholds of returns (for instance, if too many of your ACH debits bounce or are unauthorized), your bank may reach out to you to address the issue, because NACHA mandates monitoring of return rates. For most legitimate businesses, it’s straightforward to comply with the rules – just use Automated Clearing House for authorized, agreed-upon payments, and keep documentation.

Banks provide Automated Clearing House origination services with these requirements baked in, often giving you templates for authorization or other guidance. So, while NACHA rules are extensive (and updated every year), your role is mainly to use ACH responsibly. If unsure, consult resources like NACHA’s website or your bank’s Automated Clearing House specialists; NACHA also publishes a user-friendly ACH Quick Start Tool and FAQs for businesses getting started with Automated Clearing House.

Q: How does ACH compare to paying by credit card or debit card?

A: ACH transfers and card payments are different rails with different pros/cons. Paying by credit/debit card is typically instant for the merchant (authorization happens in real time), but it carries merchant fees – businesses pay a percentage (often 2-3%) of the transaction to accept card payments. Automated Clearing House, on the other hand, is much cheaper (flat cents), making it great for large payments or thin-margin businesses.

However, ACH isn’t instantaneous authorization like a card swipe; if a customer pays you via Automated Clearing House, you won’t know about NSF (bounced payment) until possibly the next day, whereas a card can decline on the spot if funds are insufficient. Automated Clearing House is also purely bank account to bank account, so it doesn’t offer the line-of-credit aspect that credit cards do (some customers prefer to put payments on a credit card to earn rewards or manage cash flow).

For business-to-business payments, ACH is often favored over cards (to avoid fees), whereas for business-to-consumer sales, cards are more common due to their ubiquity and immediate approval. Some businesses offer Automated Clearing House as a payment option to customers (often calling it “eCheck” or bank transfer) especially for large ticket items or invoices – they might even incentivize it (e.g., “pay by bank to save the credit card fee”).

Both ACH and cards are secure; cards have robust consumer protections (chargebacks), whereas Automated Clearing House has its own dispute process for errors/fraud but is generally used in trust-based transactions (or recurring billing with a mandate). In short: ACH is cheaper and best for bank-to-bank transfers, while cards are faster in authorization and universal for retail settings, but cost more to accept.

Q: Can I use ACH for international payments?

A: Not directly in the same way as domestic payments. The U.S. Automated Clearing House network is domestic, but there is an ACH transaction type called International ACH Transaction (IAT) that some banks support for cross-border payments. In an IAT, your payment instructions are sent through Automated Clearing House to your bank’s U.S. partner, which then passes it to the foreign banking system (possibly converting currency).

However, IATs can be slower and sometimes carry additional fees; they also must comply with extensive OFAC (sanctions) screening. Many businesses prefer using international wire transfers or specialized global payment services for sending money abroad, as those can be more direct.

If your business frequently pays overseas vendors, you might explore a global Automated Clearing House solution or a fintech that sends local bank transfers in target countries. But for a one-off or occasional international payment, a wire might be simpler. On the flip side, if a foreign customer wants to pay you and you both have U.S. bank accounts (or the customer uses a U.S. correspondent), they could send you an ACH – but that’s essentially domestic.

In summary, ACH’s strength is domestic U.S. payments; for international, other methods often take the lead (though Automated Clearing House-inspired systems exist in other countries, like SEPA in Europe, which operate similarly in their regions).

Q: Is there a limit to how much money I can send via ACH?

A: There’s no universal dollar limit mandated by the Automated Clearing House network for standard (next-day) transfers – you could, in theory, send very large amounts by ACH. However, practical limits apply: banks often impose their own limits on Automated Clearing House origination for risk management. For example, a small business might be limited to, say, $100,000 per day in ACH transactions, unless they request a higher limit and have a history to justify it. These limits vary widely by institution and the client’s profile.

For Same Day ACH, NACHA sets a limit of $1 million per individual payment. So you cannot send a single same-day Automated Clearing House above that amount as of 2025. If you need to pay more, you can either send multiple ACH payments in chunks or use a wire. It’s good practice to talk to your bank about your typical payment sizes – if you plan a one-time large Automated Clearing House (e.g., paying a vendor $500k), ensure it’s within your allowed limits or get a temporary increase.

Also note, for consumer-facing applications (like apps that transfer money from user bank accounts), limits may be set lower to manage fraud risk. Always verify with your financial provider what your ACH limits are.

Q: What does it cost to send or receive money via ACH?

A: Automated Clearing House is very affordable. For many business banking accounts, receiving ACH payments is free (banks usually don’t charge incoming ACH fees). Sending Automated Clearing House payments often incurs a small fee – commonly anywhere from $0.25 to $1 per transaction – or a monthly bundle fee. Some banks even include a certain number of ACH transactions at no charge in business accounts.

The exact pricing depends on your bank or payment processor; high-volume users might get volume pricing. Compared to wire transfers (which cost $15-$30 each) or credit card acceptance (which costs ~2-3% of the amount), Automated Clearing House is the low-cost leader. There might be slight premium fees for Same Day ACH, often a bit higher than regular ACH – for example, a bank might charge $1 or $2 for a same-day transaction versus $0.25 for a next-day. But these fees are still nominal.

The cost structure is one reason ACH is used for things like payroll; paying 100 employees by Automated Clearing House might cost you maybe $50 or less total, which is far cheaper than cutting 100 checks or doing 100 wires. When planning to use ACH, check your bank’s fee schedule or a payment service’s fees – many advertise Automated Clearing House as “free or low-cost” and indeed it is a minor expense in the grand scheme.

Q: How does an ACH payment compare to an RTP or FedNow instant payment from a user perspective?

A: From a user perspective (either the business sending/receiving or the end customer), an ACH payment involves a slight delay (funds appear in a day or so), whereas an RTP/FedNow instant payment will reflect in the target account within seconds once initiated.

If you send an Automated Clearing House to a vendor, you might initiate it today and they see it tomorrow; if you send via RTP, they see it right away. Another difference is that to use RTP/FedNow, your bank’s interface must support it – some banks have a button for “real-time payment” or “instant payment” if the payee is eligible.

Otherwise, the experience of providing routing/account info is similar. One consideration: instant payments are typically credit push only (you can send money instantly, but not pull without the other party initiating). Automated Clearing House allows both debits and credits, so for pulling customer payments, Automated Clearing House is the method whereas RTP is more for push payments.

In terms of cost and process, you might not notice the small fee for an RTP if your bank waives it for certain accounts, or they might charge a dollar or so. FedNow and RTP also have messaging – you might get an immediate notification of payment.

Over time, these differences may blur as banks integrate services. But currently, if you initiate a payment in online banking, “Automated Clearing House” might be labeled as standard or next-day transfer and “RTP” as instant – you choose based on urgency and cost. The important thing is recipients will definitely notice the speed difference: e.g., paying a contractor via Automated Clearing House they get it the next business day, via RTP they have it within a minute.

Conclusion

In conclusion, ACH is a foundational payment system for U.S. businesses, offering a blend of affordability, reliability, and broad accessibility that’s hard to beat. It powers the direct deposit paychecks that keep employees happy and the automatic bill payments that keep vendors paid on time. From a business owner’s perspective, leveraging Automated Clearing House can streamline operations – reducing costs associated with paper handling, minimizing payment delays, and improving cash flow predictability.

The technical underpinnings we discussed (ODFI/RDFI roles, batch processing, NACHA rules) operate behind the scenes to ensure that whether you’re a small business or a Fortune 500, your electronic payments clear accurately and securely.

In recent years, ACH has kept pace with the demand for speed through Same Day Automated Clearing House, making it even more useful in a world that increasingly expects faster payments. And while new real-time systems like RTP and FedNow are expanding the options for instantaneous transfers, Automated Clearing House remains the workhorse for everyday transactions given its ubiquity and low cost. In fact, rather than being replaced, Automated Clearing House continues to grow year over year in volume, proving its ongoing relevance and adaptability.

For business owners in the United States, understanding ACH is essential. It can give you a competitive edge – for example, you can offer flexible payment options to customers, pay your staff and suppliers efficiently, and reduce overhead. By comparing Automated Clearing House with wires, checks, and emerging alternatives, you can craft a payments strategy that uses the right tool for each job. In many cases, that tool will be ACH for all the reasons outlined.

Embracing ACH payments is a step toward modernizing your financial operations. It’s a prime example of how a decades-old system has modernized and continues to deliver value in the digital age of finance. Whether you’re looking to save money on transaction fees, mitigate fraud risk, or just simplify your accounting processes, Automated Clearing House is likely to play a key role in your solution. With the information in this article, you should be well-equipped to utilize Automated Clearing House effectively and confidently for your business needs.

Leave a Reply